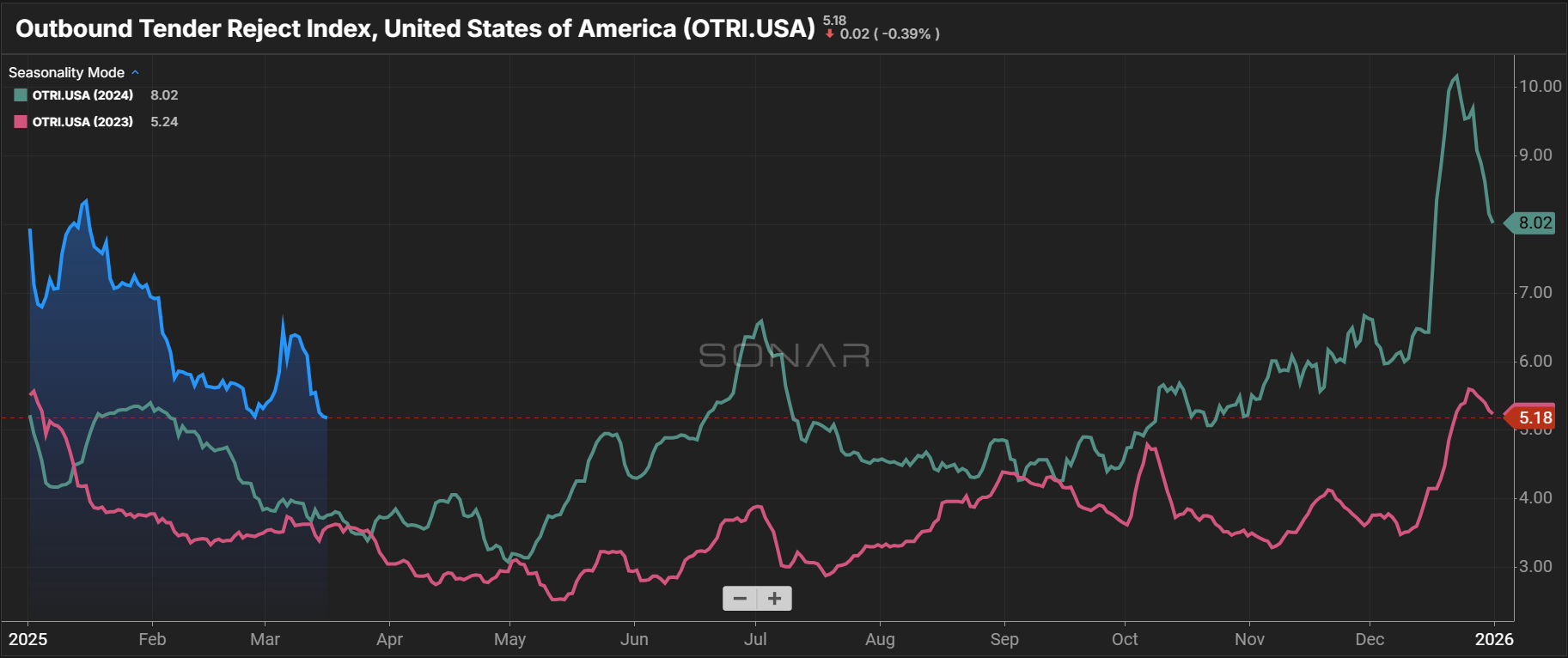

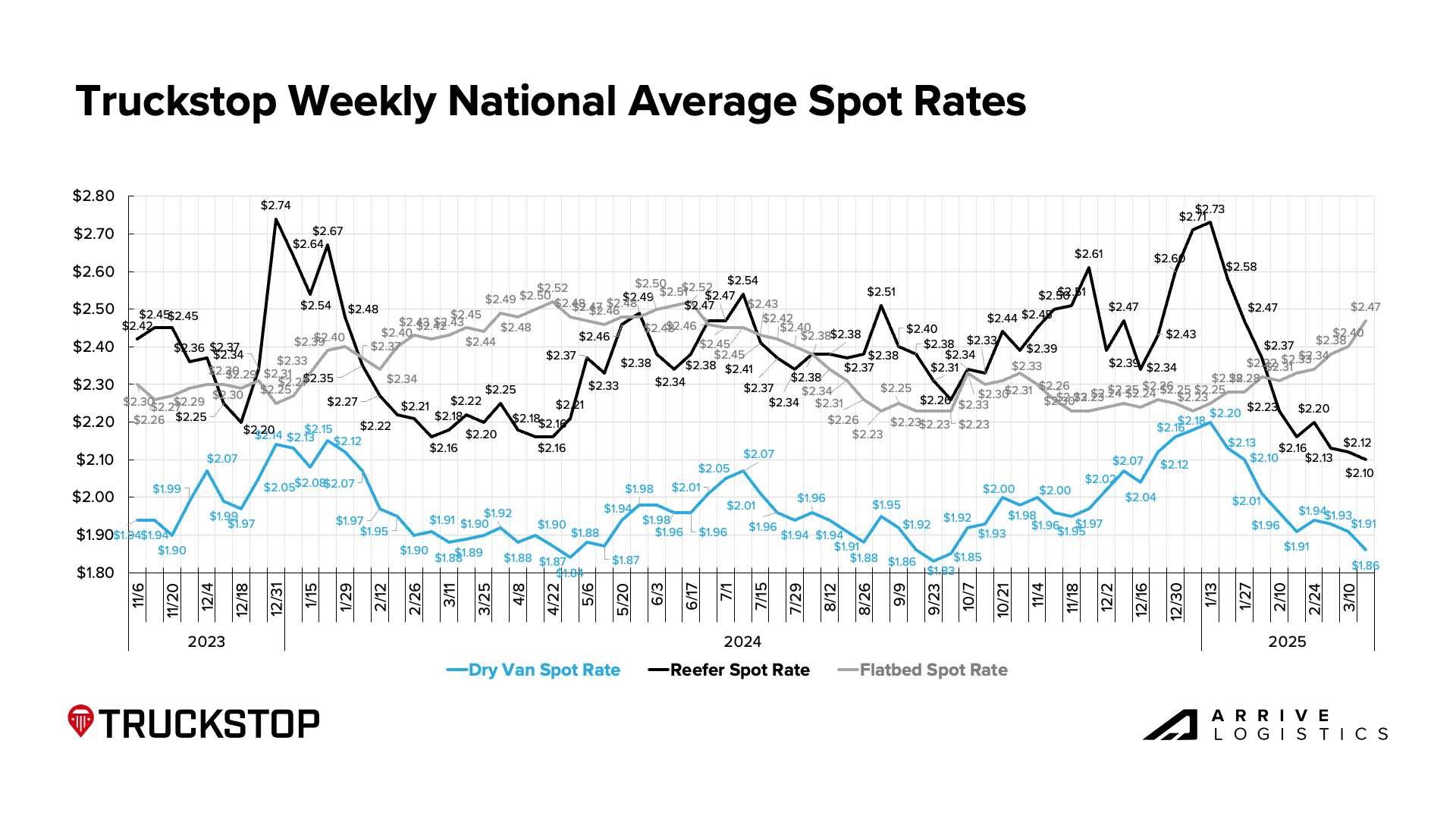

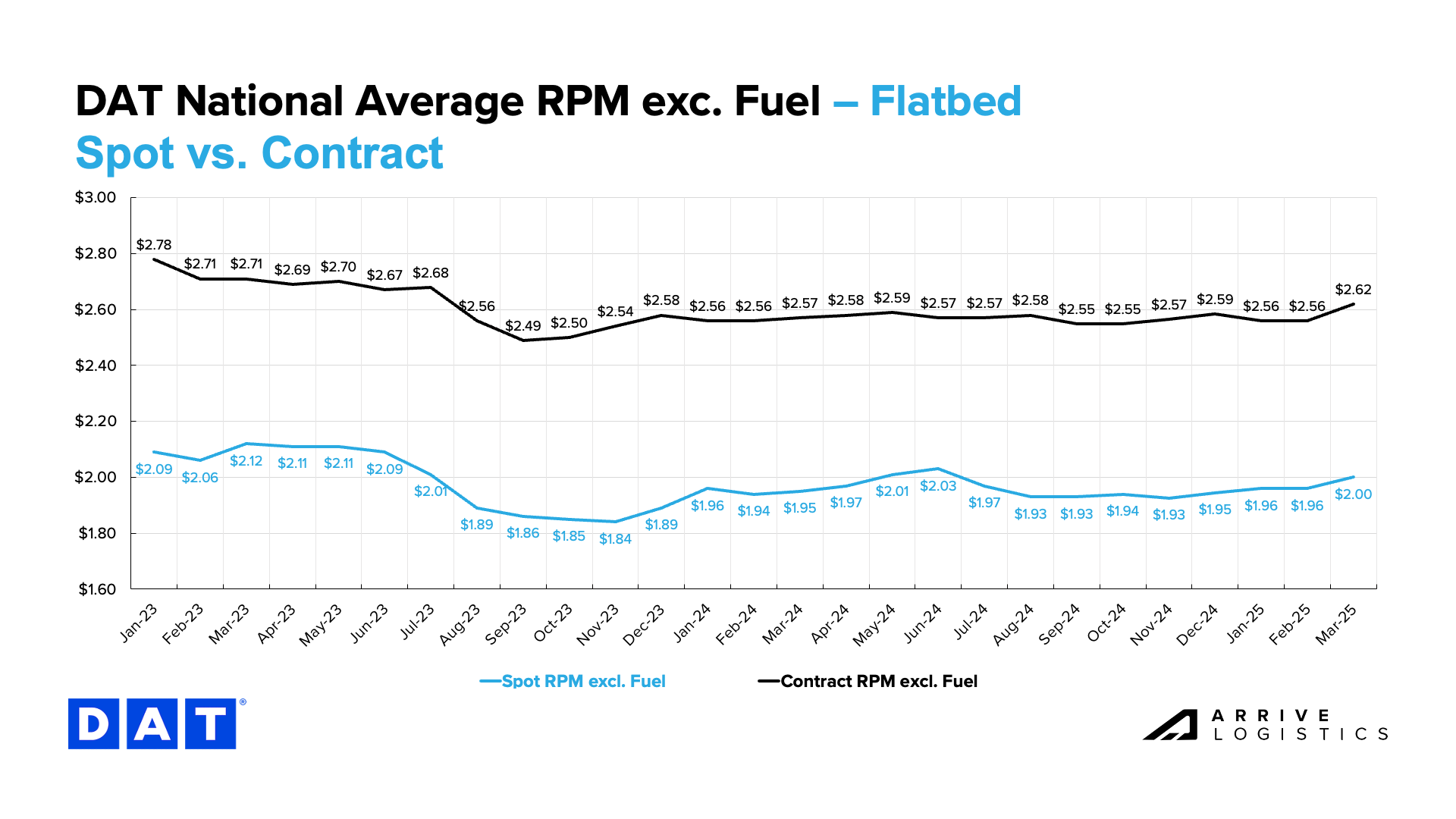

After a volatile start to the year—marked by the bullwhip effect of Q4 tariff-related pull-forward volume and severe winter storm disruptions in January—market activity eased in February and remains quiet as of mid-March. In line with seasonal patterns typical of Q1, demand, supply and rates have all softened month-over-month. However, several variables continue to complicate the near- and long-term freight market outlook.

