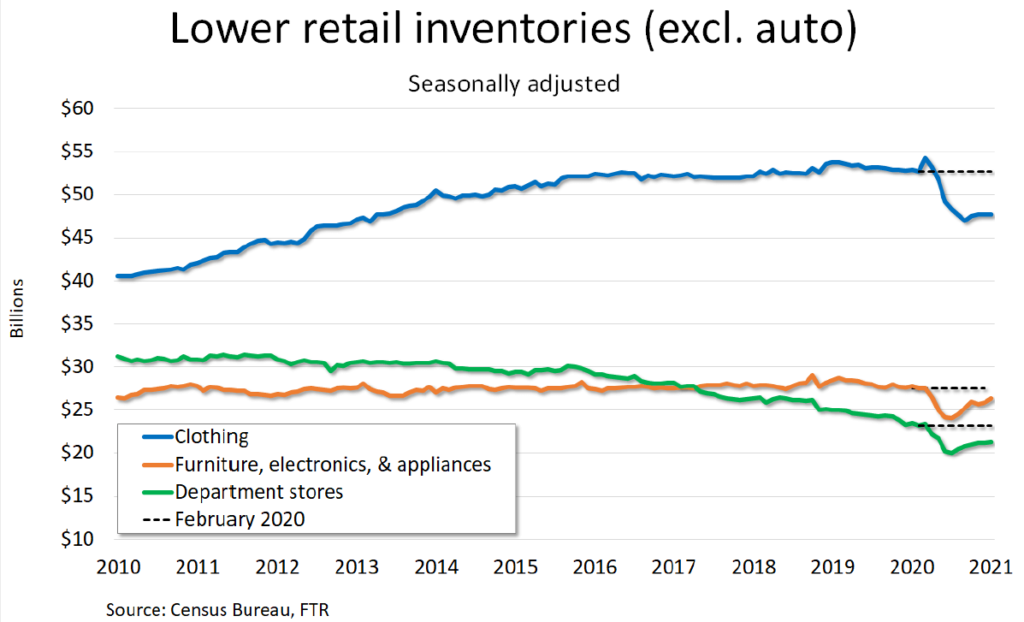

Freight volumes remained elevated throughout March following the surge in demand resulting from the winter storms that wreaked havoc across the south in February. Shipper routing guides failed as capacity networks were disrupted, resulting in an increase in contract tender rejections and a flood of freight to the spot market. Freight volumes have begun to ease in early April, following the end of quarter push, but overall demand remains strong. The backlog at the ports has provided a steady stream of volume in the form of imports, and the low inventory levels that have fueled increased demand throughout the pandemic are not getting any better.

