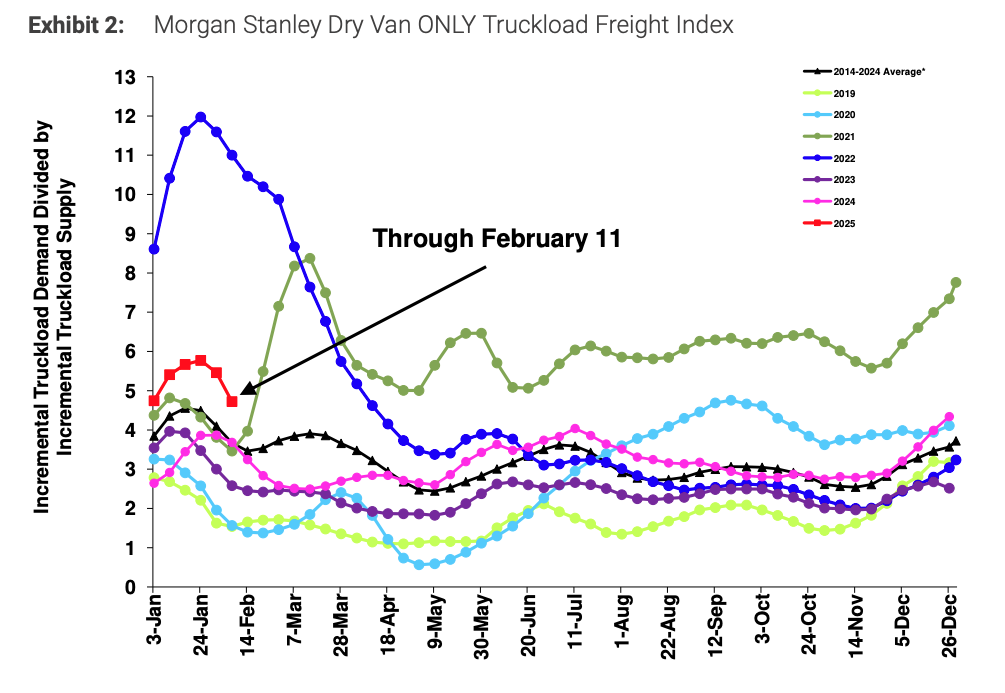

The Morgan Stanley Dry Van Freight Index is another measure of relative supply; the higher the index, the tighter the market conditions. The black line with triangle markers on the chart below provides a great view of what directional trends would be in line with normal seasonality based on historical data dating back to 2007.

Trends deviated from the 10-year average toward the end of 2024 and remained above 2024 levels and the 10-year average in early February 2025. However, the movement so far in 2025 has followed historical seasonal patterns very closely. If these trends continue, we expect further seasonal softening over the next few months.