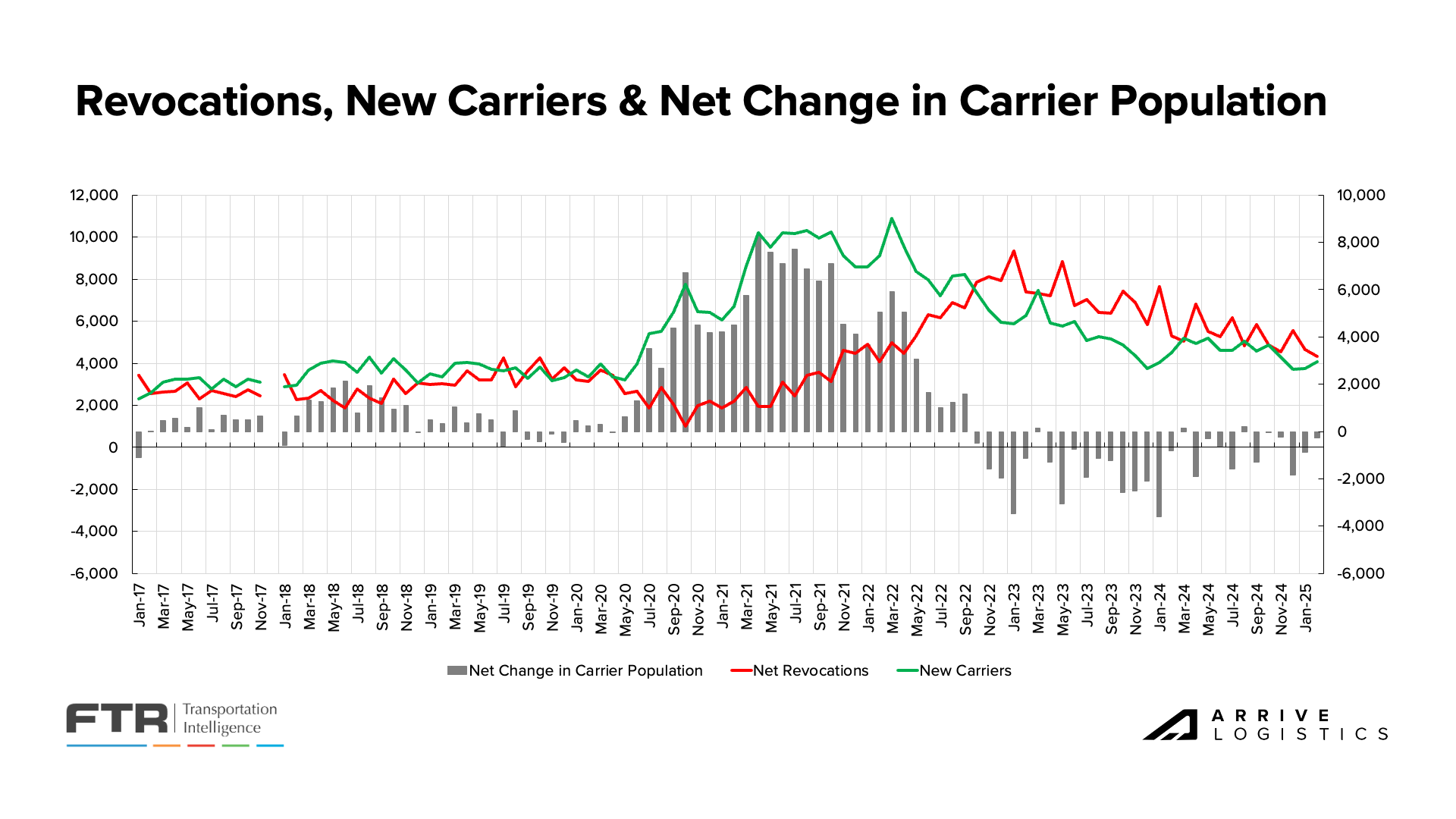

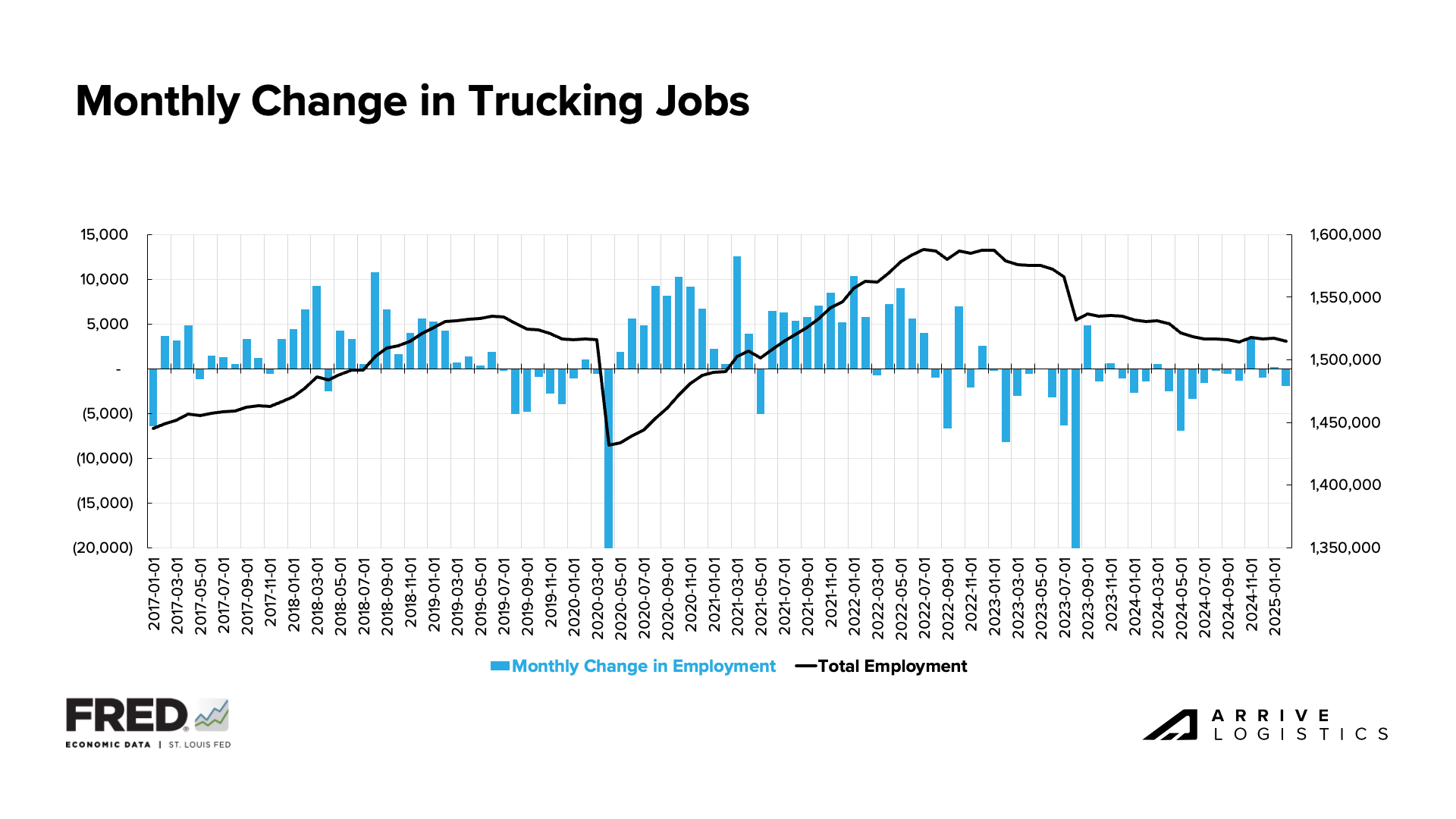

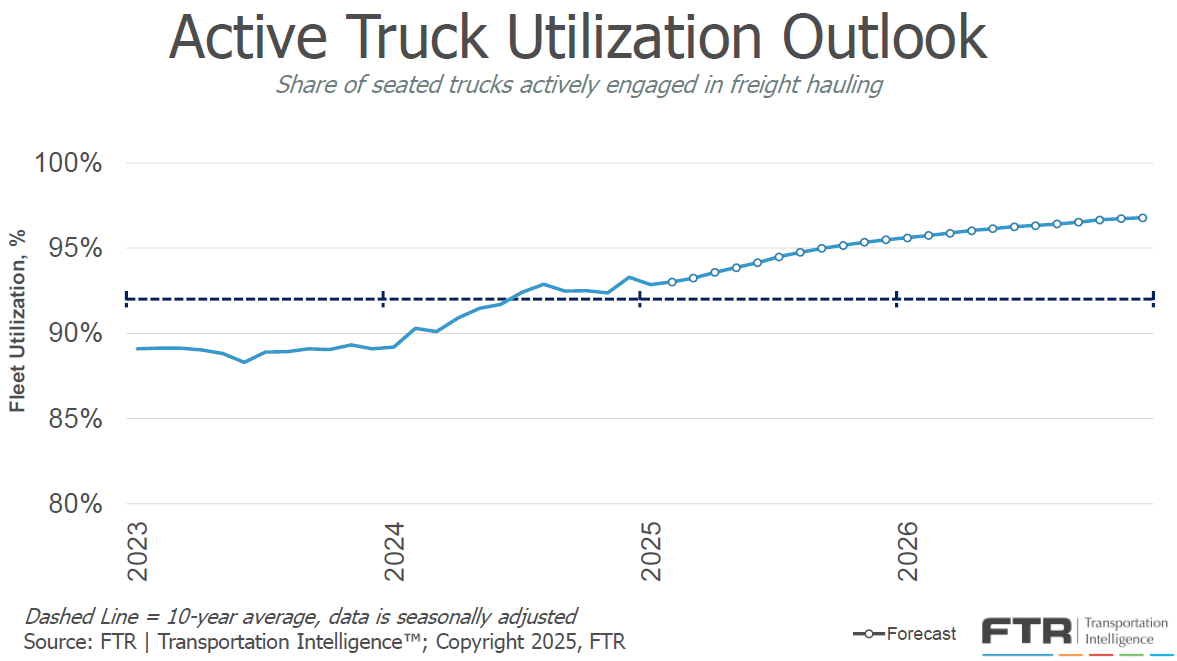

Persistently weak demand and low rates have challenged many carriers to right-size their fleets for maximum efficiency, leaving supply tighter and more vulnerable to disruption than it was a year ago. Though significant demand shocks seem unlikely in the near term, produce season, DOT Roadcheck Week and the 100 Days of Summer will all test the tightening capacity market and provide a good indication of where we stand in the cycle.

Broader economic trends are influencing consumer sentiment and, in turn, freight demand. Though spending remains relatively strong, elevated interest rates, sticky inflation and uncertainty around how tariffs might impact the price of goods have many consumers de-risking. This trend, combined with The Federal Reserve’s stance that the economy is healthy enough to hold off on additional cuts despite consumer uncertainty, creates a downside risk to demand.

