The Morgan Stanley Dry Van Freight Index is another measure of relative supply; the higher the index, the tighter the market conditions. The black line with triangle markers on the chart provides a great view of what directional trends would be in line with normal seasonality based on historical data dating back to 2007.

The most recent reading in mid-August showed month-over-month trends following the 10-year average: tightening in early to mid-July and then softening. Based on historical patterns, conditions should remain soft through August until Labor Day, when we expect some increased routing guide challenges to begin and last through the end of the quarter. The index is also up year-over-year, indicating a similar story as tender rejection and load-to-truck ratio data.

The reefer index continues to closely follow the 10-year average, while the flatbed index is well below it but in line with 2023 levels.

Morgan Stanley Dry Van Truckload Freight Index

Morgan Stanley Reefer and Flatbed Truckload Freight Indices

Morgan Stanley Reefer and Flatbed Truckload Freight Indices

The ACT For-Hire Trucking Supply-Demand Balance Index fell to 49.6 in June from 58.7 in May, reflecting declining freight volumes and increasing fleet capacity. While capacity remains abundant, future demand growth and improving inventory cycles should continue to support the market. However, private fleet expansion (not included in the data) could extend the market’s recovery period overall.

ACT For-Hire Trucking Survey

ACT For-Hire Trucking Survey

While obtaining precise capacity data remains challenging, recent trends and flattening rates indicate that the market has stabilized following some volatility around the Fourth of July.

The Sonar Outbound Tender Reject Index (OTRI), which measures the rate at which carriers reject the freight they are contractually required to take, shows more volatility now than at this time last year. Tender rejections and rates were flat in late July and early August, and rejections continue to reflect 2019 mid-year trends. Flattening rejection rates likely stem from steady demand trends and slow capacity attrition.

Reefer rejection rates are higher than a year ago, when the Q3 harvest season created volatility. Elevated rejection rates could create routing guide challenges for shippers as volatility increases around Labor Day and the end of Q3.

Outbound Tender Reject Index (SONAR)

Outbound Tender Reject Index (SONAR)

Van & Reefer Outbound Tender Reject Indices

Van & Reefer Outbound Tender Reject Indices

The DAT Load-to-Truck Ratio measures the total number of loads relative to the total number of trucks posted on its spot board. The dry van reading fell to 4.18 in July, a slight slip from June and the first decline following four consecutive months of increases. Despite the month-over-month drop, the ratio remains slightly elevated compared to previous years. The reefer load-to-truck ratio fell to 6.52 but remains slightly above the July 2023 reading.

FTR’s latest revocation trends showed the largest single-month decline since April. FTR points out that this was likely because July had five Mondays, and that’s the day the FMCSA usually handles the most revocations. However, revocations still outpaced the number of new authorizations, indicating capacity pullbacks.

FTR’s Carrier Revocations, New Carriers & Net Change in Carrier Population

A recent survey conducted by the National Private Truck Council and published by ACT Research shows that the cost per mile for private fleets continues to rise, a trend that may correlate with new equipment purchases increasing ahead of the EPA regulatory changes coming in 2027. However, as private fleets’ costs rise and for-hire rates decline, shipper investments in private fleets may start to wane, leading to a shift in market share back to the for-hire market. This shift would increase for-hire demand over time and apply upward pressure on rates, even if freight volumes remain stable.

For-Hire Freight Rates & Private Fleets Costs Per Mile, ACT Research

For-Hire Freight Rates & Private Fleets Costs Per Mile, ACT Research

Based on the latest ACT Research data for U.S. Class 8 Tractors, the backlog-to-build (BL/BU) ratio increased to 4.5 months in July from 3.9 months in June, suggesting that incoming orders are outpacing production. The backlog is now 67,000 units, a four-year low. While build plans have fallen, the shrinking backlog indicates there is still a way to go as the market stabilizes.

ACT Research, U.S. Class 8 Tractors: Backlog and Backlog/Build Ratio

ACT Research, U.S. Class 8 Tractors: Backlog and Backlog/Build Ratio

The ACT For-Hire Driver Availability Index fell to 50.0 in June from 52.9 in May. However, driver availability remains relatively high as older drivers stay in the workforce longer due to increased living costs and the influx of CDLs issued during the pandemic. Given today’s soft market conditions, additional driver exits will be necessary to support rate recovery.