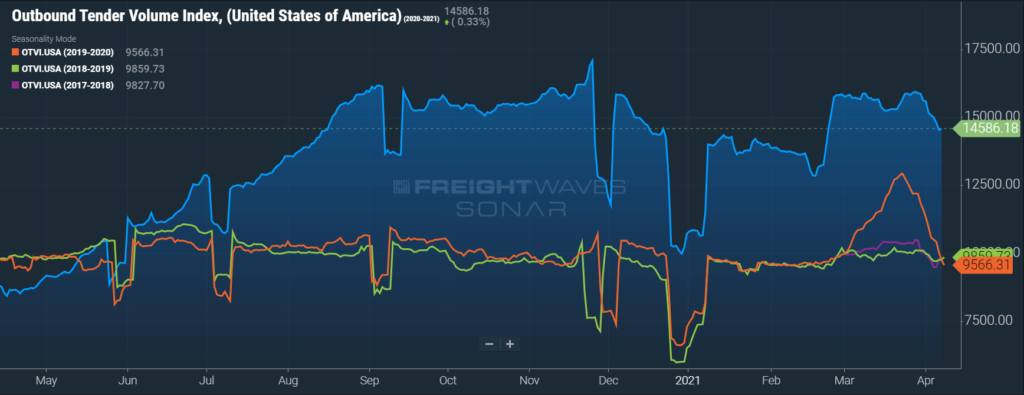

FreightWaves SONAR Outbound Tender Volume Index (OTVI), which measures contract freight volumes across all modes, was up nearly 38% year-over-year on March 31st. It is important to note that OTVI includes both accepted and rejected load tenders, so we must discount the index by the corresponding Outbound Tender Rejection Index (OTRI) to uncover the true measure of accepted tender volumes. If we were to apply this method to the year-over-year OTVI values, the increase in volume drops to 23%. This was a large increase from just eight days earlier, when the OTRI adjusted volume index was only up 8.4% year-over-year when 2020 freight volumes surged and panic buying reached its peak. The dry van and reefer tender volume indices were also up more than 60% and 88% year-over-year at the end of the month, which equated to 42% and 36% increases in actual volumes for the two modes, respectively. Tender volumes for both dry van and reefer have fallen in early April, with OTRI adjusted dry van volumes down 6% and OTRI adjusted reefer volumes down 9% since their peak on March 28th.

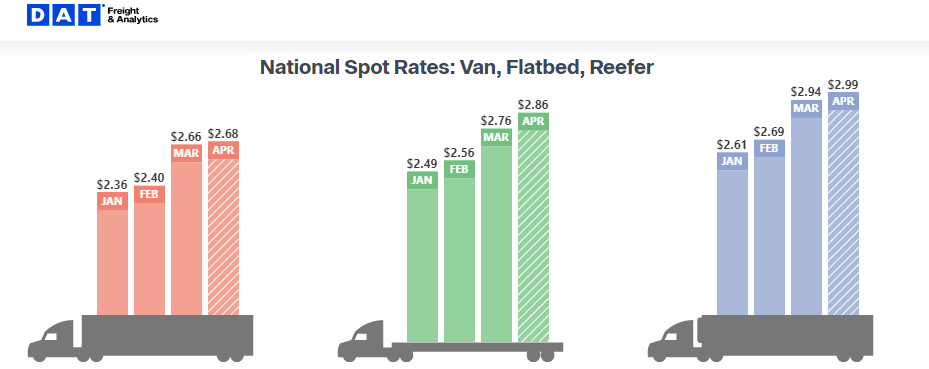

DAT reported that dry van spot load posts increased sharply in March, climbing by 22.3% month-over-month and 129.9% year-over-year. Spot volume growth slowed recently with only a 0.3% increase since last week, following the last full week of the quarter.