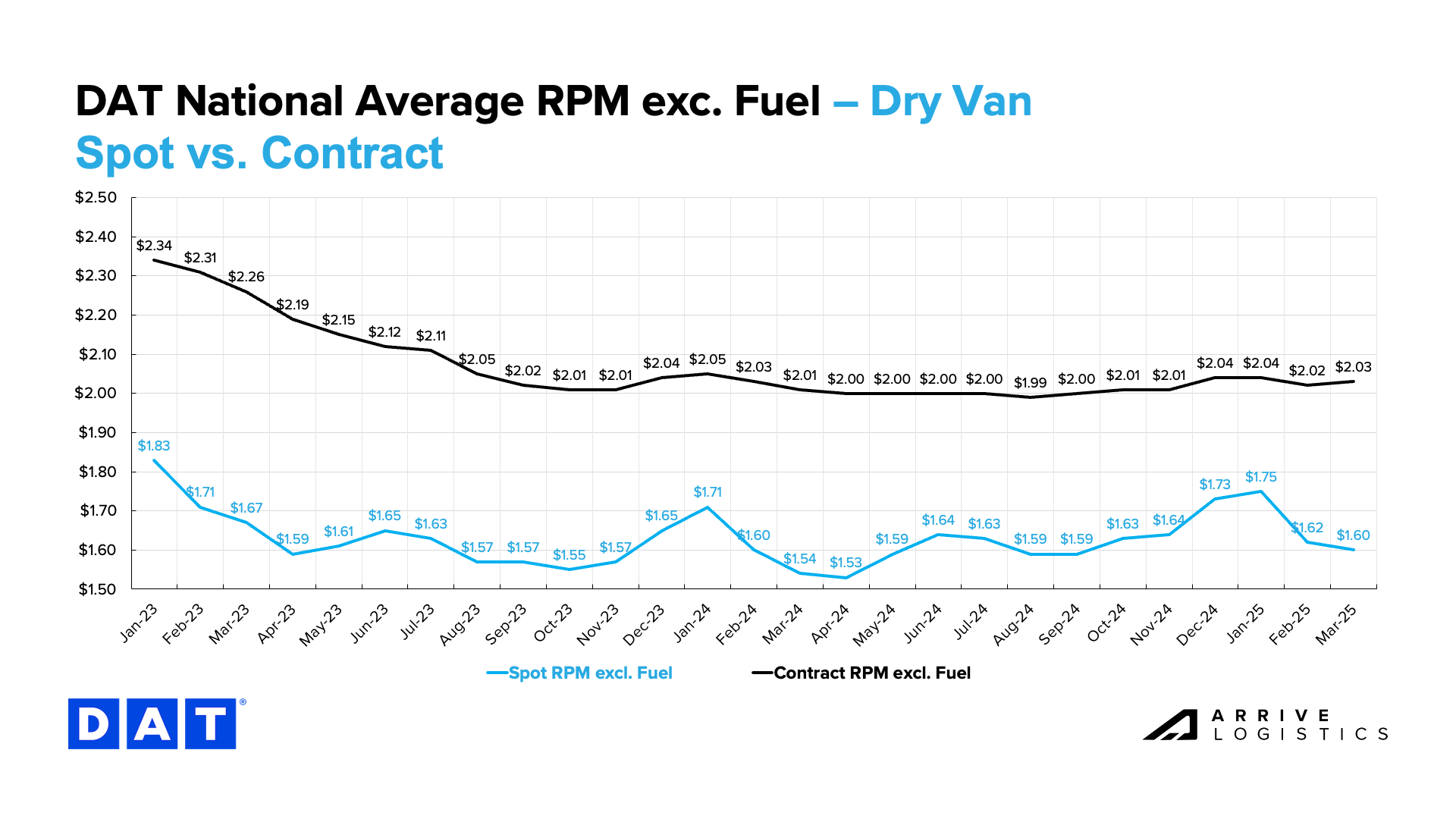

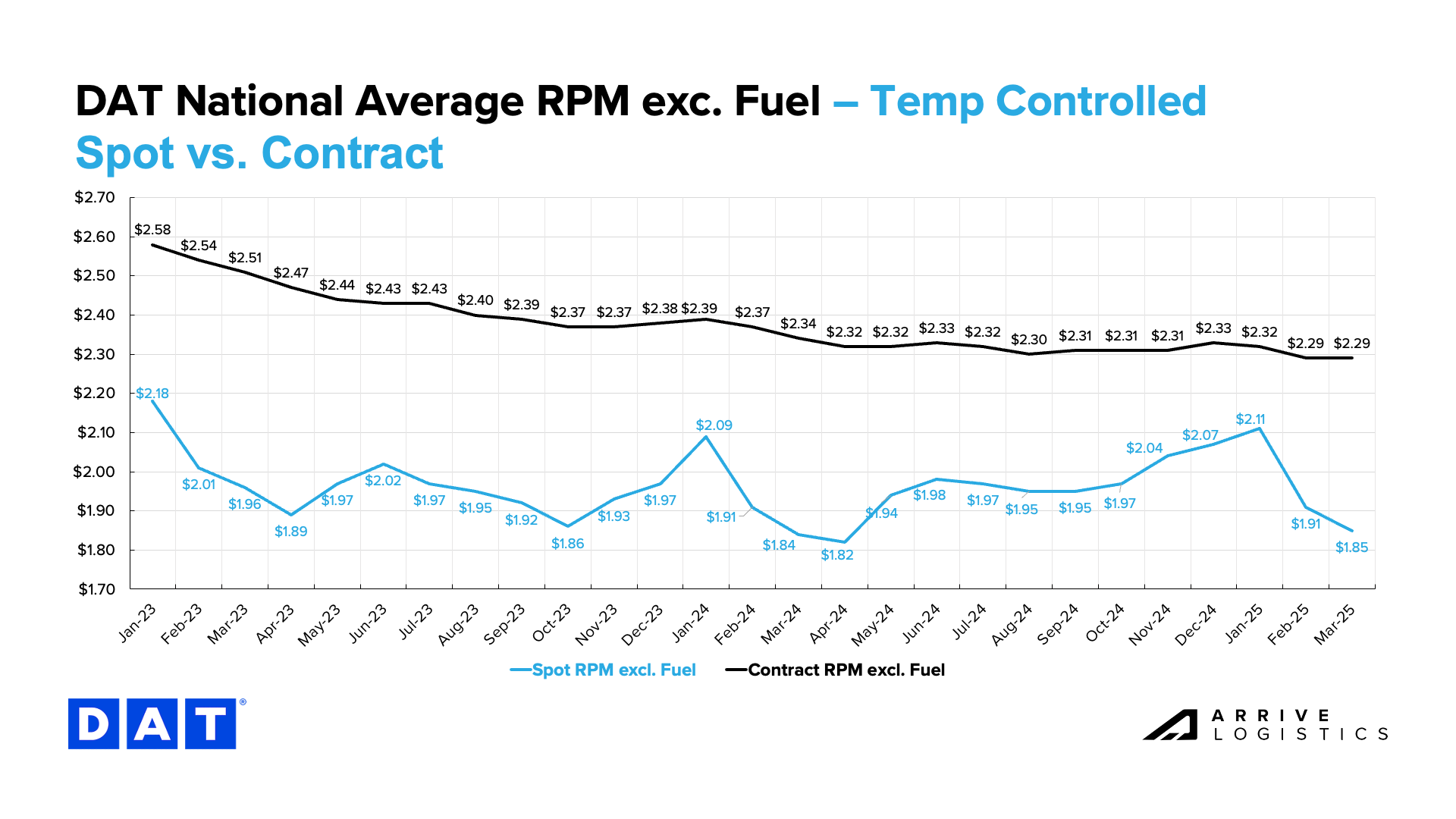

So, what does all this mean for the freight market and your business? Simply put, more of the same, at least for now. Demand should hold steady and get a helpful boost from early produce season and outdoor goods shipments, but a surge significant enough to make spot rates cross contract rates remains unlikely. However, that could change as supply continues to contract over the next few months.