ACT For-Hire Trucking Index: Driver Availability

ACT For-Hire Trucking Index: Driver Availability

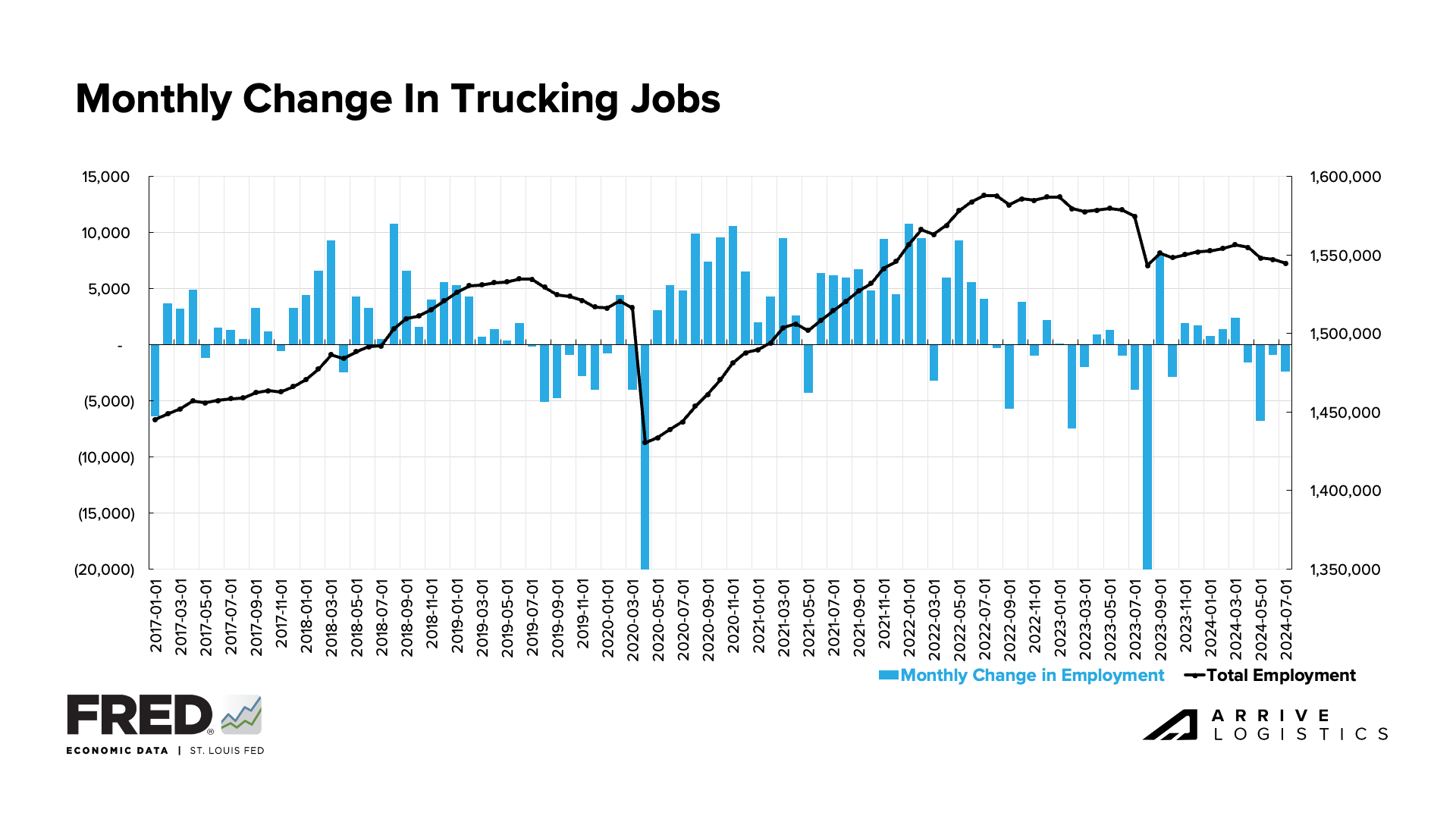

Trucking jobs fell by 2,400 in July on a seasonally adjusted basis, marking the fourth consecutive month of declining employment. Over 30,000 jobs have disappered since last July, and another 12,000 since April 2024. Drivers hoping for a strong peak season never saw it materialize, and since meaningful rate increases could still be a year away, employment will likely shrink further in the coming months, increasing the market’s vulnerability to demand fluctuations.

