"*" indicates required fields

"*" indicates required fields

"*" indicates required fields

Welcome to Arrive’s comprehensive outlook for national dry van and reefer truckload rates for January 2024 through December 2026. The Arrive Insights team generated this forecast through a combination of extensive historical research and output from the predictive models built into ARRIVEnow™, our proprietary technology platform.

Successfully navigating freight market cycles starts with a clear understanding of the relationship between rates and the core components of truckload supply and demand. In short, high or rising demand paired with tight capacity drives rates up, while soft or declining demand and abundant capacity push rates down.

By tracking directional trends in truckload demand (volume) and available capacity (trucks) at any point in time, we can predict rate movements with a high degree of accuracy and consistency. With that foundation, we present our rate forecast for the year ahead.

Tariff impacts will begin to compound in the back half of 2025 and carry into 2026, limiting the potential for demand growth. Additional demand destruction will result in more capacity leaving the market. With both forces on the decline, the current rate floor should remain in place with minimal further downside risk to spot rates. A flat to modest rate growth environment, with greater upside potential if demand trends inflect, is our base case for spot rates over the next year.

Contract rates have stabilized and reached a floor. Further reductions in the national average are unlikely as rates are already near carrier breakeven points. At the same time, significant near-term rate increases are improbable as shippers maintain pricing power with spot rates still well below contract rates.

Brief volatility around holidays and seasonal surges will remain the main risk for shippers in the spot market. Carrier attrition could make these swings more pronounced over time and increase market vulnerability, but only a large-scale black swan event would create sustained disruption.

Uncertainty in global trade policy limits visibility into a potential inflection toward inflationary conditions. Even so, declining capacity should keep the outlook dynamic, even if near-term rate forecasts point to more of the same.

Routing guides have held largely intact and should be stable through at least the first half of 2026, with some increased vulnerability to disruption in the back half of the year. Seasonal demand will continue to drive regional or nationwide rate volatility and should make short-term directional trends more predictable.

Asset carriers will continue to face profitability pressure as shippers negotiate for lower rates. As a result, some may be forced to exit the market or scale back fleet investment, gradually reducing available capacity.

Without a meaningful capacity disruption or black swan event, spot rates are unlikely to cross contract rates. Rate growth and disruption duration throughout the year are expected to remain muted.