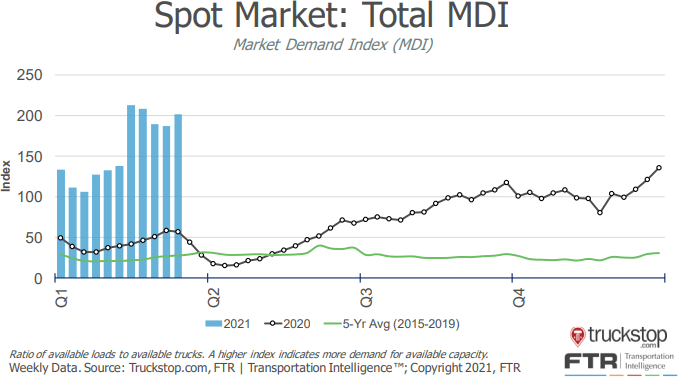

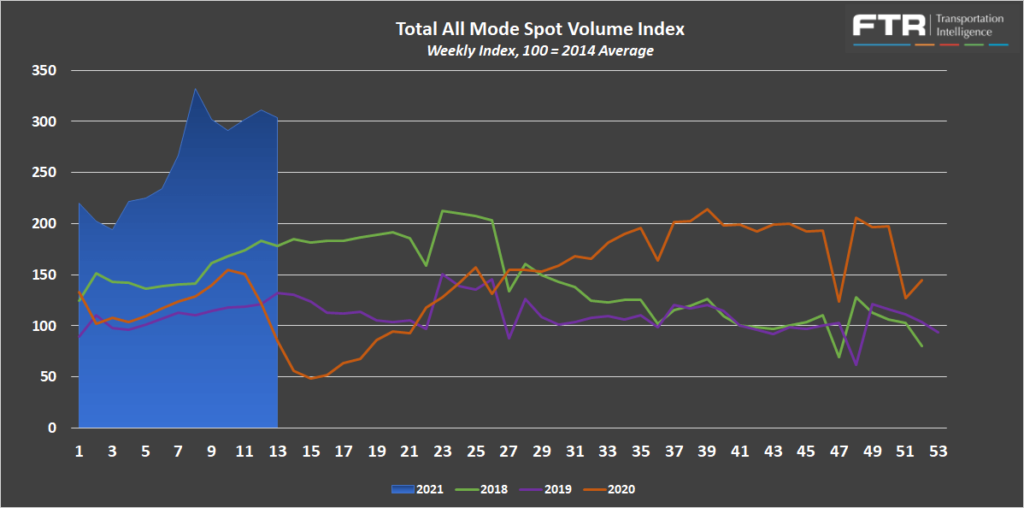

FTR and Truckstop’s Total All Mode Spot Volume Index is down 8.5% from the high in late February but is now up 257% year-over-year. After falling early in the month, the index climbed as it approached the end of the month and quarter, resulting in a relatively flat increase of just 0.5% from the start of the month.

