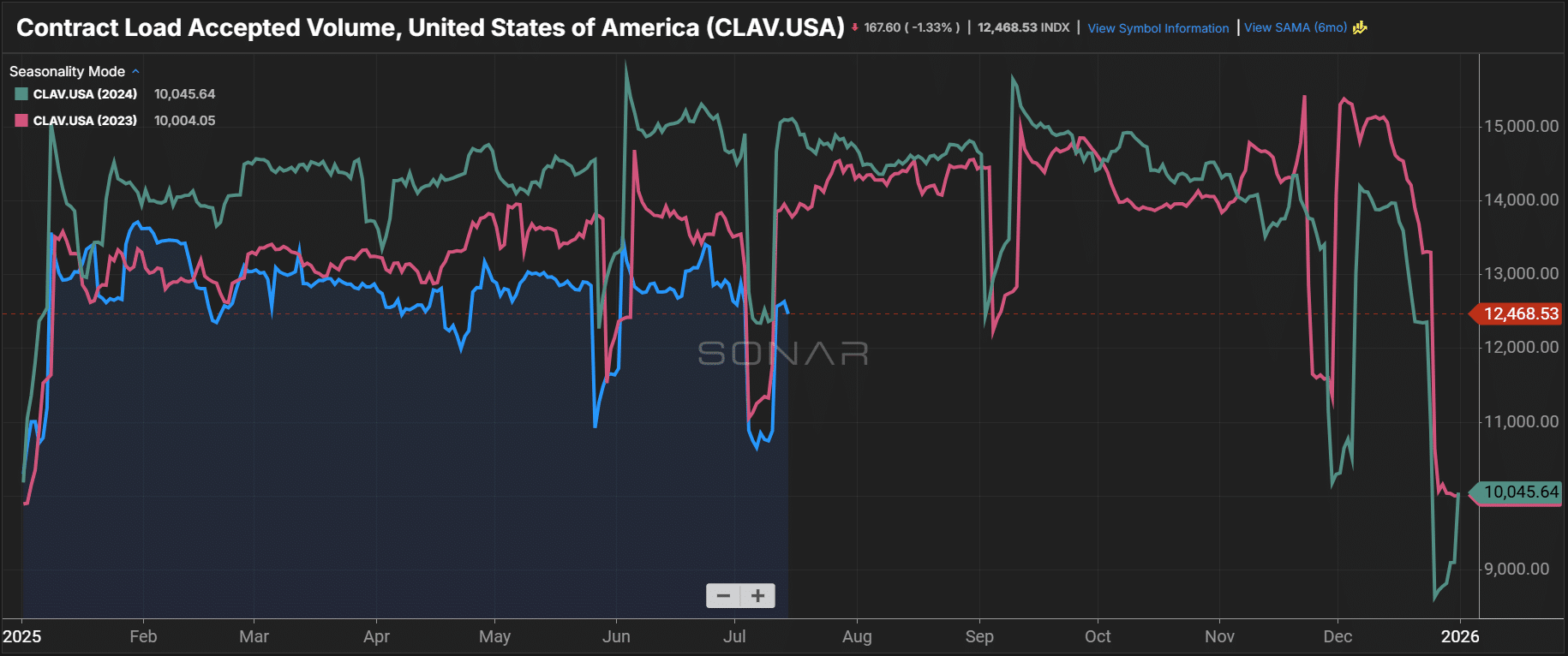

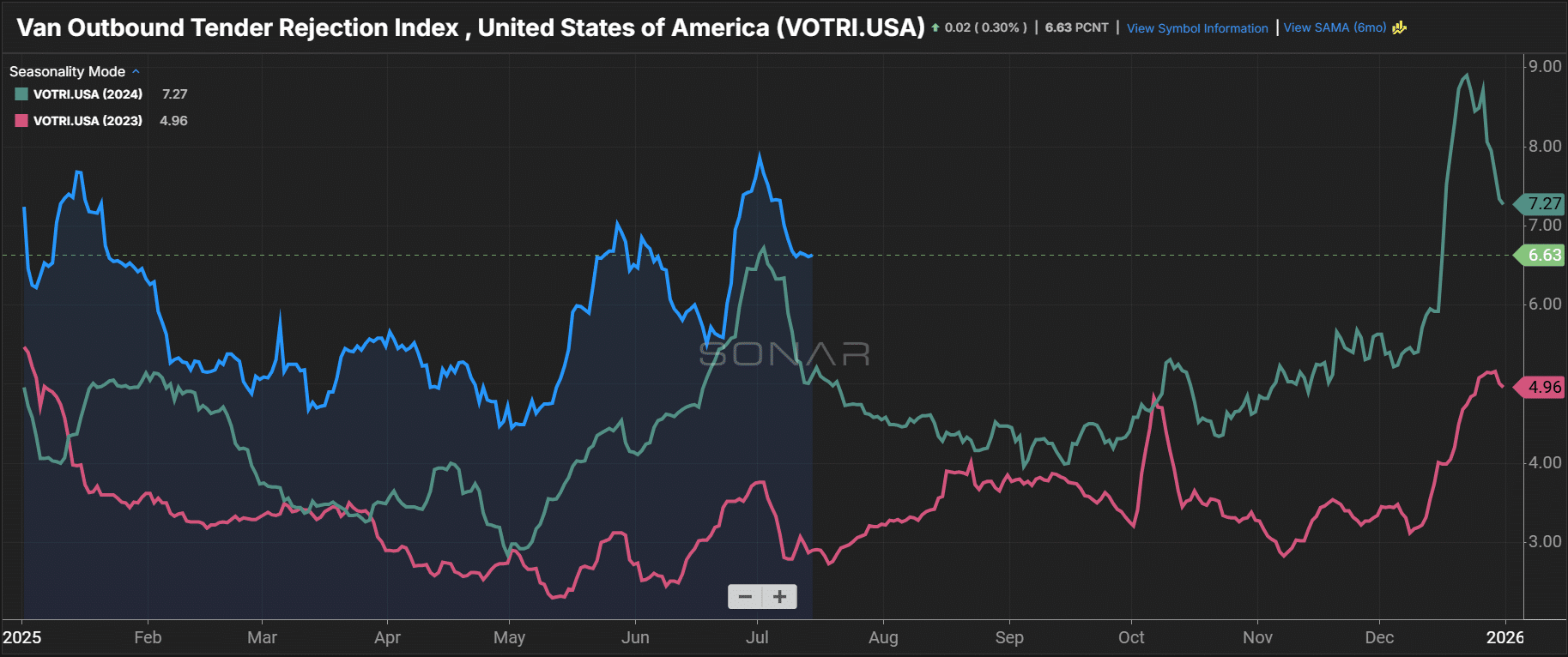

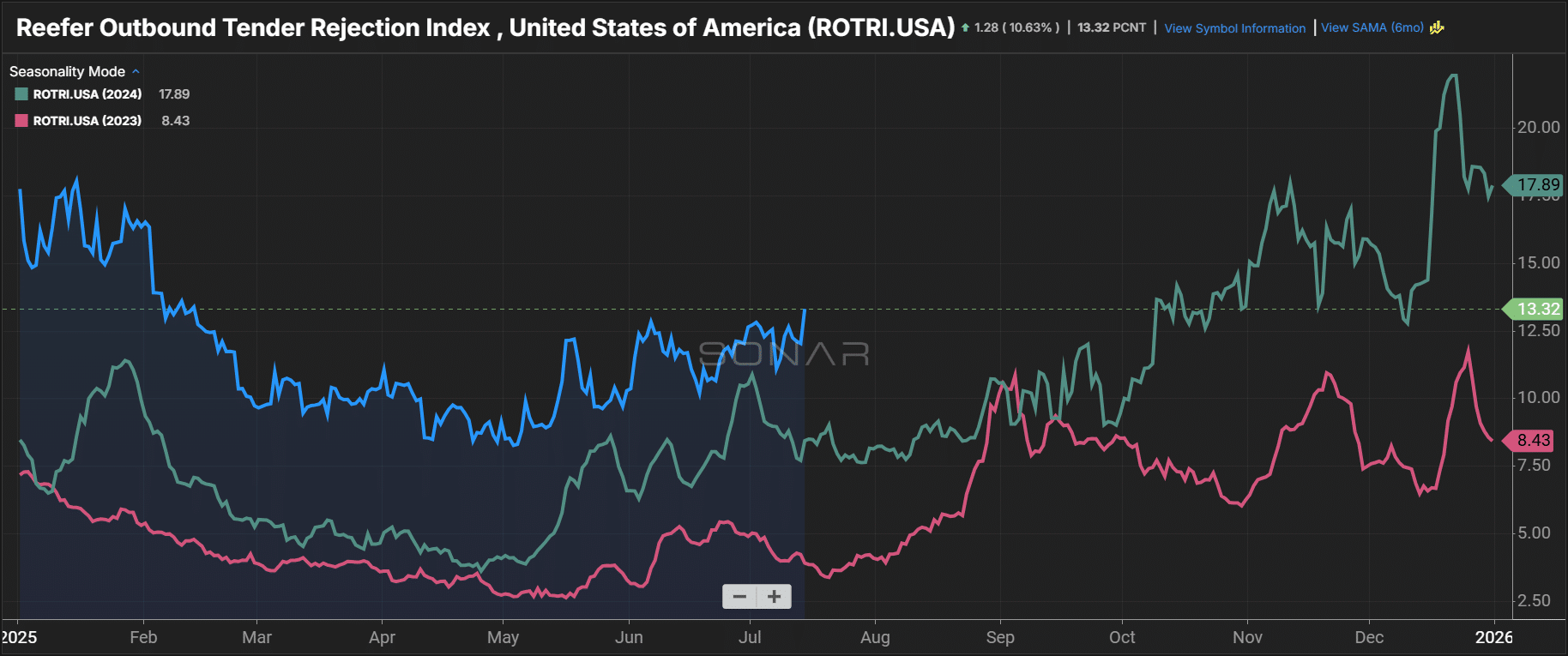

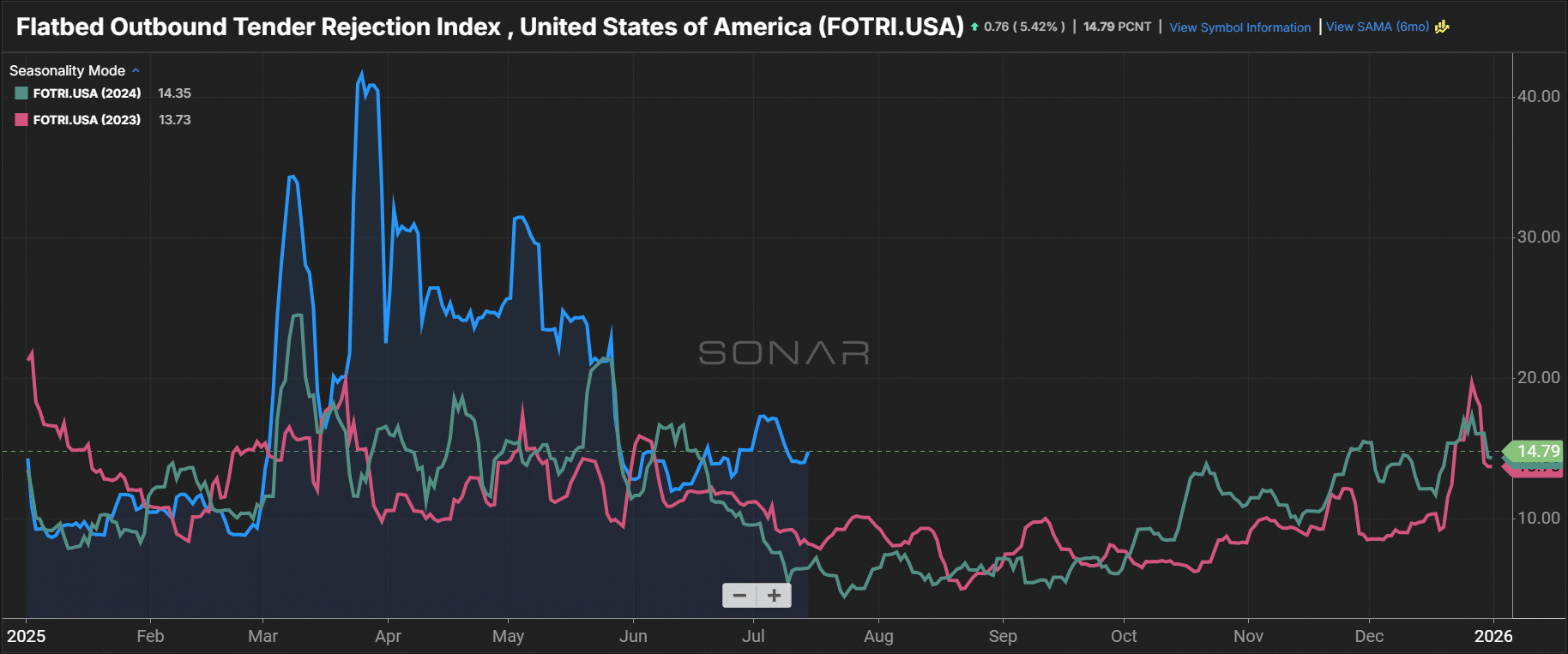

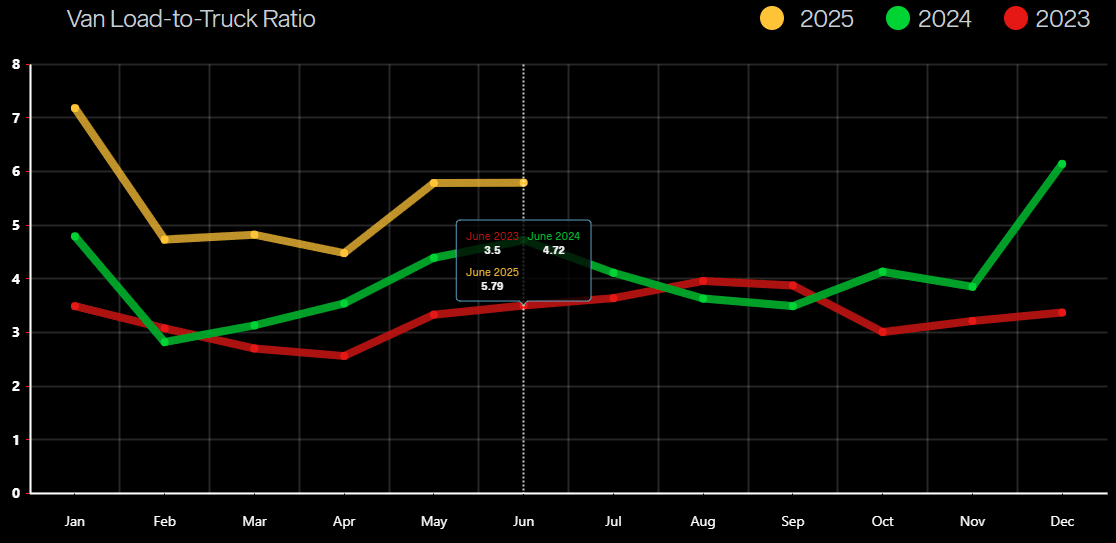

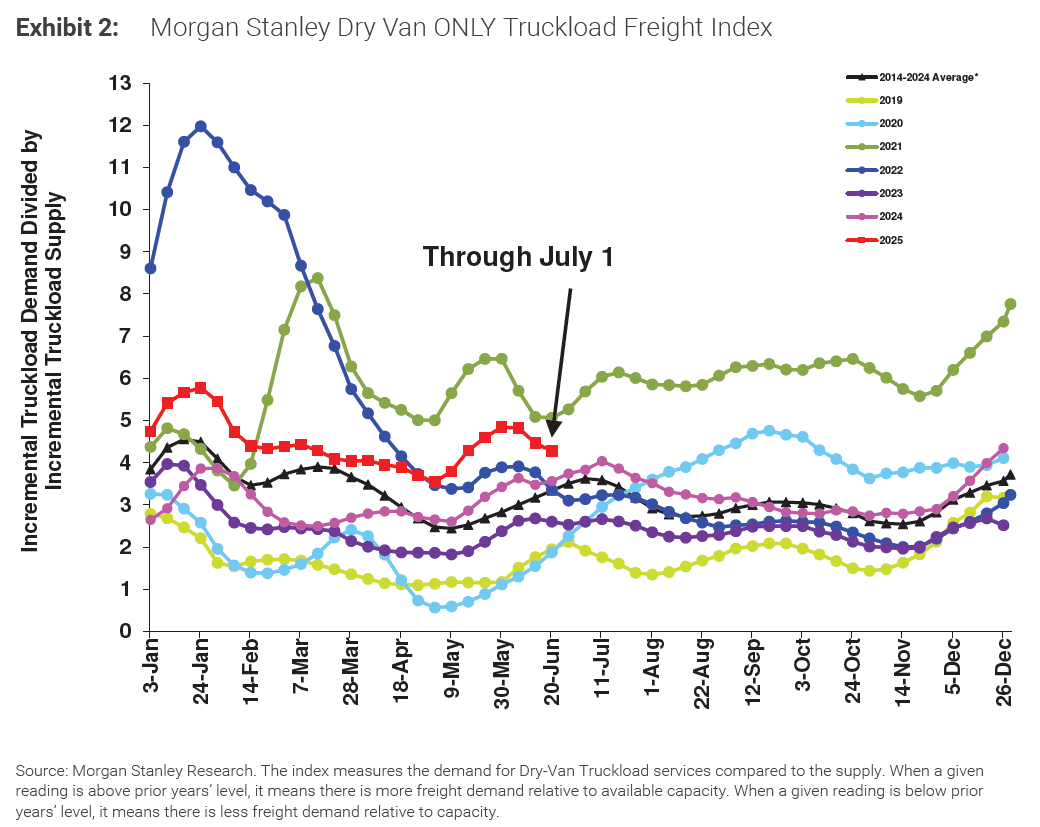