Morgan Stanley Dry Van Truckload Freight Index

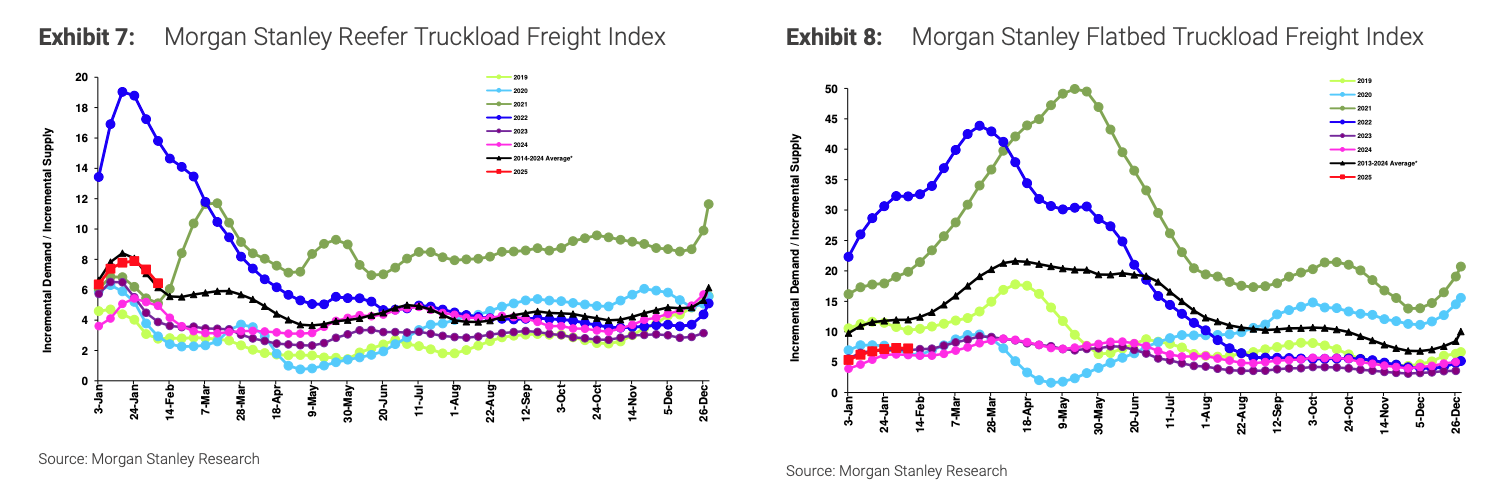

Morgan Stanley Reefer and Flatbed Truckload Freight Indices

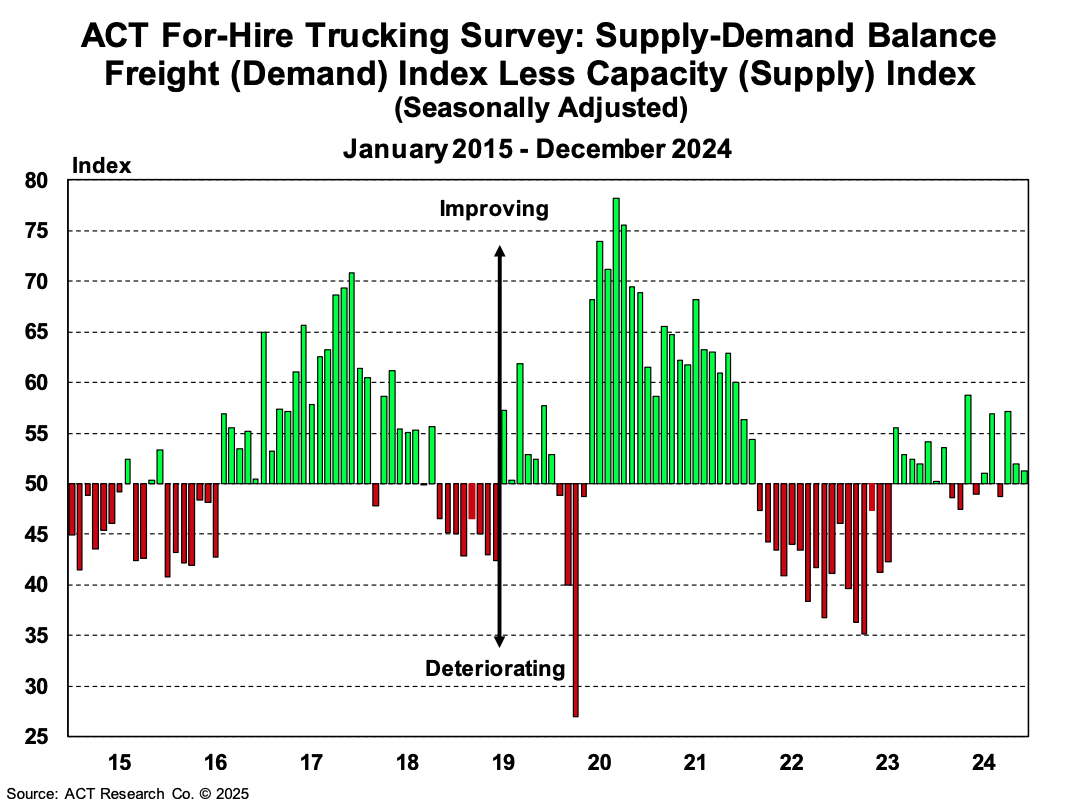

The latest ACT For-Hire Trucking Supply-Demand Balance Index indicates that market conditions tightened from October to November, driven by rising freight volumes and shrinking capacity. ACT also highlighted that the expansion of private fleets continues to play a key role in sustaining the prolonged equilibrium cycle.

Meanwhile, Class 8 tractor sales have slowed further, reinforcing expectations that the market will continue rebalancing in the coming months. If the U.S. economy expands as projected, freight volumes should rise, leading to tighter market conditions in 2025 compared to 2024.