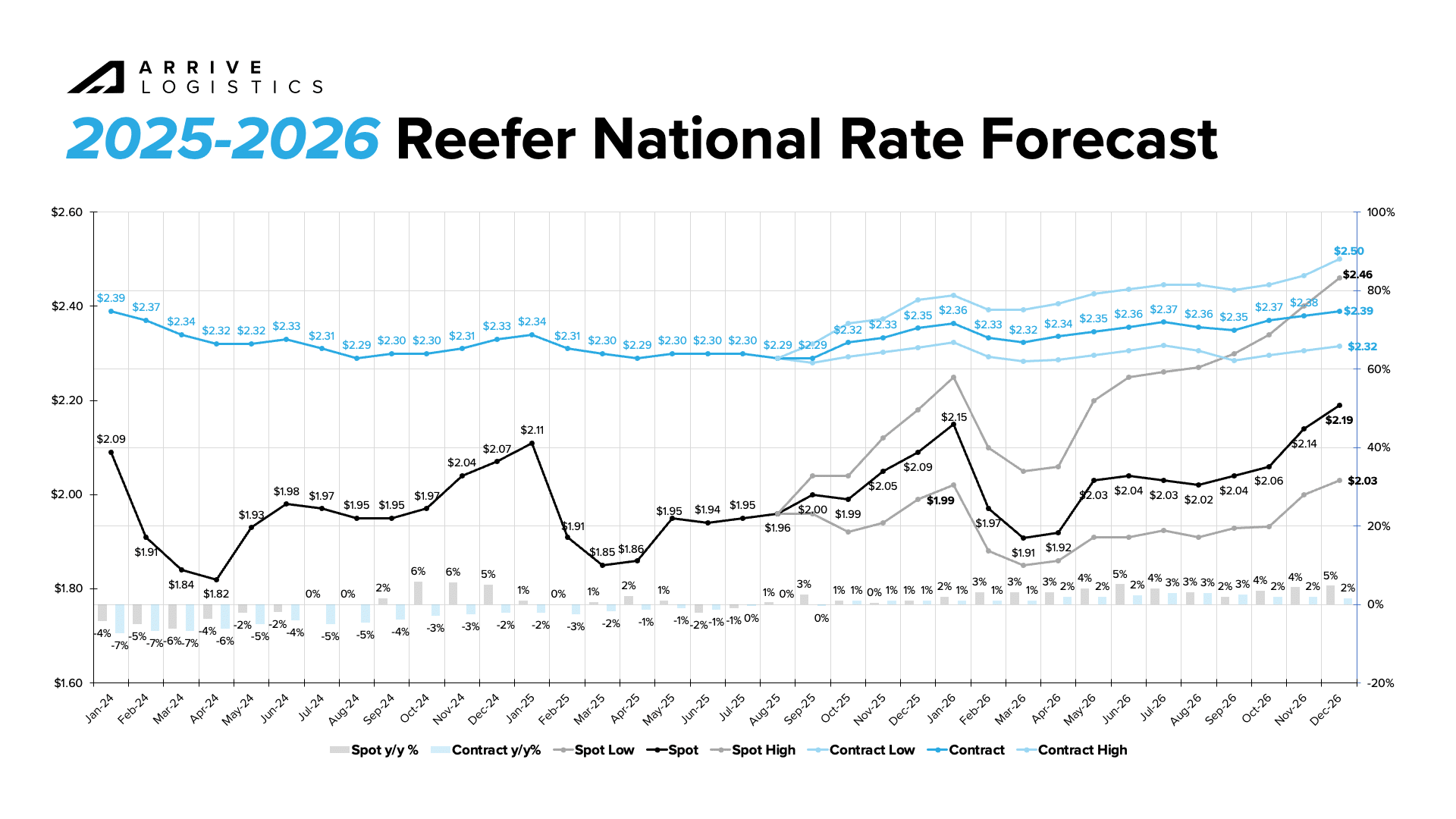

Reefer routing guides continue to show higher volatility during seasonal surges, indicating greater vulnerability to demand shocks and suggesting the reefer recovery is further along than van.