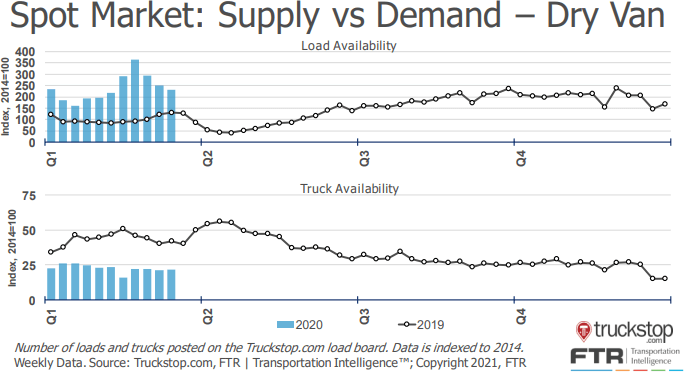

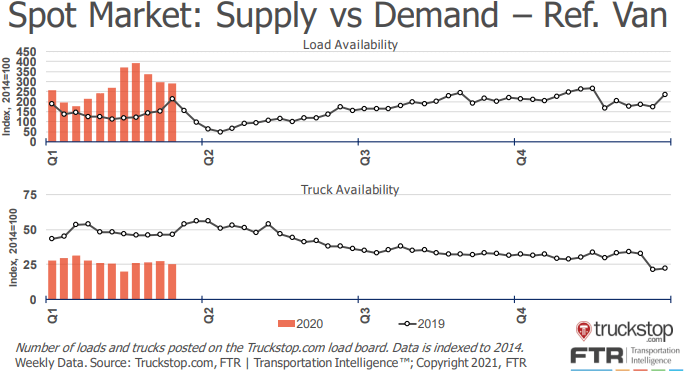

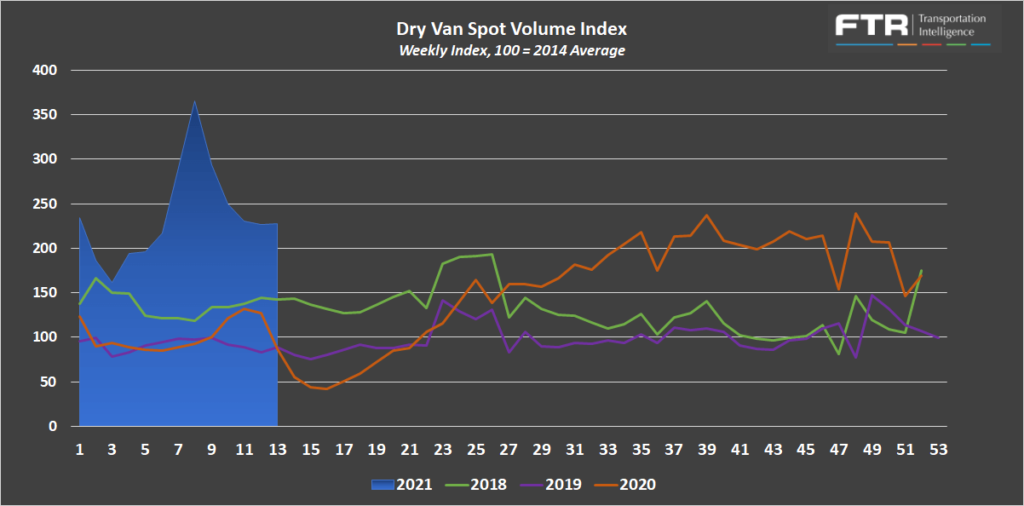

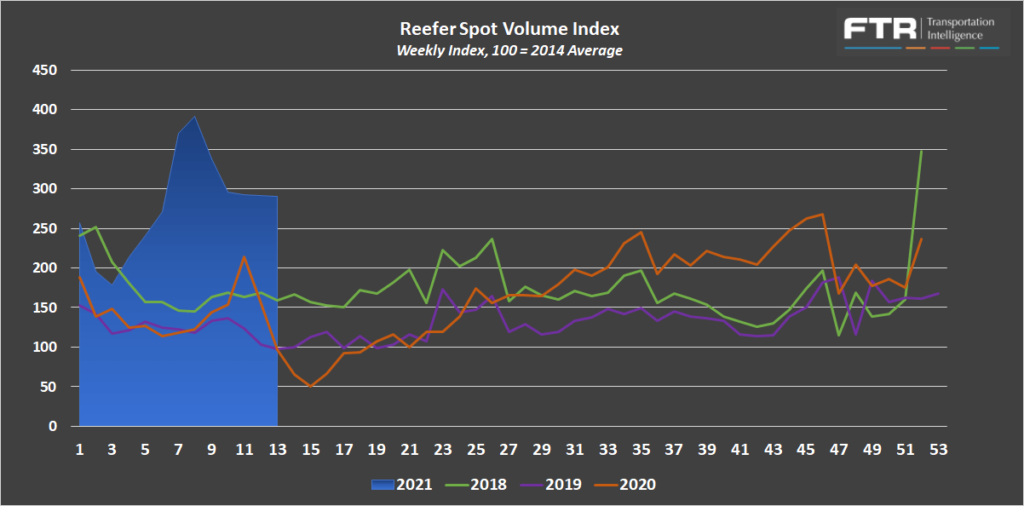

The Dry Van Spot Volume Index is down 38% from the high in late February and up 161% year-over-year, and the Reefer Spot Volume Index is down 26% and 199% over the same time period.