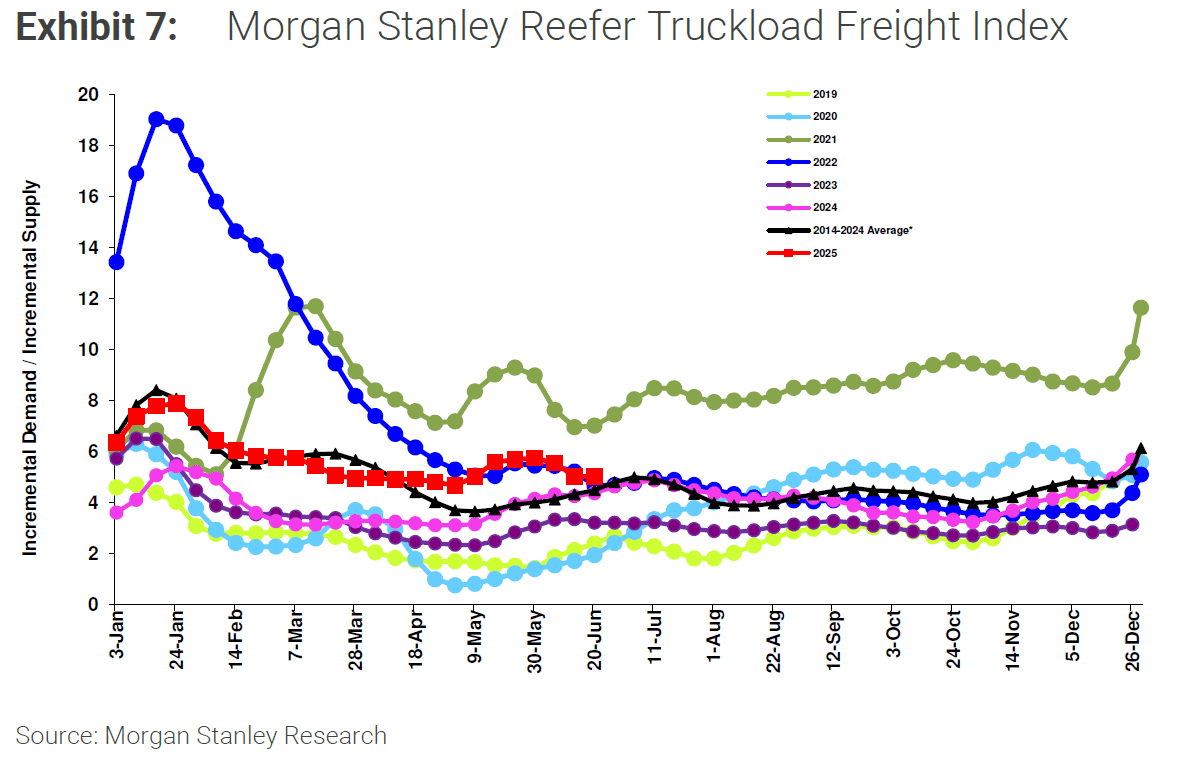

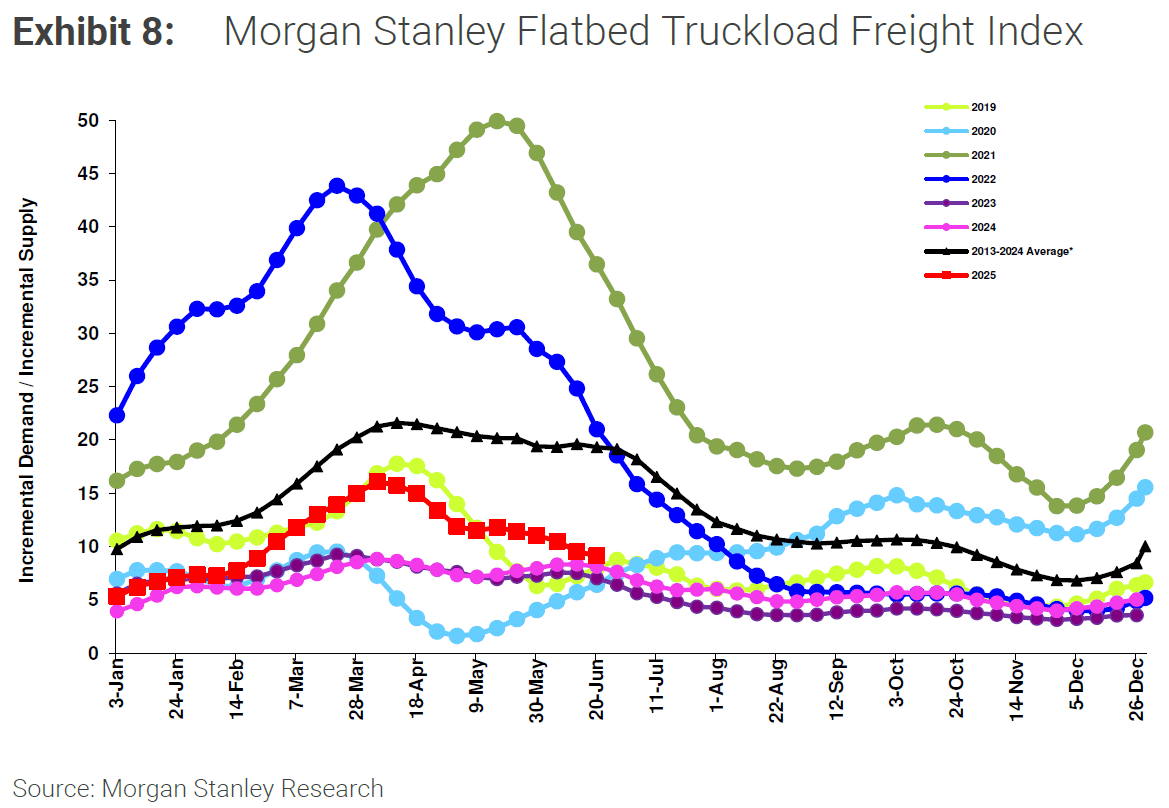

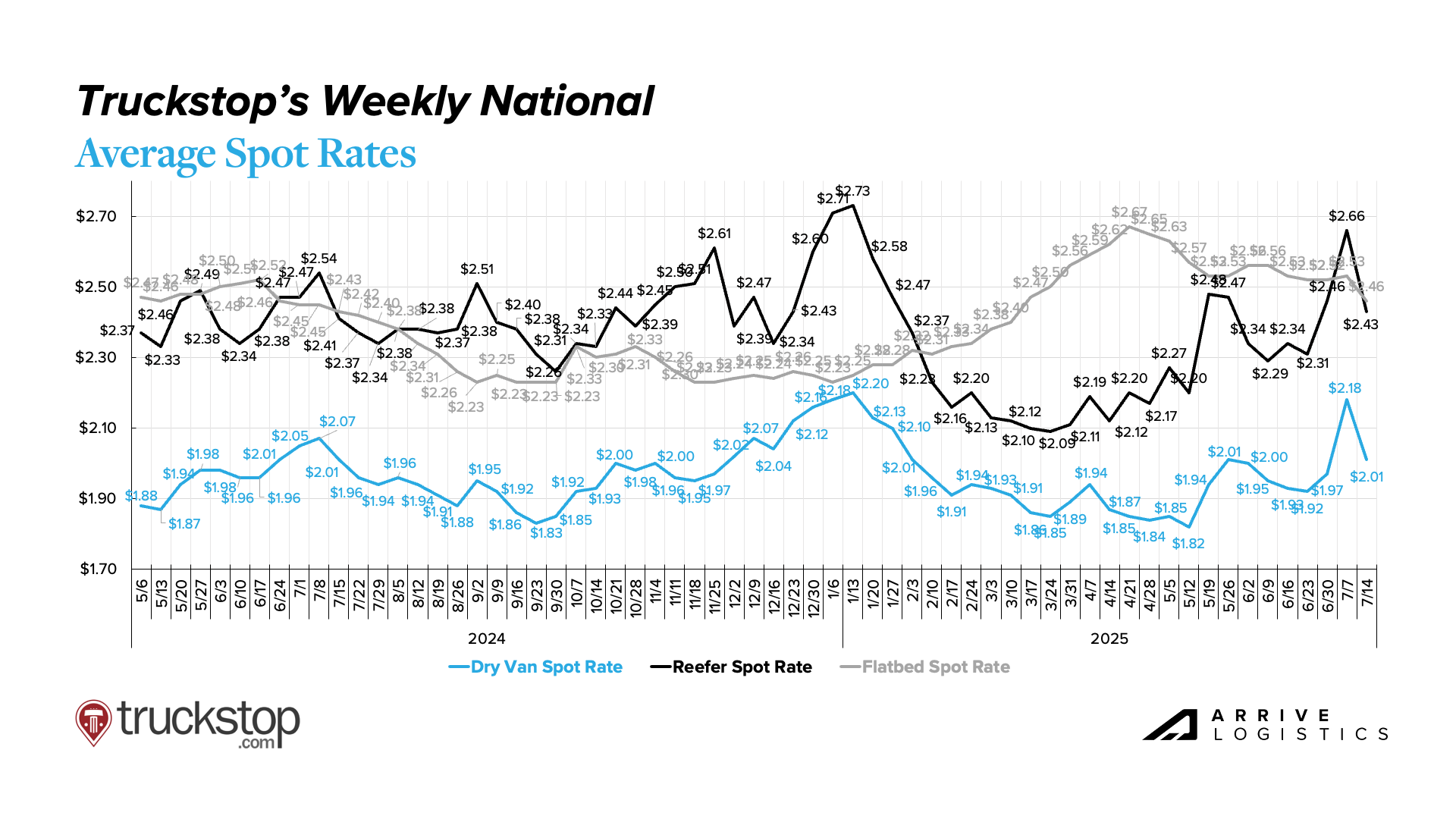

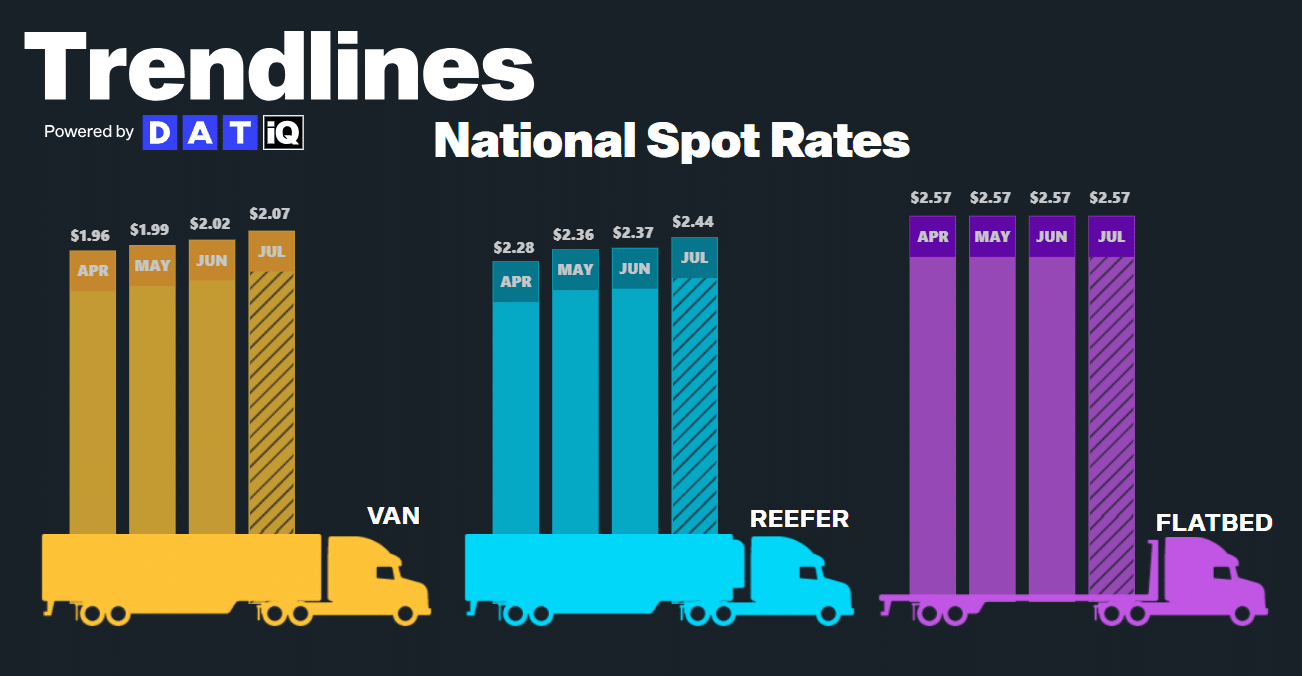

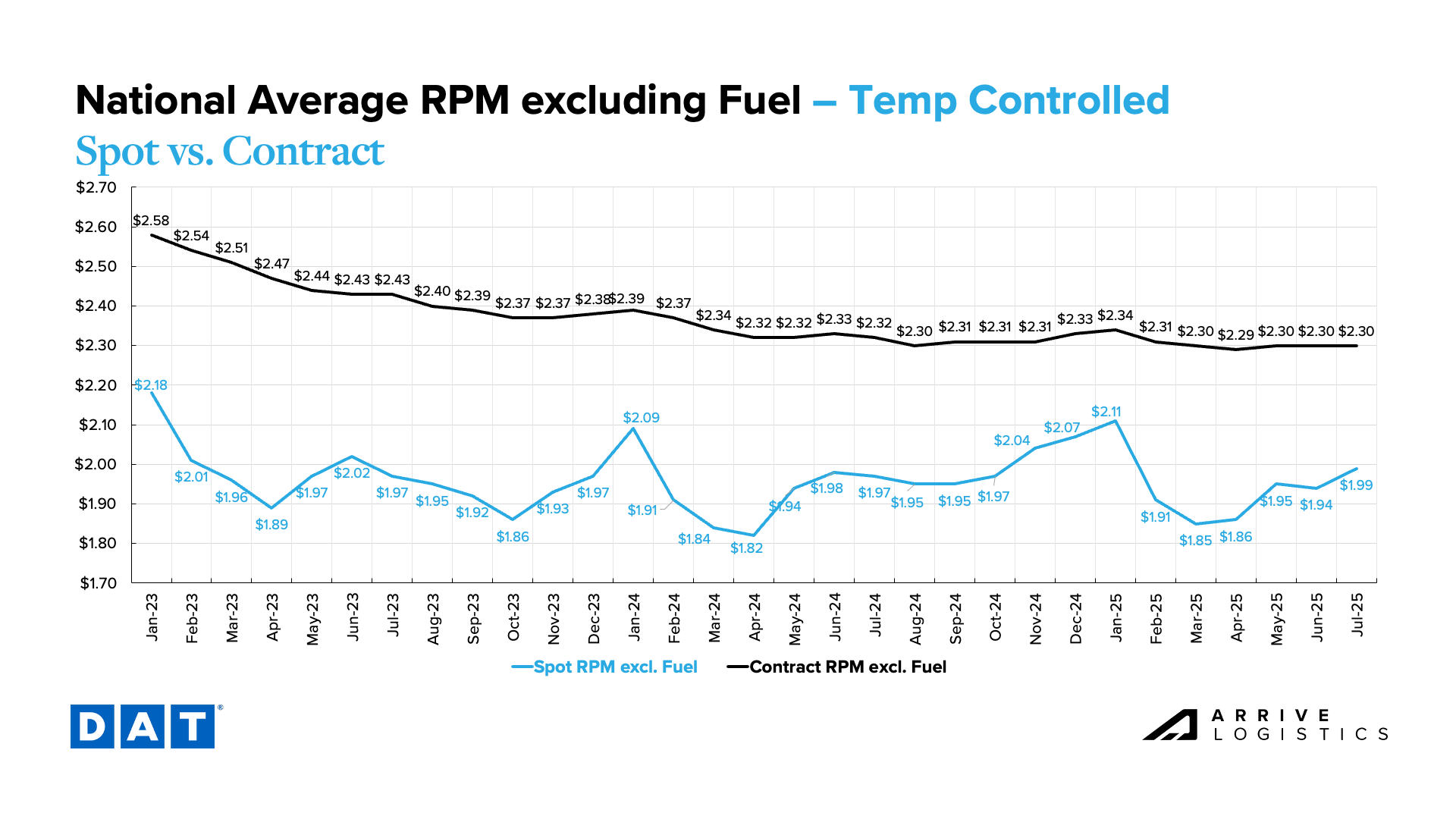