Shippers can count on routing guides remaining relatively intact while these conditions last, as carriers will continue to honor contractual commitments. Those moving freight outbound from southern regions should expect some rate increases as capacity tightens with the start of produce season, but any volatility should be short-lived.

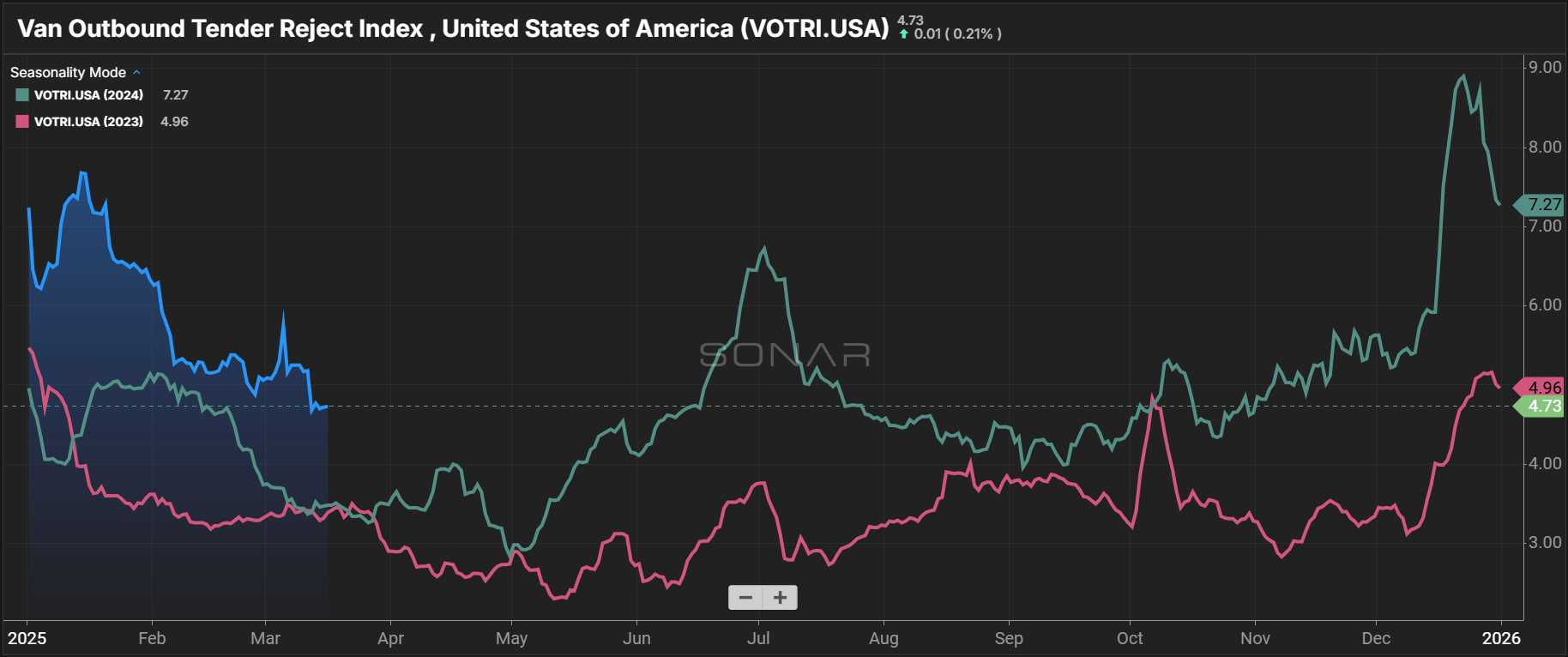

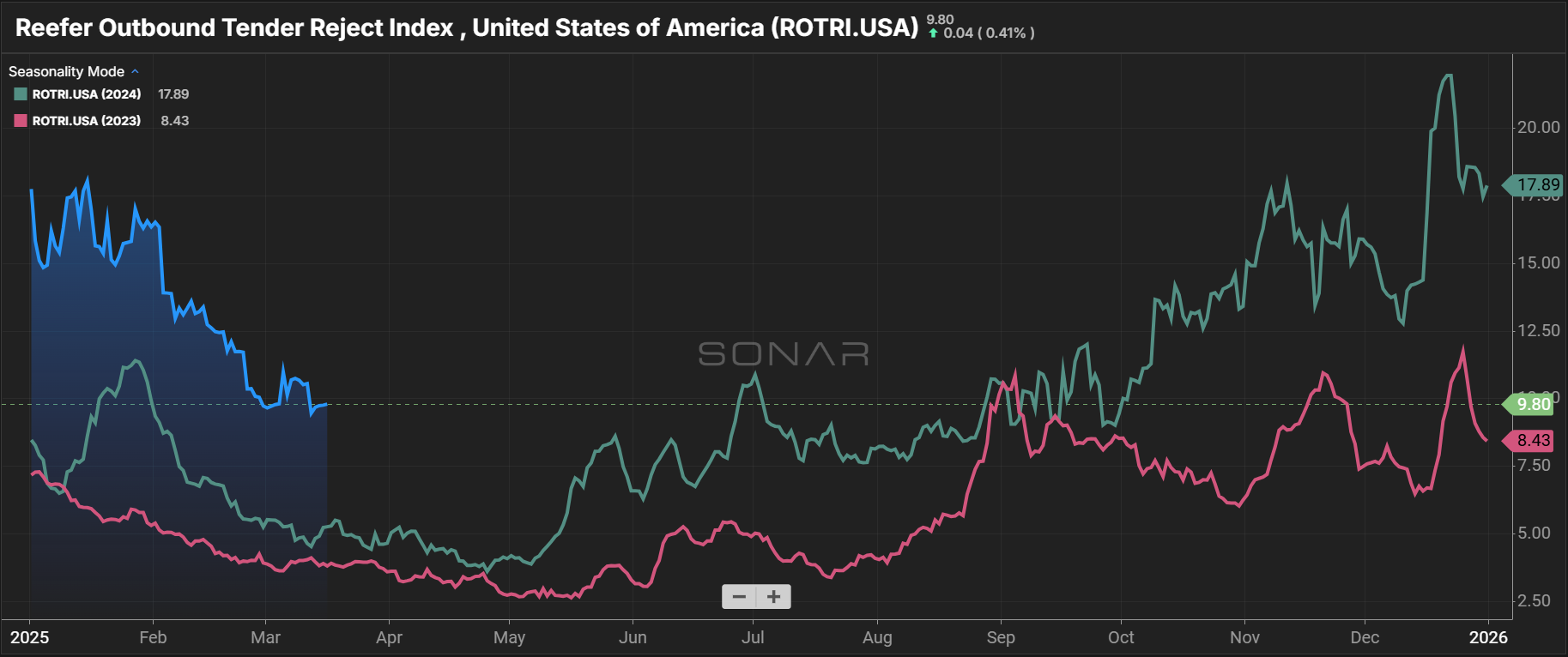

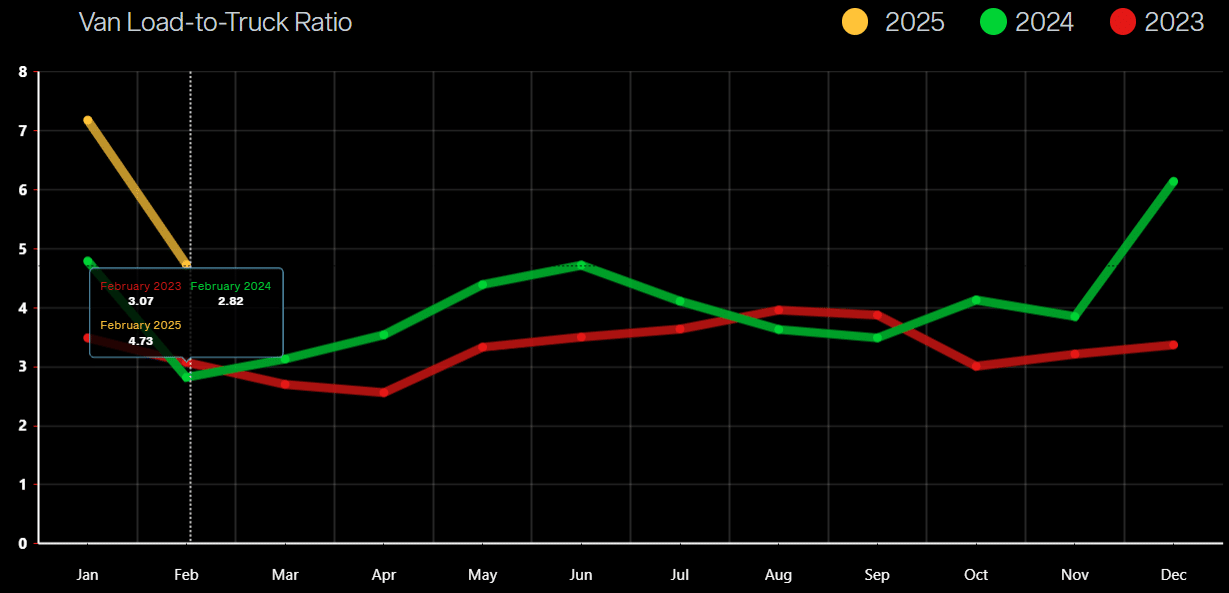