ACT For-Hire Trucking Survey

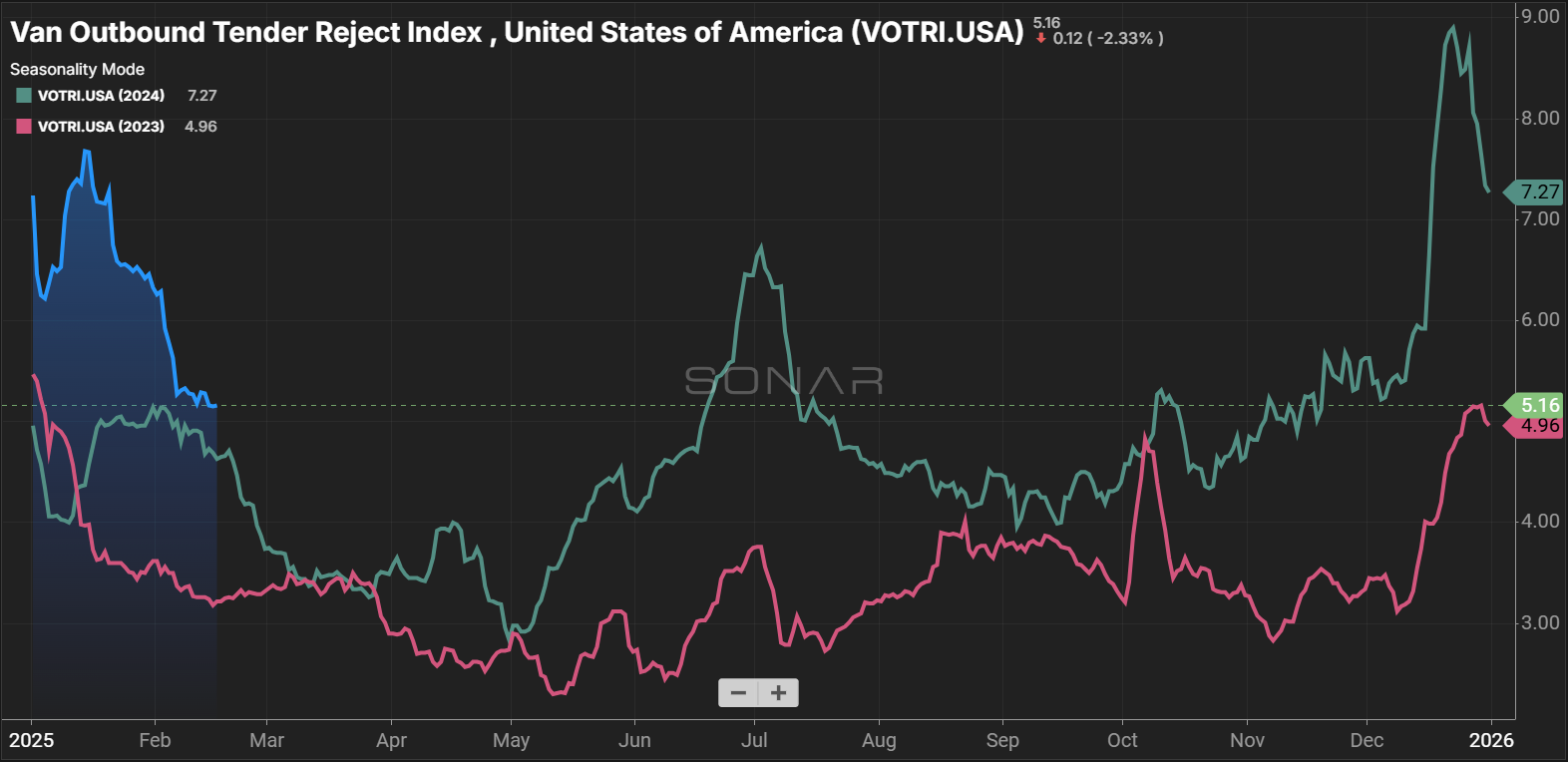

After several volatile weeks, recent data indicates rapid market normalization as demand and capacity ease. We expect Q1 conditions to remain steady aside from the disruptions typical for this time of year, such as winter storms.

The Sonar Outbound Tender Reject Index (OTRI), which measures the rate at which carriers reject the freight they are contractually required to take, has declined significantly from the weather-induced peaks of mid-January. Rates are hovering in the upper 5% range—while slightly higher than the same period last year. This reading indicates strong routing guide compliance.

We expect rejection rates to fall further in March and April in line with seasonal expectations ahead of the 100 Days of Summer. However, the increased volatility during the 2024 peak season is a sign that the market is more vulnerable to disruption than at any point in the current cycle, even as demand declines.

Outbound Tender Reject Index (SONAR)

Outbound Tender Reject Index (SONAR)

Dry van tender rejection rates have declined significantly and now align closely with February 2024 levels. As the market continues to follow typical seasonality, we expect rates to remain near the floor through the rest of Q1 and into early Q2.

The reefer market remains far more volatile than the dry van market. At 13%, tender rejection rates are up 75% year-over-year. Winter weather remains a risk, but if market conditions persist as temperatures rise, the 2025 produce and summer peak seasons could be significantly more active than in recent years.

Van & Reefer Outbound Tender Reject Indices

Van & Reefer Outbound Tender Reject Indices

The DAT Load-to-Truck Ratio (L/T), which compares the total number of loads to the total number of trucks posted on the DAT spot board, increased for dry van and reefer freight in January. The dry van L/T ratio climbed above 7.0, the highest point in the last two years. Similarly, the reefer L/T ratio surpassed 11, exceeding any point in 2023 and 2024. DAT’s load and truck posting metrics suggest this increase is driven almost entirely by a pullback in equipment postings, indicating carriers were much less reliant on posting equipment to find freight.