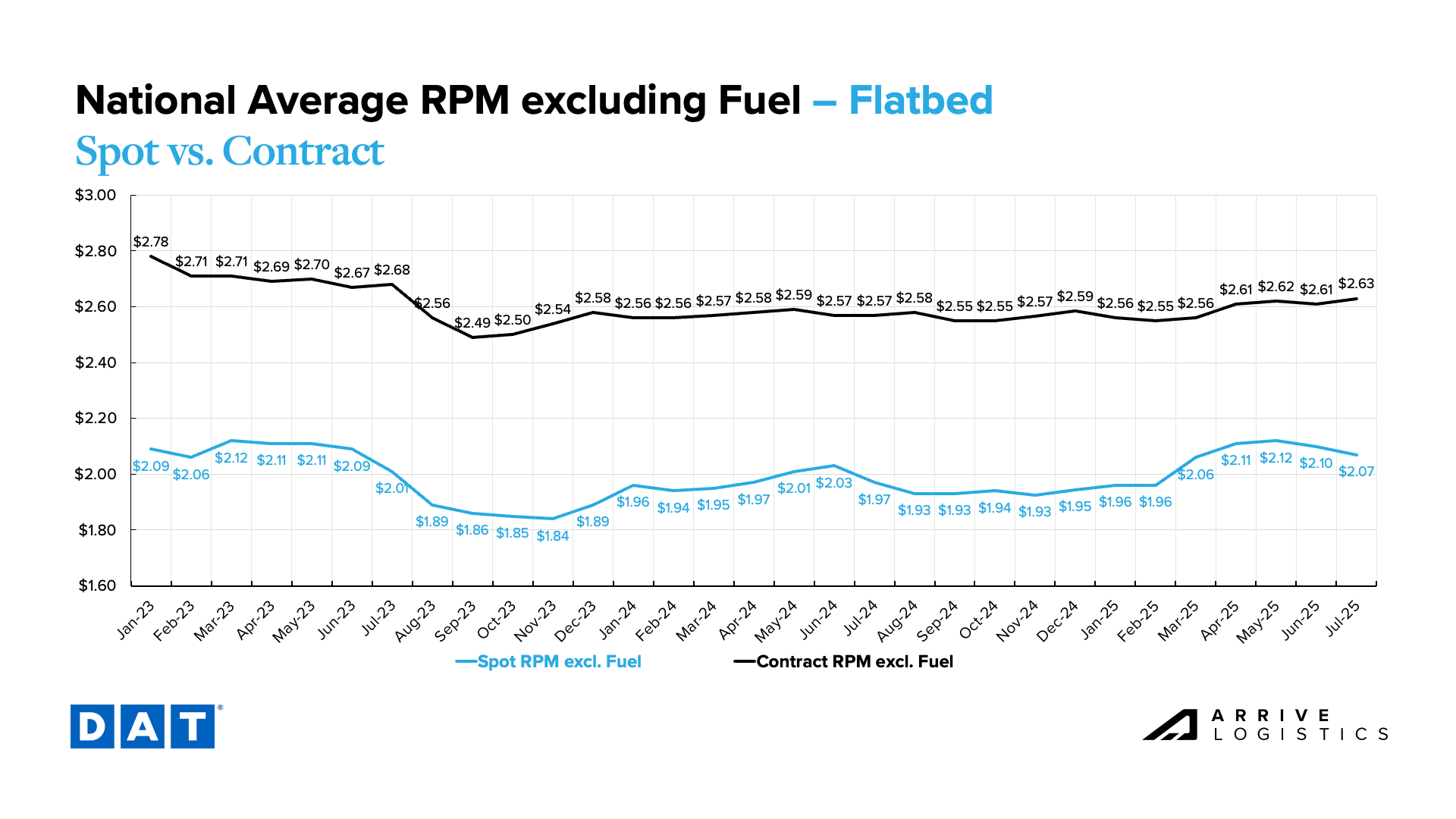

The summer peak season is one of two key litmus tests for the freight market, but a number of variables at play this year made for somewhat complicated results.

Coming off a June that underperformed historical patterns, this year’s Fourth of July ramp-up largely followed suit. With many shippers holding well-stocked inventories after pulling freight forward to avoid tariffs, typical seasonal tightness arrived late and fizzled quickly, making the holiday week a fleeting high point amid an otherwise soft peak season.

The short-lived volume surge offered carriers a brief reprieve from the persistently low rate environment. Supply showed some signs of strain but recovered quickly, indicating that current market conditions will likely persist or deteriorate further before improving.

For now, the only upside demand risk is the possibility that the Supreme Court rules that the use of the International Emergency Economic Powers Act (IEEPA) to enact retaliatory tariffs was illegal — a decision that could reverse the current policies and restore trade flows. Otherwise, demand will likely continue to fade in Q3 and remain soft well into next year.