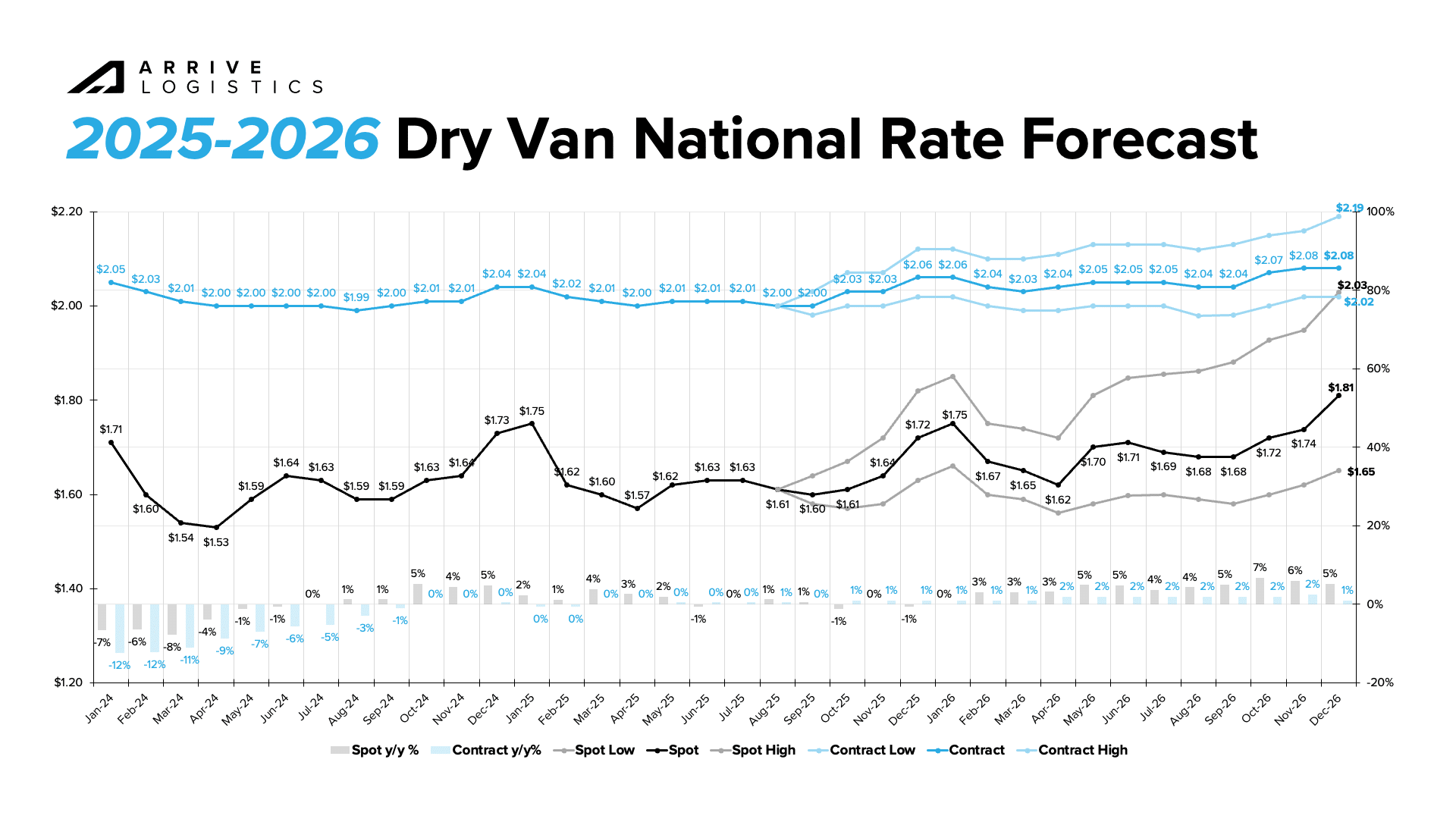

Van spot rates will reach a peak year-over-year growth rate of 6% in Q4 2026.

Van contract rates will reach a peak year-over-year growth rate of 2% in Q4 2026.

Reefer spot rates will reach a peak year-over-year growth rate of 5% in Q3 2026.

Reefer contract rates will reach a peak year-over-year growth rate of 2% in Q4 2026.

The dry van spot-contract rate spread will reach a low of $0.27 per mile late in Q4 2026.

The reefer spot-contract rate spread will reach a low of $0.20 per mile late in Q4 2026.

Weak demand has been a major theme in 2025, and the outlook suggests more of the same on the horizon. Tariffs are expected to have an impact in the second half of the year, especially for retail imports. These volumes typically provide a late-year lift, but after heavy front-loading in the first half, they are projected to decline.

The market is pricing for multiple interest rate cuts over the next year, though any benefit to freight-heavy sectors such as new home construction will take time to materialize. Manufacturing also remains in contraction, though the latest report showed a modest rebound in new orders.

Stable routing guides should continue to support strong contract market share while spot market demand remains muted.

Domestic manufacturing has now contracted for six straight months. New orders improved in the latest data, but tariffs remain a headwind to investment in large-scale projects.

Import volumes are expected to fall sharply after shippers pulled freight forward ahead of tariff implementation. At some point in 2026, inventories will need to be replenished, which should create a modest demand boost. Still, that replacement cycle alone is unlikely to shift broader market conditions.

Labor market cooling would create some downside pressure, but conditions remain stable for now. If they hold, we expect consumer spending to stay at or near current levels.

The market remains oversupplied as resilient carriers stay on the road despite ongoing financial challenges and right-sizing, limiting near-term vulnerability to disruption. However, declining equipment orders to below replacement levels will reduce capacity and could leave the market vulnerable to demand shocks.

The truck driver role is facing heightened scrutiny. From English language proficiency rules to other regulatory pressures, adding drivers to the road is expected to remain as difficult as ever. This could increase the magnitude and duration of disruptions when they occur by limiting how quickly capacity can be added once needed.

Year-over-year growth in tender rejections during seasonal or weather-driven disruptions points to mounting routing guide challenges and a more balanced supply environment. Still, the rapid normalization of rates once those disruptions pass confirms that overall capacity remains sufficient to meet demand.

Soft equipment orders in 2025 signal a shrinking tractor population. Carriers are not replacing equipment at the pace it is aging out, and private fleets are slowing investment in growth.

This forecast outlines what we believe will be the most likely scenario based on the information available at the time of writing. The upside and downside risks presented could materialize due to unforeseen events, including but not limited to the following:

Ongoing uncertainty around tariffs and other U.S. trade policies has clouded the truckload demand outlook for 2025 and 2026. Any meaningful actions by the new administration — or foreign governments in response — could create both upside and downside risks to the forecast.

Although a recession seems unlikely in the near term, uncertainty remains. Effects from elevated inflation and interest rates are still emerging and could worsen trucking conditions faster than expected, as reduced consumer spending and manufacturing slowdowns may lead to declining demand.

Severe weather regularly disrupts the freight market. Hurricanes Helene and Milton, along with the Q1 2025 winter storms, created notable short-term impacts. Similar events are likely, but conditions have tended to normalize quickly once storms pass, suggesting disruptions of this scale are unlikely to cause lasting market shifts in the near term.

Public truckload carrier spot rates have been below operating costs per mile for more than two years. Historically, spot rates can only fall so far before carriers begin exiting the market, which in turn drives rates higher. That dynamic has established today’s spot and contract rate floor. As capacity continues to leave the road, spot rates should reset higher after each period of seasonal volatility.

Fuel price and fuel surcharge volatility can complicate the measurement of forecast errors and influence shipper and carrier behavior. For example, rapidly declining fuel costs can ease conditions for carriers while reducing pressure on shippers seeking cost savings. While fuel prices have been relatively stable recently, the past 2–3 years have redefined volatility.