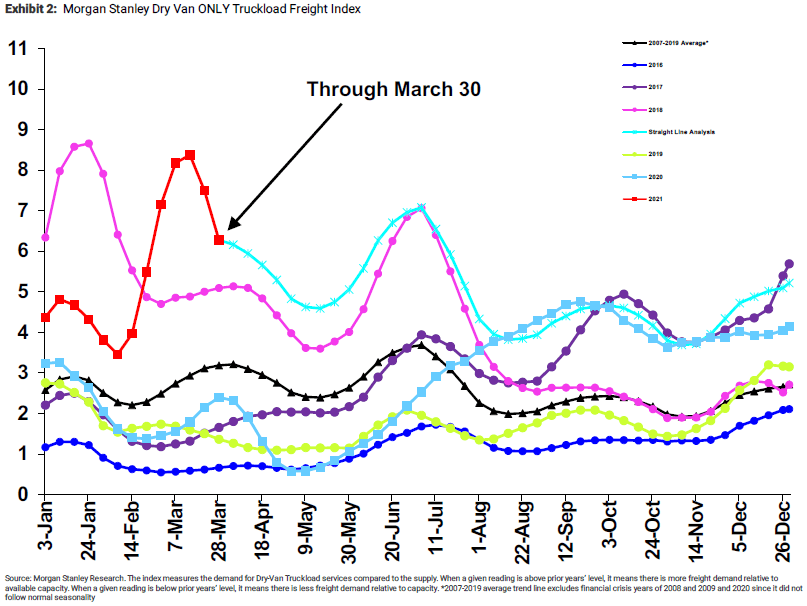

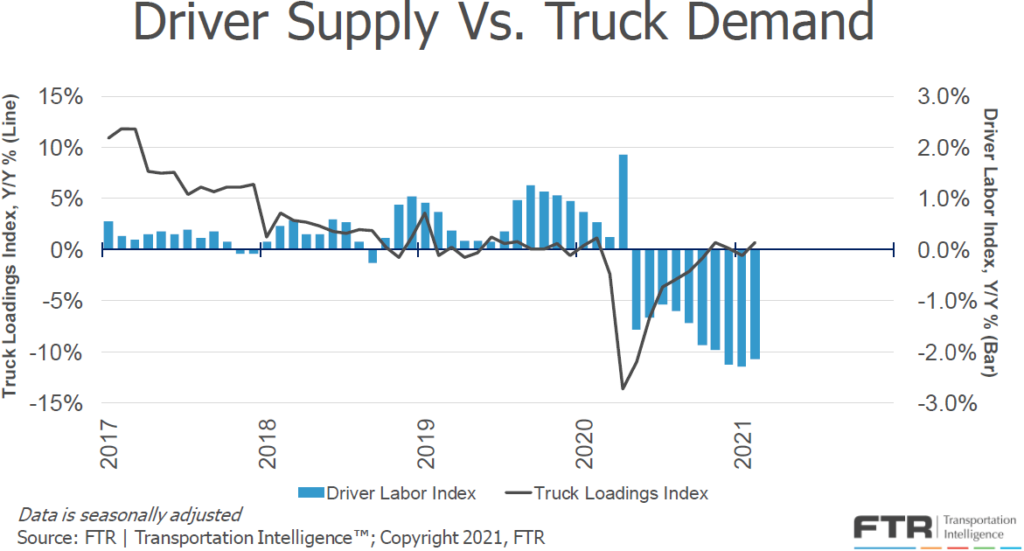

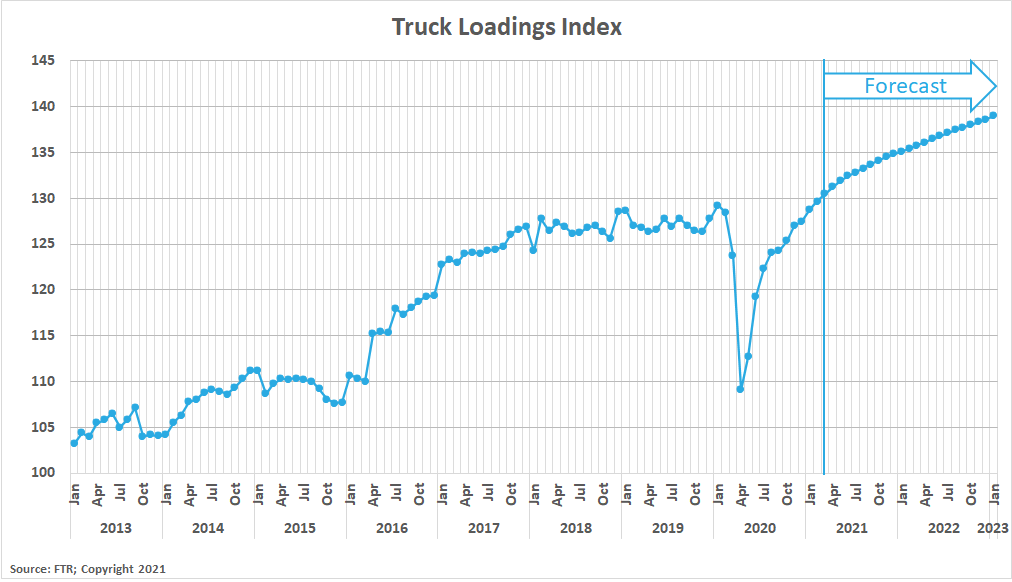

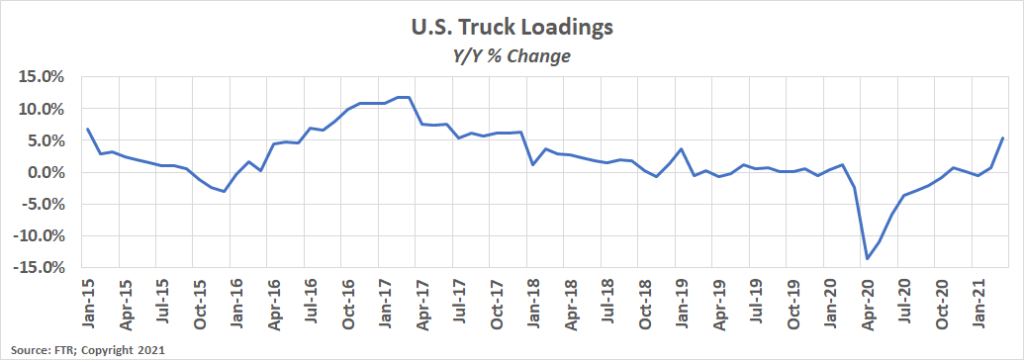

FTR’s Truck Loadings Index was up by 5.3% year-over-year in March after rising by 0.8% month-over-month from February. This is the first year-over-year increase of more than 5% since December 2017. Moving forward in 2021, year-over-year comparisons will be mostly irrelevant as the initial stages of the pandemic created highly volatile demand beginning in March 2020. The two-year trend should give us a better indication of monthly growth. March 2021 truck loadings were up 2.8% from March 2019 truck loadings, an increase from 1.8% in the two-year period beginning February 2019.

Truckload supply became extremely constrained following the winter storms in February. Fluctuations in demand created surges in spot volume activity as capacity networks were thrown out of balance. There wasn’t much of a change in the capacity environment throughout March as