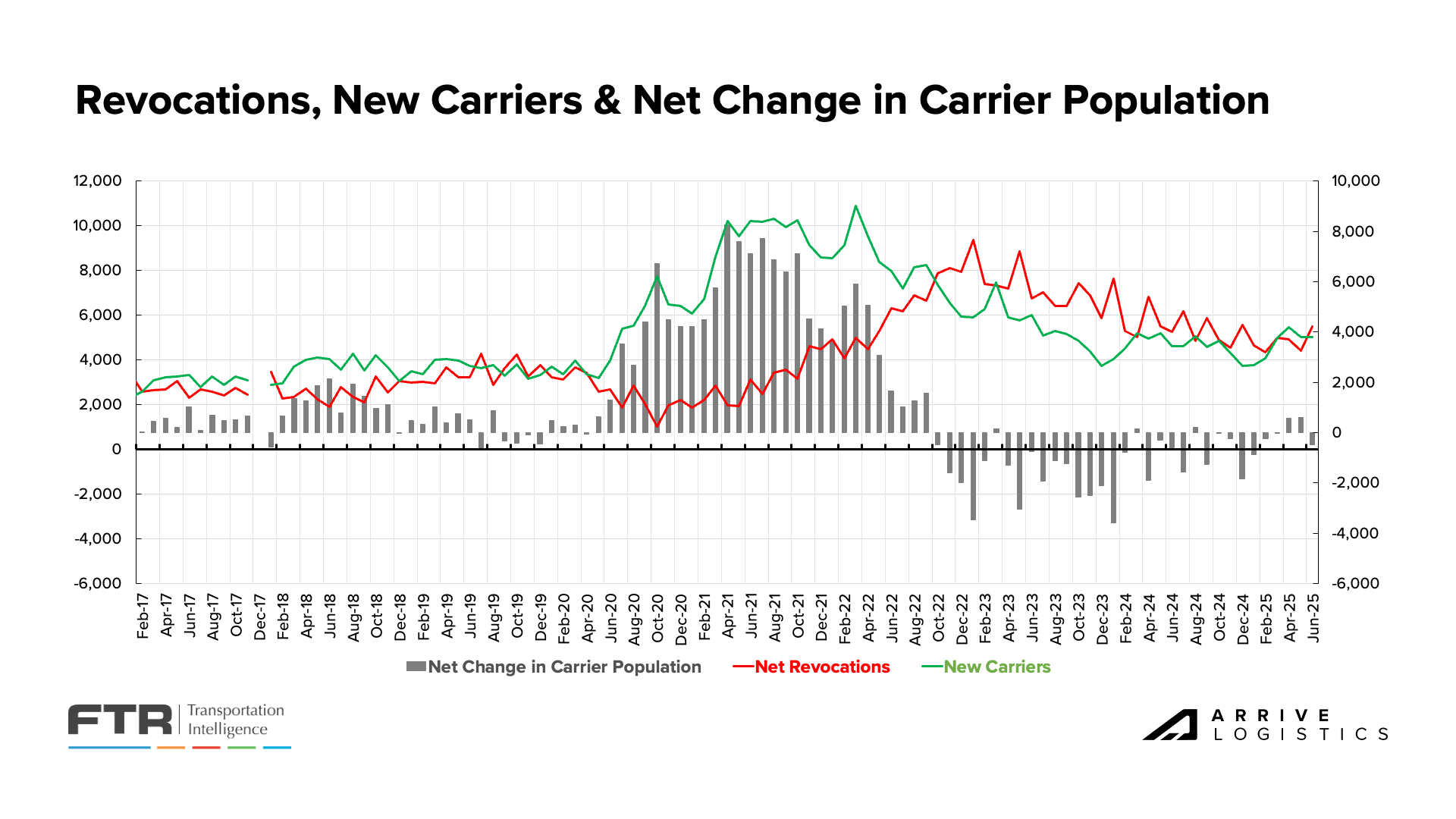

The combination of low demand, soft rates and high carrier operating costs remains the most significant risk to capacity. If current conditions persist, reductions will continue in the form of carrier exits and smaller truck counts at active fleets. Federal Motor Carrier Safety Administration initiatives like English proficiency requirements also pose a risk — the impacts have been limited so far, but that could change if enforcement ramps up.

A healthy broader economy and relatively strong consumer spending should continue to support demand for now. The next period of volatility will come as the back-to-school shopping season begins, though rising inflation later this year could limit its impact.

That said, shippers and carriers can expect more of the same market conditions in August.

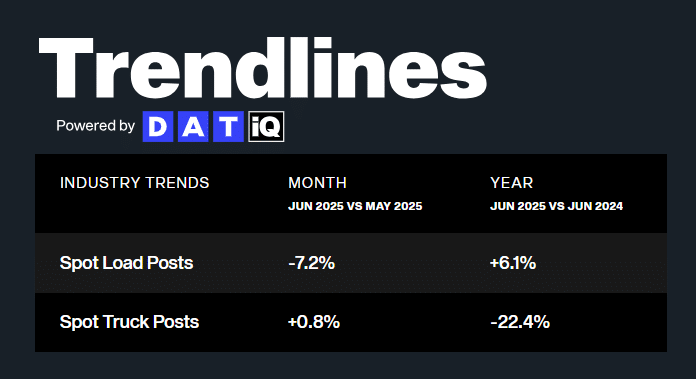

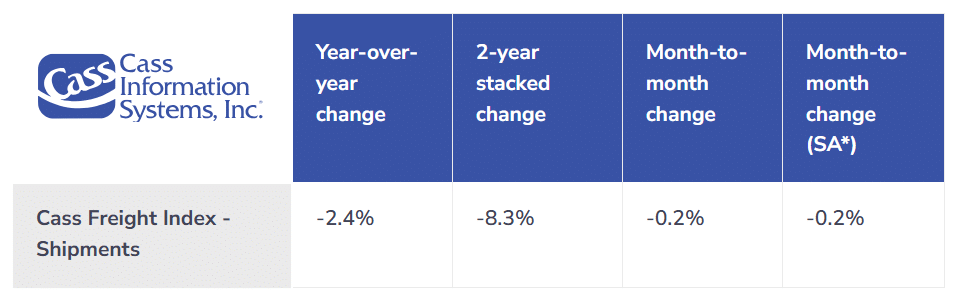

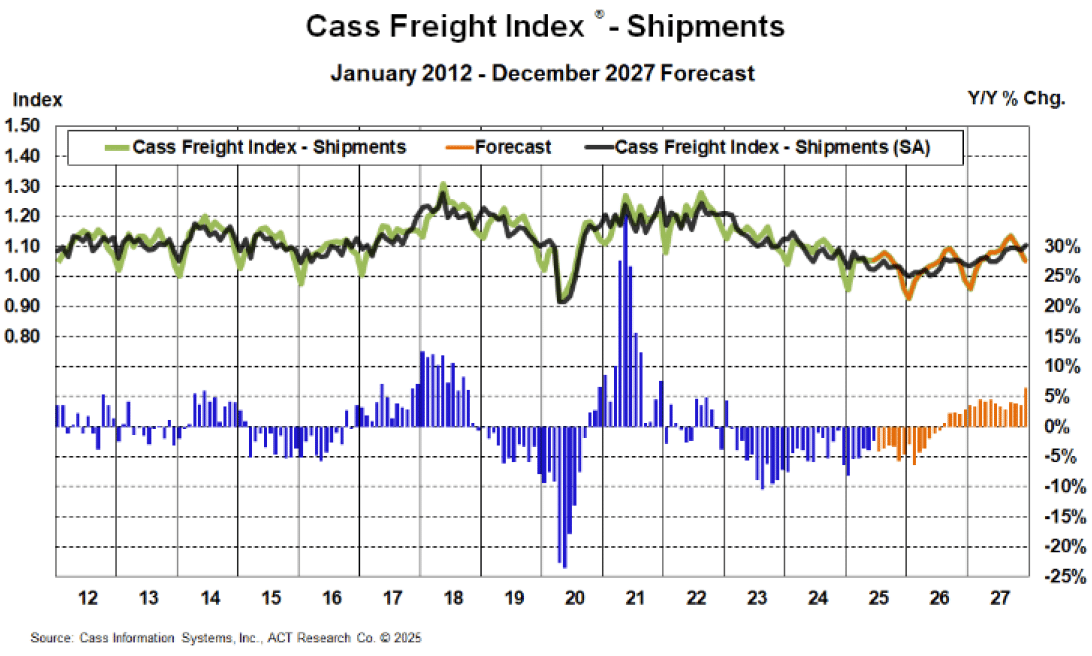

Keep reading for a closer look at what’s unfolding across demand, supply and rates.