Tariff policy conversations have taken center stage in recent months, with speculation about demand destruction dominating media headlines as shifting trade dynamics create strategic complexities for supply chain stakeholders.

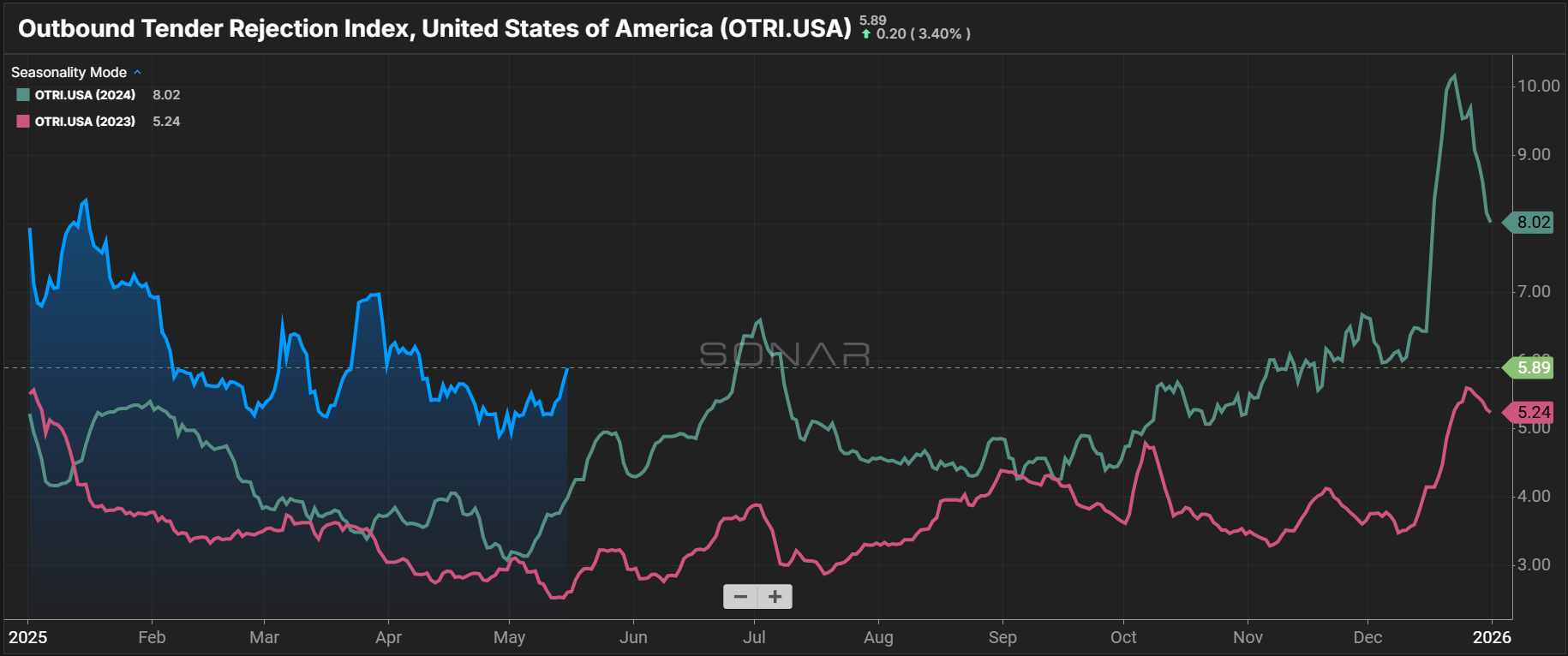

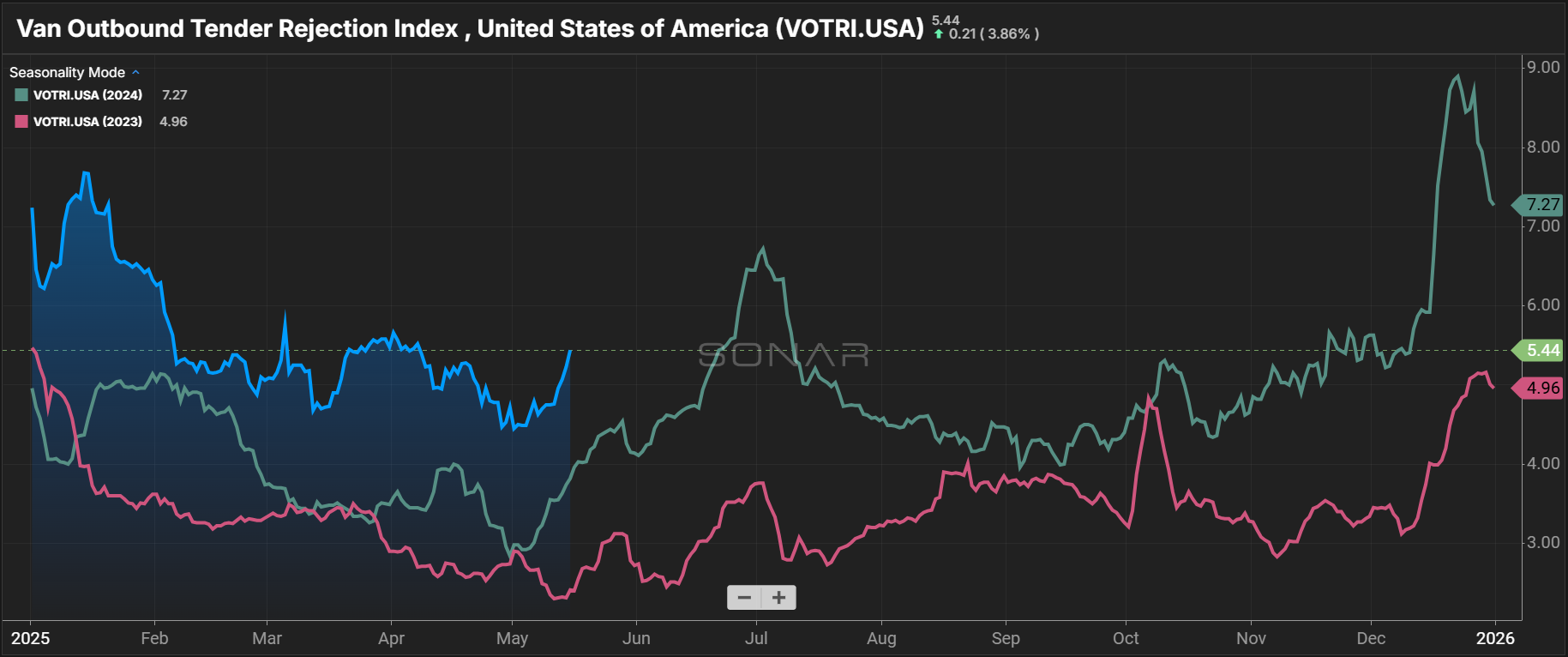

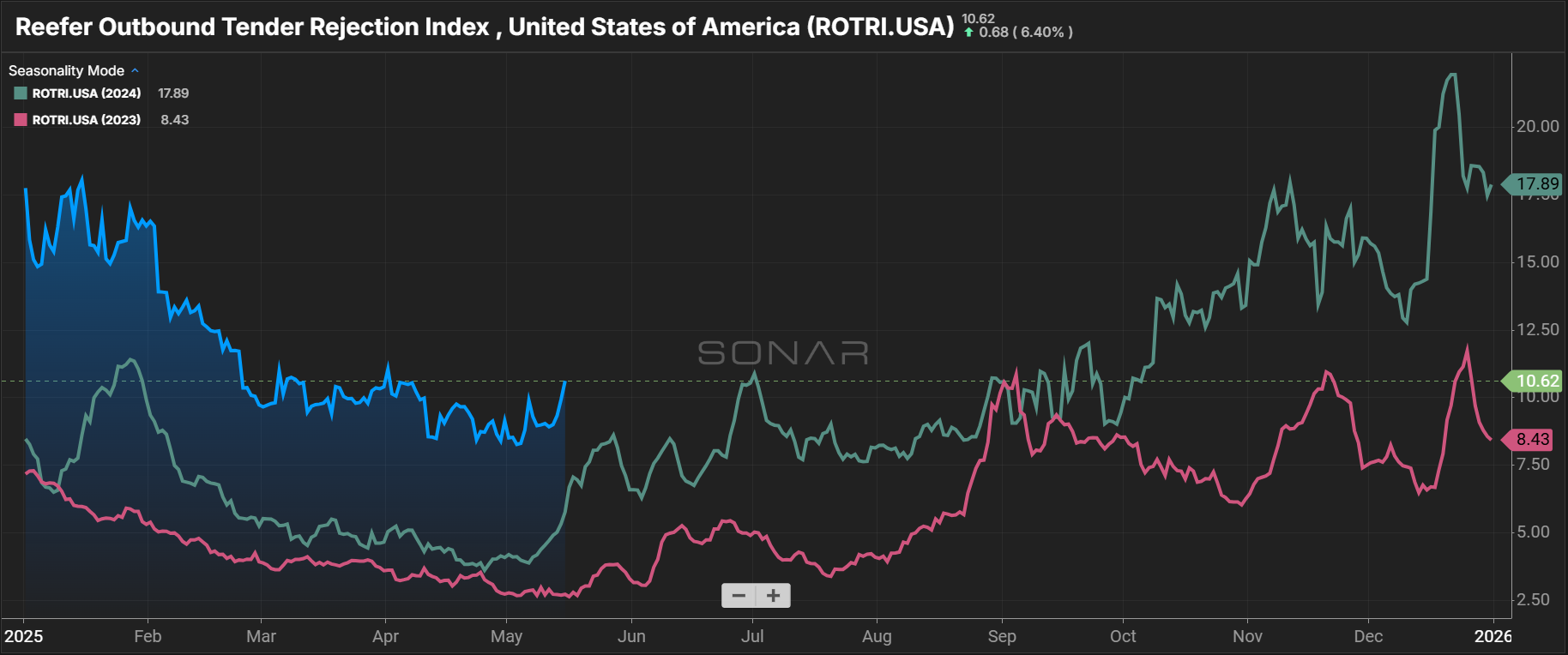

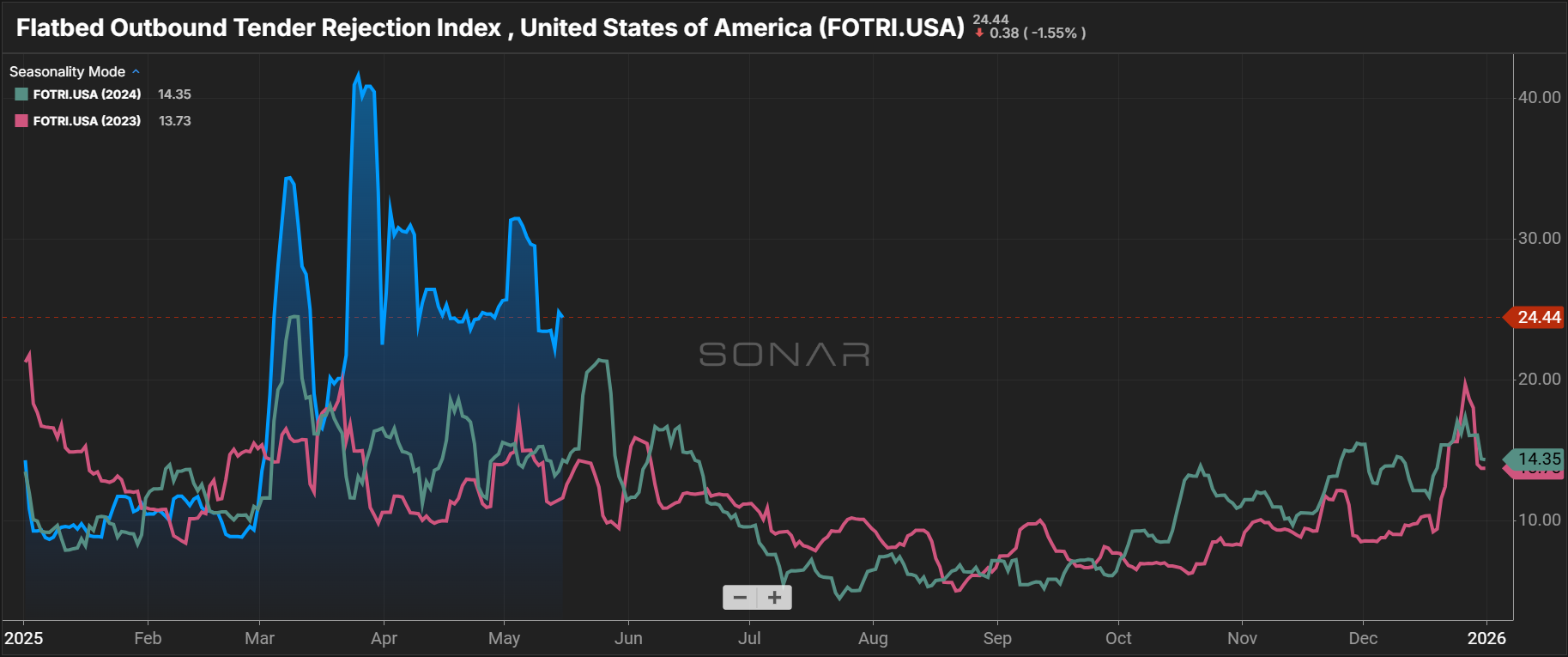

While the stop-and-start nature of elevated tariffs has created some abnormal freight movements and periods of regional volatility, the data tells a more nuanced story. In fact, the prevailing market narrative remains one of typical seasonality amid ongoing rebalancing—and that’s likely to continue for as long as demand levels hold.