conditions remained tight leading up to the end of the month and quarter. In early April, however, the data suggests that the peak of tightness has likely passed.

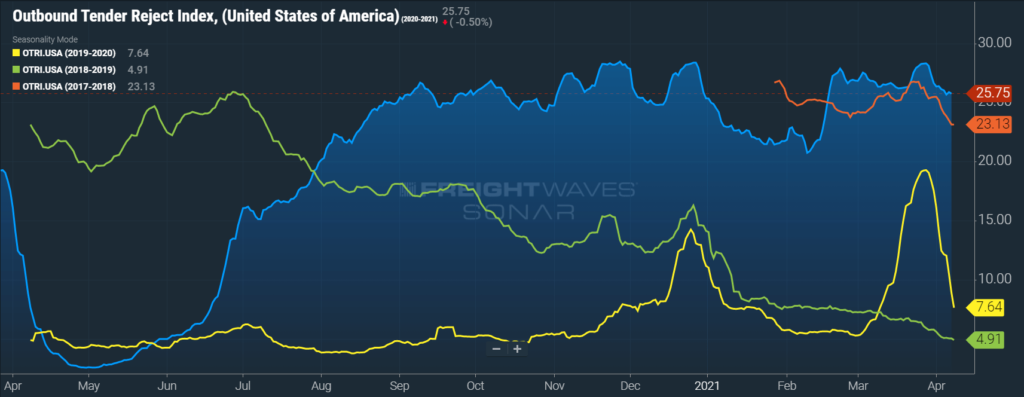

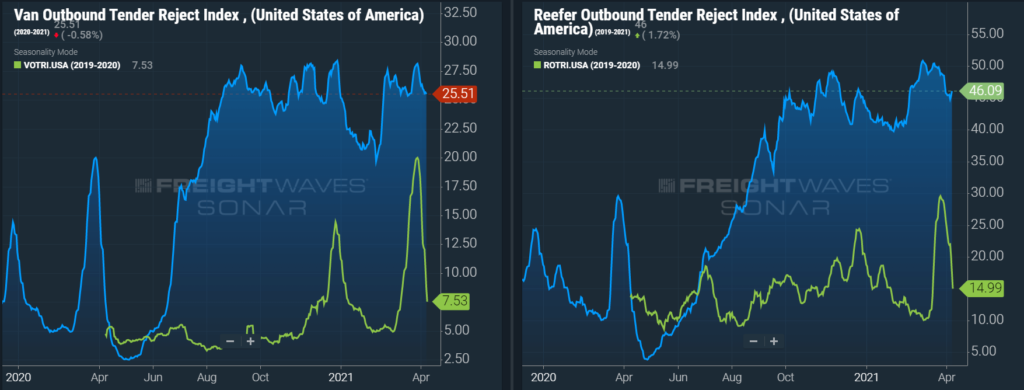

Sonar Outbound Tender Reject Index (OTRI) measures the rate at which carriers are rejecting the freight that they are contractually required to take. This index tends to follow the changes of spot freight activity — the higher the tender rejections, the higher the spot volumes. Tender rejections peaked at more than 28% on March 28th, just shy of the all-time record high. The index currently sits at 25.75%. This decline illustrates that conditions have moderated early in the second quarter. This trend aligns with normal seasonality, which would indicate things should soften further, before starting to heat up again in mid to late May. That being said, conditions have been far from normal over the past year, so we recommend remaining vigilant as conditions could shift quickly.