This report aims to set reasonable expectations for directional movements of national average spot and contract rates by factoring in macroeconomic conditions that impact supply and demand in the domestic truckload freight market.

The national average spot and contract rates per mile are sourced from DAT and receive no additional processing by Arrive. DAT may revise previously published rates, which can create variations between this report and source materials.

"*" indicates required fields

Matt Pyatt is the Chief Executive Officer of Arrive Logistics. He co-founded Arrive with President Eric Dunigan in 2014 after building his career at Command Transportation. As CEO, he is responsible for overseeing the company’s financial health, strategic vision and culture, as well as building a scalable leadership team to support Arrive’s growth.

"*" indicates required fields

"*" indicates required fields

Please have the following info ready to complete registration

Fraud Prevention

Freight fraud continues to impact our industry. We encourage shippers and carriers to reach out to Arrive immediately if there is ever a shipment in question that may be subject to fraud (including fictitious actors and websites). Arrive will not ask you to pay upfront for any dedicated lane or committed capacity program. If the offer you are receiving sounds too good to be true or unrealistic, it may be fraud. Arrive Logistics recommends verifying all communications come from our registered email domain is @arrivelogistics.com and notes that access via VPN or Proxy is prohibited on Arrive systems. Our 24/7 phone number is 888-861-0650 and our leadership team can also be reached at feedback@arrivelogistics.

Use of Cookies

We use cookies to enhance your browsing experience, serve personalized ads or content, and analyze site traffic. By continuing to use this website, you acknowledge and consent to our use of cookies as detailed in our privacy policy.

If you’re not an Arrive customer, please join our network to access the portal.

"*" indicates required fields

Scott Sandager is the Chief Administrative Officer at Arrive Logistics. He joined Arrive in 2018, bringing over 14 years of logistics and brokerage experience, with expertise in project and change management, organizational design, talent development and customer satisfaction. Scott previously held many diverse roles of increasing responsibility with AFN, a Chicago-based freight brokerage.

Eric Dunigan is the President of Arrive Logistics. He began his career at Command Transportation before co-founding Arrive with Matt Pyatt in 2014. As president, he is responsible for driving revenue and growth, as well as leading the Strategic Partnerships team — a veteran group of supply chain experts who work with Arrive’s customers to reimagine their shipping strategy.

"*" indicates required fields

David Spencer is the Vice President of Market Intelligence at Arrive Logistics. David joined Arrive in 2017 after spending six years at AFN focused on business intelligence. His department provides critical market data and expert analysis to internal teams and publishes monthly market updates for shippers and carriers under the Arrive Insights banner.

Andrew Clarke is Board Chairman for Global Critical and DCLI, Inc., and a board member for Arrive Logistics and Element Fleet Management Corp. His 20 years of global transportation and logistics experience include time as CFO of C.H. Robinson, CEO of Panther Expedited Services, Inc. and SVP and CFO roles at Forward Air Corporation.

Dean Croke is a Market Analyst at DAT Solutions, where he focuses on freight market intelligence and data analytics. His 35 years of experience with data analytics, transportation, supply chain management, mining and insurance risk management include time as co-founder of FleetRisk Advisors and in a number of other high-level roles with FreightWaves, Spireon, Lancer Insurance, Omnitracs Analytics (formerly Qualcomm) and more.

Asanka Jayasuriya is the CTO at 8VC. He is an accomplished engineering and product leader with 20+ years of experience in the cloud. He has a strong background in enterprise SaaS, PLG products, infrastructure, and security. Notably, he served as CTO and SVP of Engineering at SailPoint, leading their successful transition to the cloud and successful exit event. He also held senior leadership roles at InVision, Atlassian, and Amazon, driving growth, operational excellence, and innovation. At 8VC, Asanka works with the entrepreneurs and leaders in our portfolio as a virtual CTO supporting their growth.

Chad Eichelberger is the President of Reliance Partners. Since 2015, he’s leveraged his extensive experience in risk management, compliance, best practices and contracts to lead the company’s logistics and truck insurance strategy and operations. Chad was previously the President of Access America Transport, where he led the company from $8M to over $600M in revenue.

Barry Conlon is the CEO and founder of Overhaul, the global leader in active supply chain risk management and intelligence. With a remarkable career spanning over 30 years in supply chain security, he is widely regarded as a trailblazer in modern-day supply chain security standards and best practices.

As VP and Senior Analyst at ACT Research, Tim analyzes commercial vehicle demand and alternative powertrain development (i.e. electrification), and authors the ACT Freight Forecast, U.S. Rate and Volume Outlook. He previously spent fifteen years in equity research focused primarily on the transportation, machinery, and automotive industries, and co-founded leading equity research firm Wolfe Research.

"*" indicates required fields