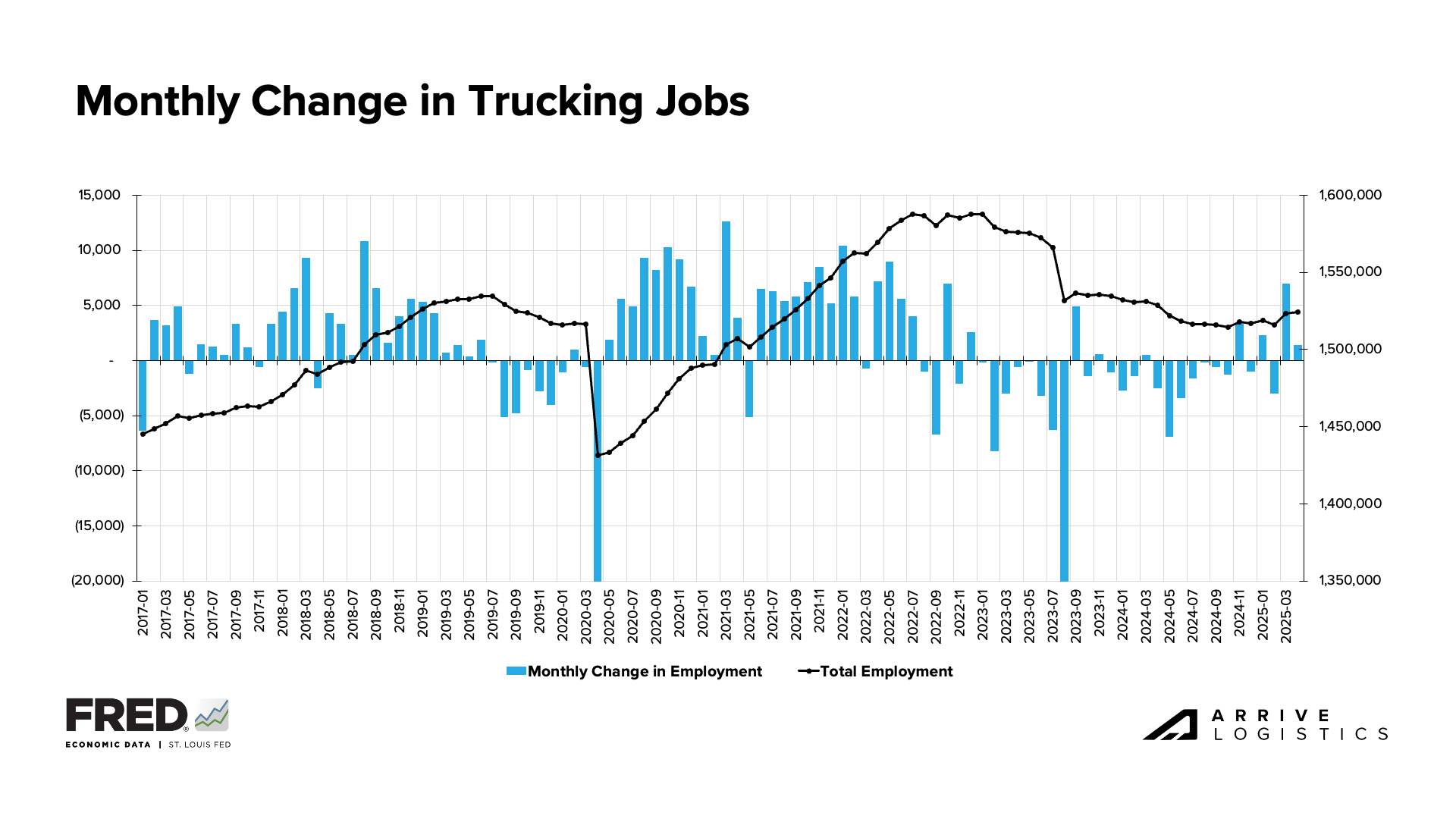

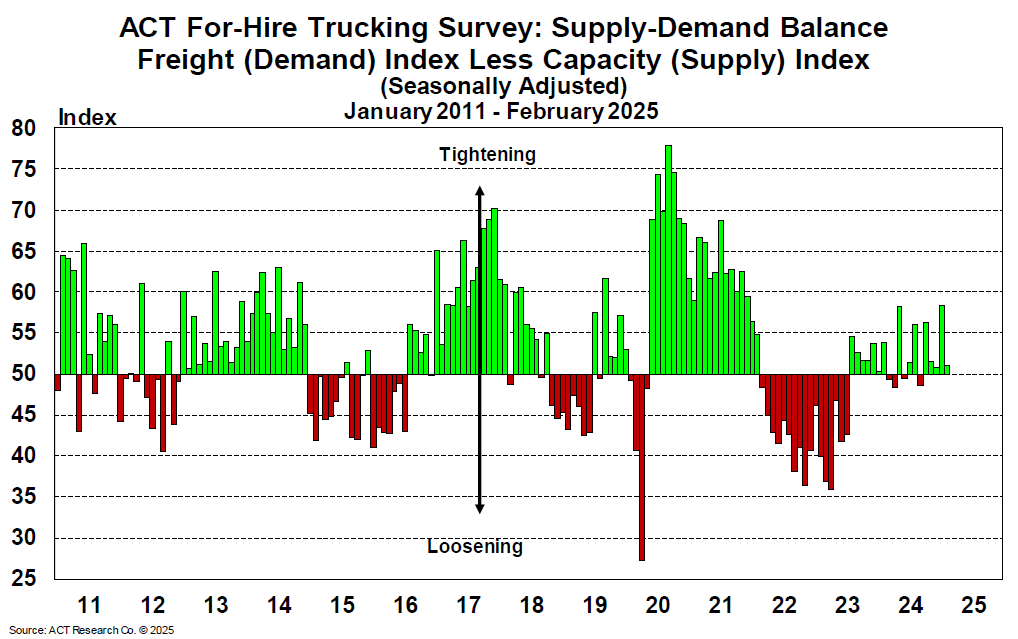

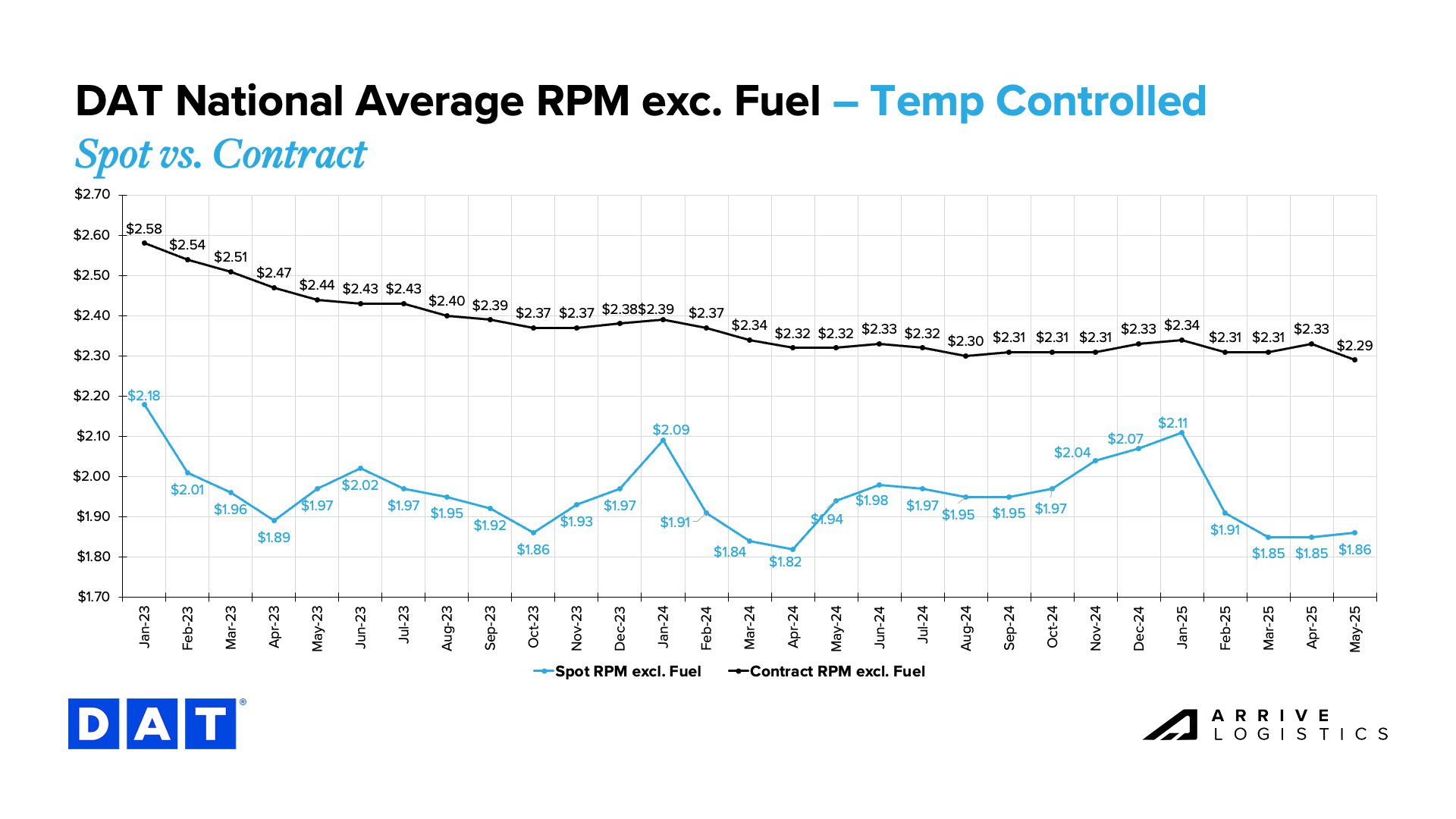

April and early May supply indicators confirm that narrative. Capacity tightened as equipment went offline during the Commercial Vehicle Safety Alliance’s (CVSA) Roadcheck Week alongside increased early peak season spot activity, supporting our position that supply has become more vulnerable to upside demand risks.

If the trade war de-escalates and economic indicators improve, those risks could soon materialize. But if negotiations reverse course and demand dramatically softens, supply would contract in turn, leaving the market more vulnerable to disruption when volume returns.

As that story unfolds, some shippers are using this window to reevaluate supply chain and production strategies, such as reformulating SKUs to reduce reliance on tariff-exposed suppliers. Freight flows are also being reshaped in ways that will keep stakeholders on their toes. For example, new lanes and shifting demand patterns are reconfiguring capacity networks, driving further change in an already dynamic environment.

As the market responds to these pressures, the year-end picture will continue coming into sharper focus. While shippers will face varying levels of tariff exposure and must navigate accordingly, peak season should otherwise be business as usual. Beyond that, patience, planning and strategic preparation around evolving trade policy and capacity shifts will be key to managing risk on the road ahead.

For a closer look at what’s happening across demand, supply and rates, keep reading.