The trends were consistent across the different equipment types as both dry van and reefer rejections have fallen from a peak in late March. Dry van tender rejections currently sit at 25.51%, and reefer tender rejections currently sit at 46.09%.

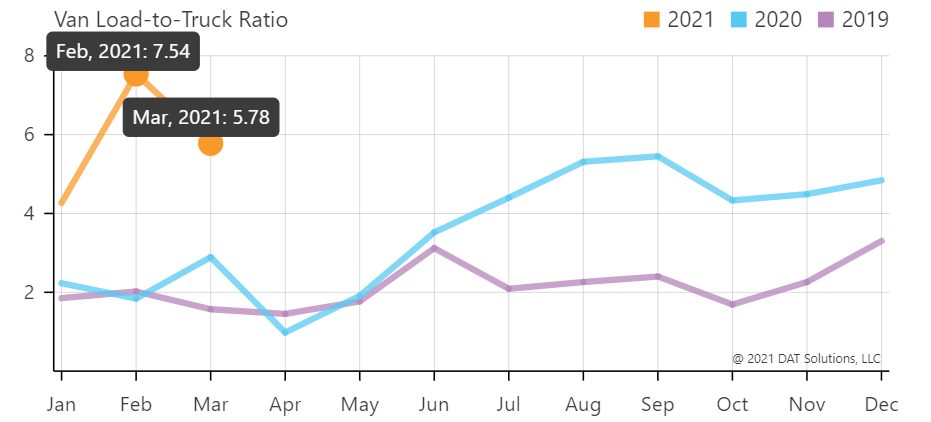

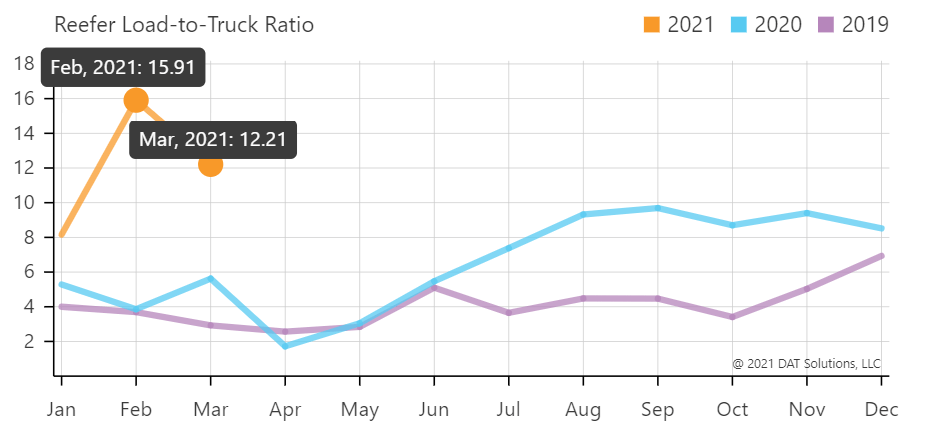

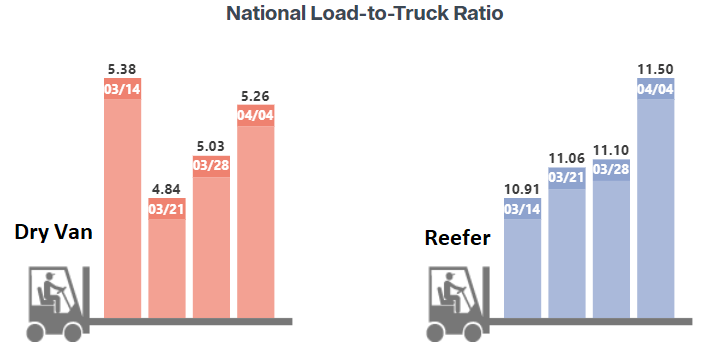

The DAT Load to Truck Ratio measures the total number of loads posted compared to the total number of trucks posted on their loadboard. In March, the Dry Van Load to Truck Ratio fell to 5.78, a decrease of 23% month-over-month, and an increase of 100% year-over-year. The Reefer Load to Truck Ratio fell 12.21 in March, an increase of 23% month-over-month and an increase of 117% year-over-year.