The import outlook remains positive overall, with the National Retail Federation’s (NRF) forecasting over two million TEUs monthly until November. U.S. ports handled 2.16 million TEUs in June, a 15% year-over-year increase. July and August imports should reach 2.34 million TEUs, marking a year-over-year increase of 22.5% and 19%, respectively. If current projections hold, 2024 imports would total 24.9 million TEUs, a 12% year-over-year increase.

High import volumes result partly from retailers preparing for a potentially strong 2024 holiday retail season. While this data is encouraging, we caution that retail orders are not always an accurate indicator of future retail spending. If retail executives overorder, it could create inventory stockpiles similar to those of the post-COVID era, which would have a deflationary impact on the freight market.

NRF Monthly Imports

NRF Monthly Imports

DAT reports that spot load postings declined 7.0% from June to July 2024 but rose 5.9% compared to July 2023, when postings fell by nearly 20% month-over-month and over 50% year-over-year. This data indicates conditions are stabilizing and moving closer to equilibrium.

Truck postings moved in the opposite direction, rising by 6.5% month-over-month, indicating easing spot demand. However, they fell over 10% from July 2023, likely reflecting the overall spot capacity decline.

Rates followed typical seasonality in July and early August, rising around the Fourth of July and declining steadily after. Van and reefer spot rates returned to June levels and should hold steady through August. However, the Q3 harvest season and produce seasons in the Midwest, Northeast and Pacific Northwest could spur reefer market volatility similar to a year ago in the lead-up to Labor Day.

Truckstop Weekly National Spot Rate Average

Truckstop Weekly National Spot Rate Average

After rising in July, national diesel prices have declined for several consecutive weeks. Prices are still lower than in August 2023, when they surged after OPEC announced surprise production cuts. Aside from demand surges and fallout from geopolitical conflicts, fuel prices should hold steady and offer carriers some relief from low spot rates.

DAT Fuel Trends

DAT Fuel Trends

DAT reports that dry van linehaul rates decreased to $1.60 per mile in August, reflecting spot market stabilization following the summer peak season. Contract rates are again trending down, falling $0.03 per mile to $1.98 per mile so far month-to-date. The spot-contract gap widened slightly to $0.38 per mile, indicating a resilient market capable of withstanding disruptions like Hurricane Debby.

DAT Dry Van National Average RPM Spot vs. Contract

DAT Dry Van National Average RPM Spot vs. Contract

The reefer market is seeing a similar pattern to the dry van market, with both spot and contract rates easing off summer peak season highs. After reaching $1.99 per mile in July, reefer linehaul rates have fallen to $1.93 per mile in August. Contract rates also fell from $2.34 per mile in July to $2.29 per mile in August. While this was the largest decline this year, contract rates will likely return closer to July levels later this month as more contract data comes in.

DAT Temp Control National Average RPM Spot vs. Contract

DAT Temp Control National Average RPM Spot vs. Contract

Flatbed spot rates declined by $0.05 per mile in July to $1.97 per mile, and contract rates rose to $2.61 per mile. The flatbed spot-contract rate gap remains historically high at $0.64 per mile, as both rates have trended down by $0.02 per mile month-to-date in August.

DAT Flatbed National Average RPM Spot vs. Contract

DAT Flatbed National Average RPM Spot vs. Contract

Inflation dropped to 2.9%, falling below 3.0% for the first time since 2021. During its September meeting, the Fed will likely cut rates by at least 25 basis points. While this will lower borrowing rates and could spur spending, it won’t impact the freight market until 2025.

Bank of America reported credit and debit card spending declined 0.4% year-over-year in July. Consumers continue to spend more on services than goods; Bank of America credited the Paris Olympics and Taylor Swift concerts overseas with a spike in international travel spending.

Bank of America, Total Card Spending per Household

Bank of America, Total Card Spending per Household