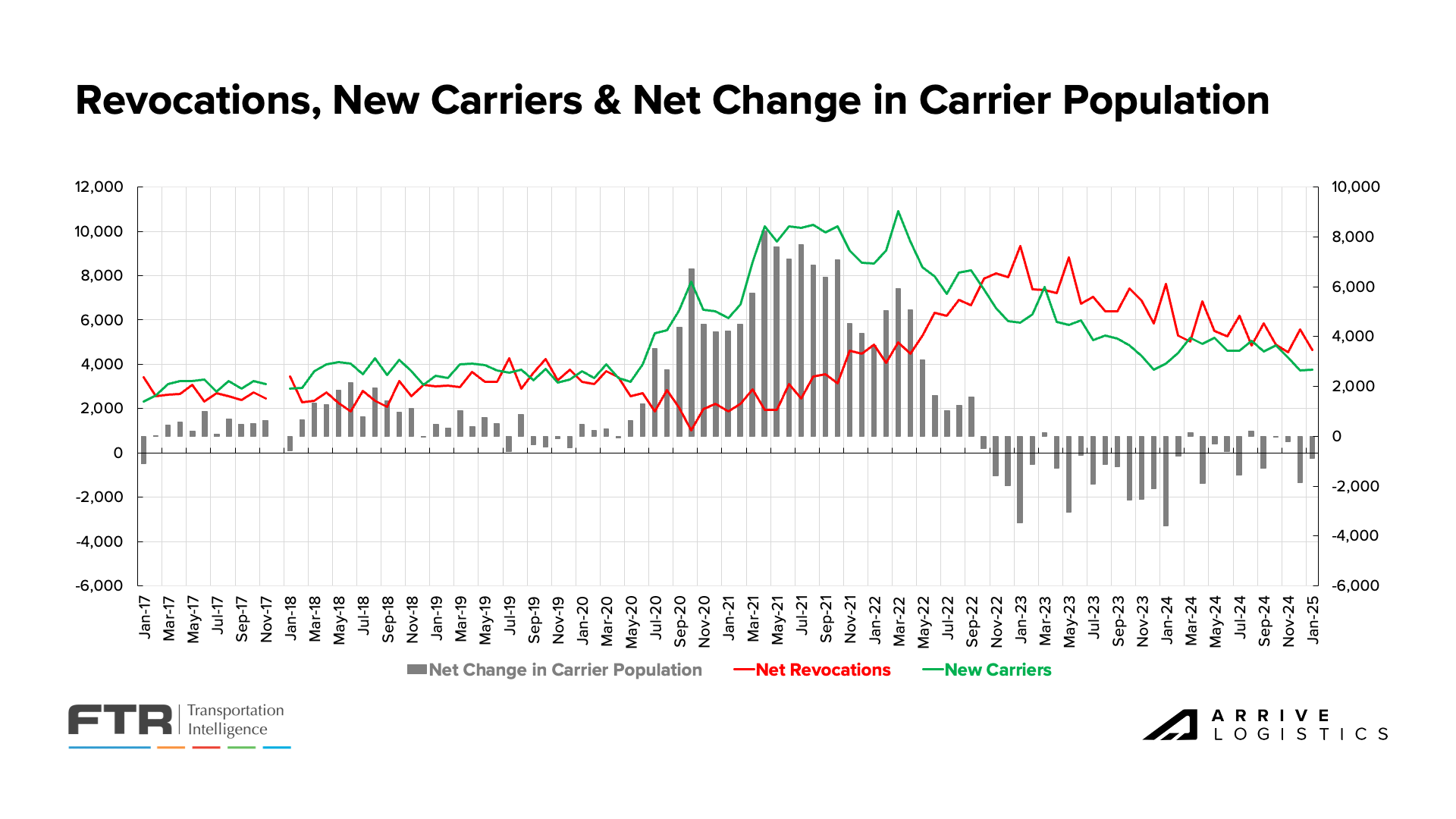

Challenging trucking conditions for carriers have resulted in high numbers of exits over the past few years. Year-over-year increases in load-to-truck ratios and tender rejection rates around the holidays make clear that these exits are creating more balanced market conditions.

While carrier population change trends do not tell the full story, they provide some insight into where supply levels are headed. Since the first carrier population decline during this cycle in October 2022, there has been a net loss of nearly 38,000 carriers, including 2,700 net revocations in the past two months—the highest number since January and February 2024 (nearly 4,400 net revocations). As the carrier pool continues to shrink, spot capacity will tighten, and market vulnerability will increase.