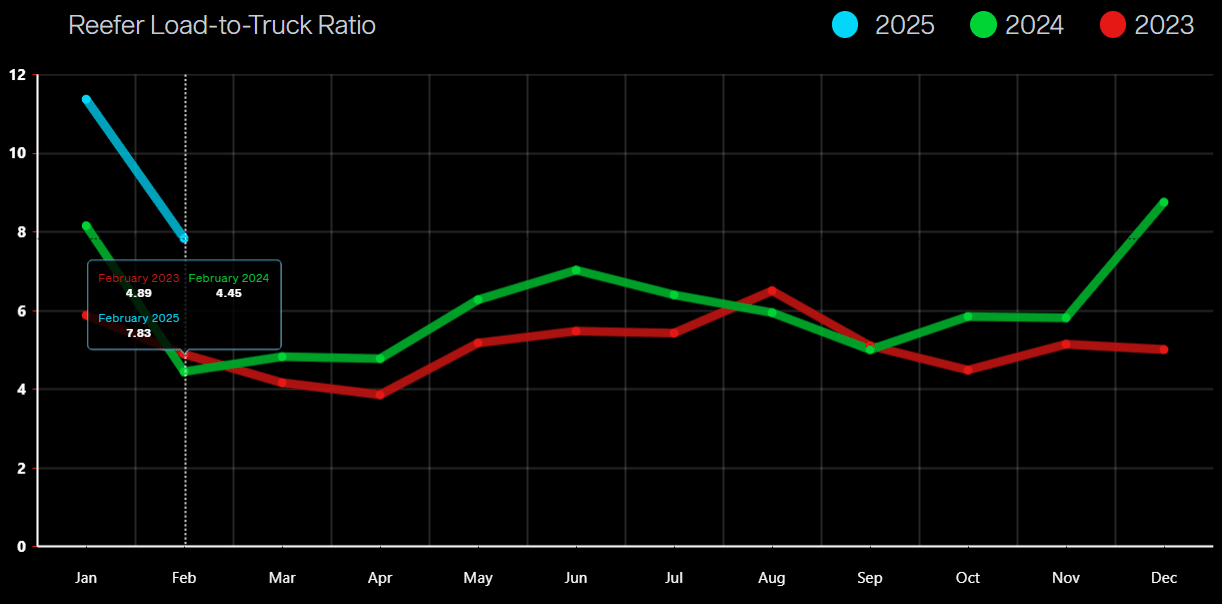

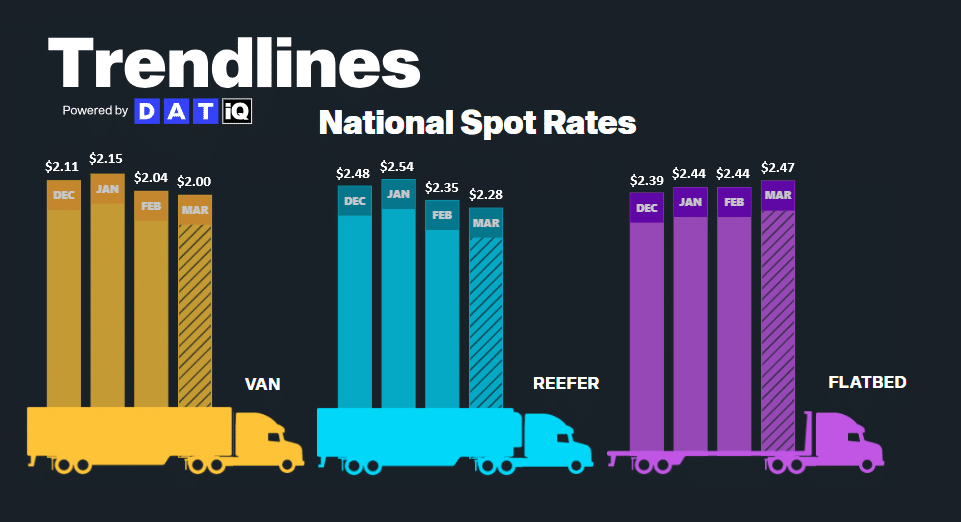

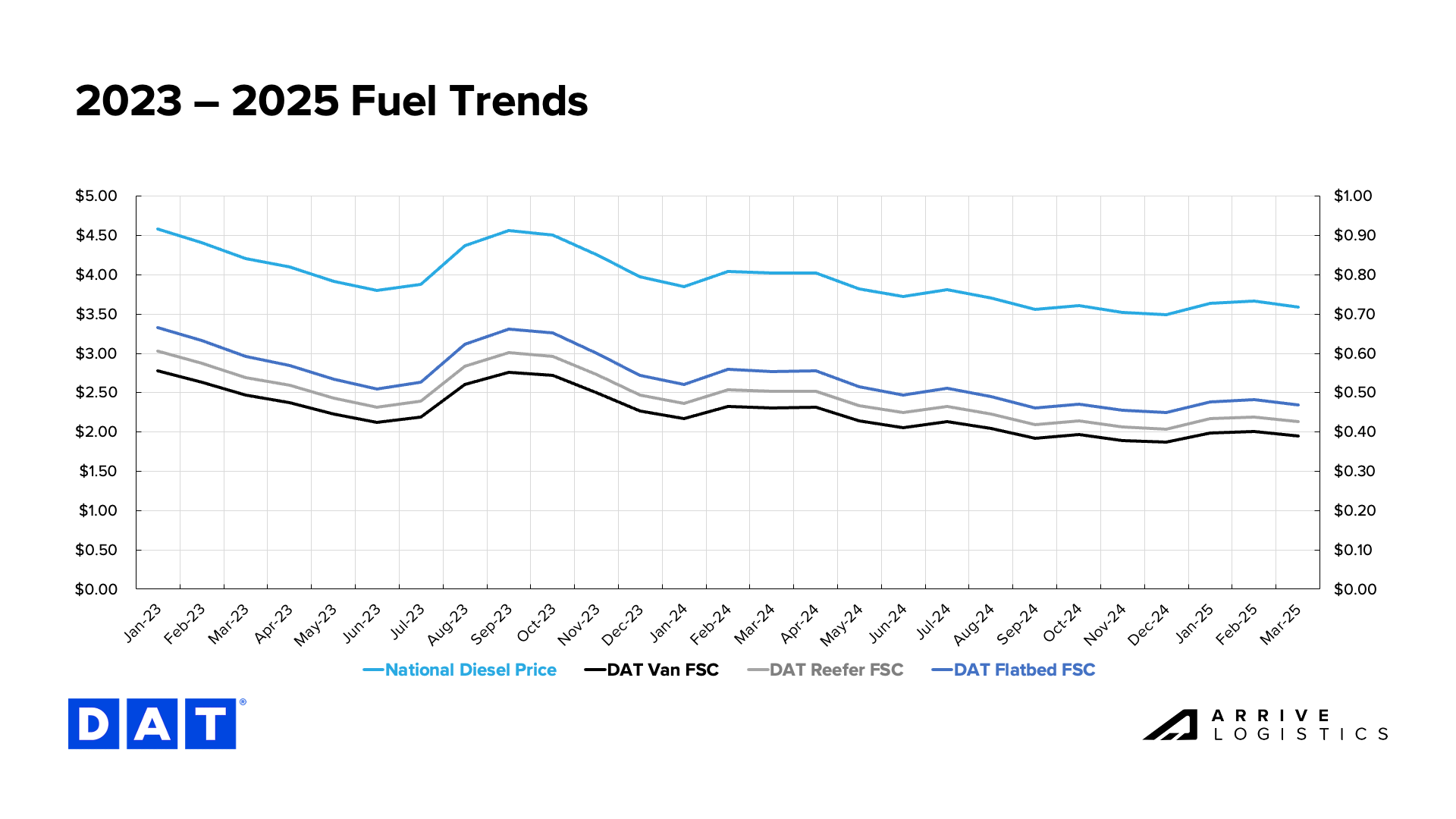

For a closer look at the data driving these trends and insights into the potential implications, keep reading.