FTR’s Carrier Revocations, New Carriers & Net Change in Carrier Population

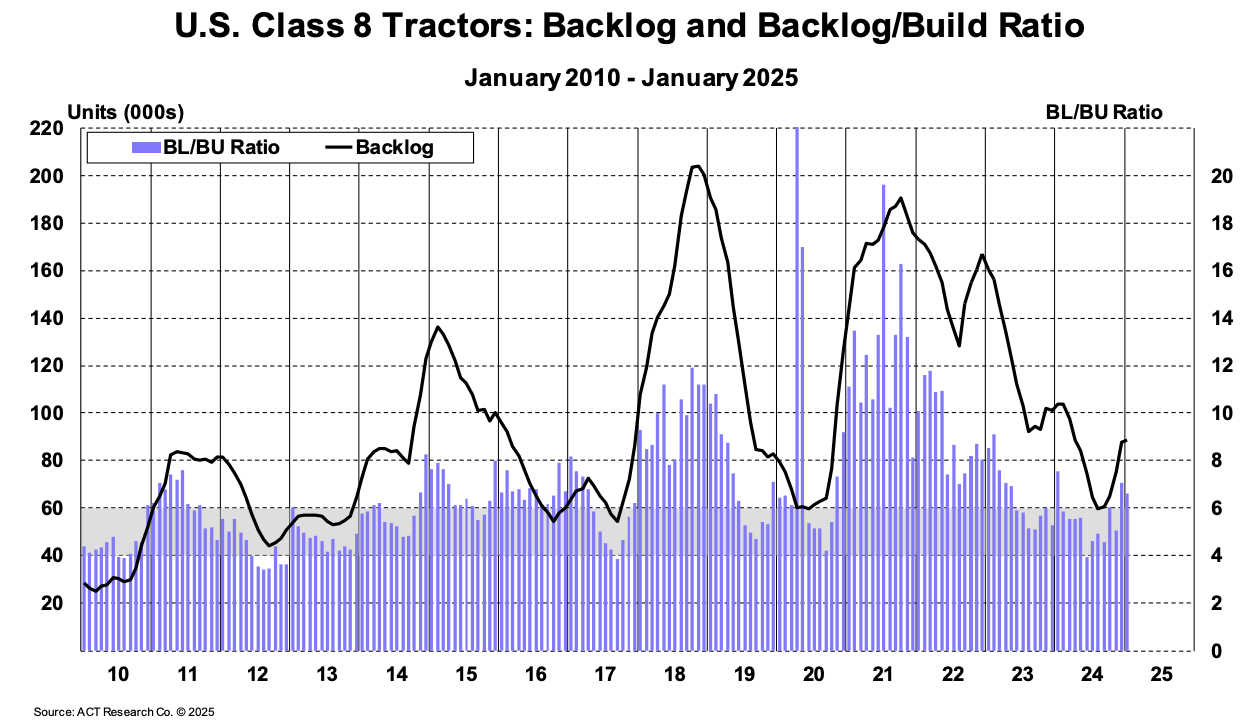

According to the latest ACT Research data on U.S. Class 8 tractors, the backlog-to-build (BL/BU) ratio rose from 6.5 months in November to 7.0 months in December. The backlog increased by more than 12,000 units, reaching 87,000 in December. ACT Research attributes this growth primarily to lower build rates as manufacturers continue prioritizing vocational production over tractor production. Lagging build rates indicate that significant increases in the capacity market remain unlikely – another sign that inflationary conditions will take shape more gradually.

ACT Research, U.S. Class 8 Tractors: Backlog and Backlog/Build Ratio

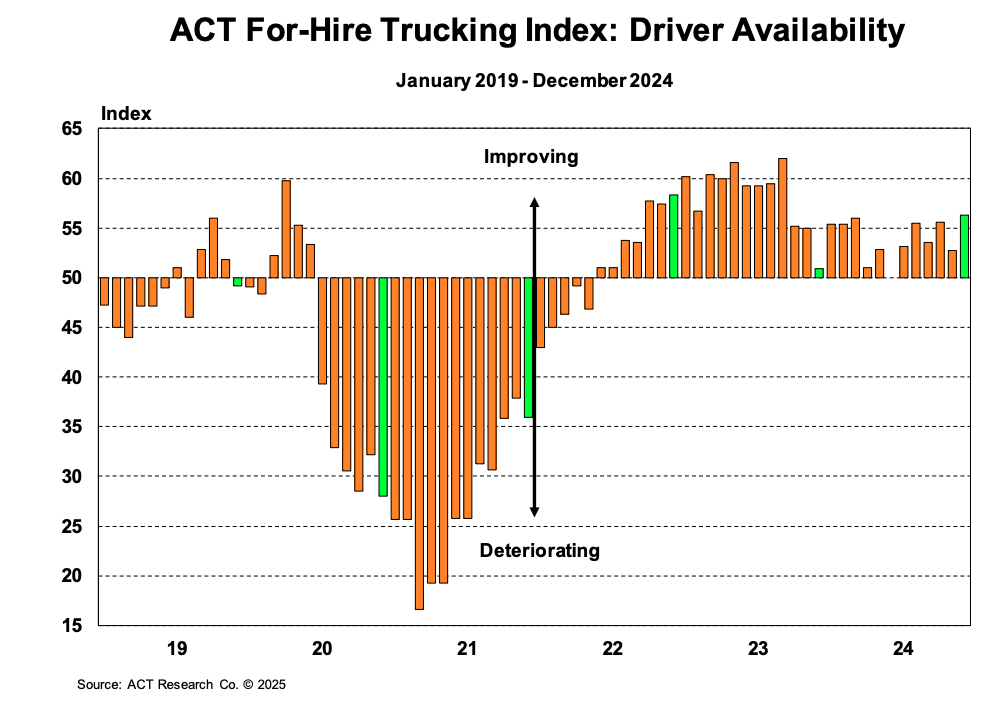

The driver market continues to support demand, as evidenced by the ACT Driver Availability Index rising 3.5 points to 56.3 in December, marking 31 consecutive months of stable or improving driver availability. Several factors contribute to sustained availability, including a 4%-5% market share shift to private fleets over the past two years and experienced owner-operators leaving the market to join larger carriers.

ACT For-Hire Trucking Index: Driver Availability

The January trucking jobs report revealed that 2024 started with 20,000 fewer jobs than previously reported and ended with 27,800 fewer jobs. This significant downward revision brings total trucking employment back to pre-pandemic levels, erasing gains from that high-rate era. This data doesn’t fully capture owner-operator capacity or private fleet capacity growth, so we do not believe overall supply has fallen to 2020 levels. However, the decline is significant and supports the narrative that capacity is, in fact, exiting the market.

On a positive note, though employment is down from its peak, there has been industry job growth in recent months. January saw a 3,800 job increase from December and 7,400 compared to October, likely driven by short-term disruptions like port strike threats, tariffs and peak retail season.

Demand was steady through the holiday season and should remain consistent in the near term. However, there is uncertainty surrounding how proposed U.S. tariffs and corporate tax cuts would impact the 2025 truckload demand environment.

The National Retail Federation (NRF) reports that imports consistently increased month-over-month in 2024. 2.14 million TEUs were imported in December, a slight decrease from November but nearly a 15% increase from December 2023. Import strength is likely due to shippers pulling freight forward to avoid the impact of the potential strike at East and Gulf Coast ports.

Imports for the first six months of 2025 are expected to remain steady. However, if additional tariffs are placed on North American, Asian and European goods, import volumes could be negatively affected.

NRF Monthly Imports

NRF Monthly Imports

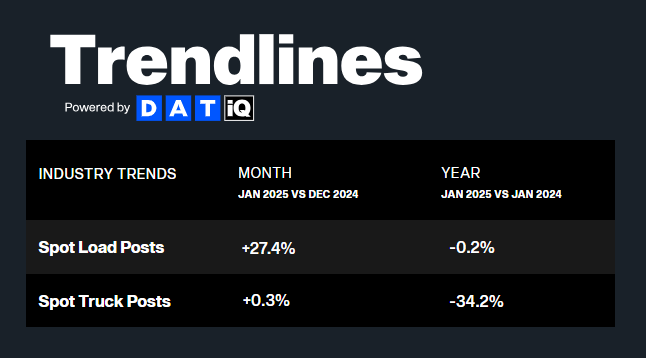

DAT reports that spot postings remained relatively flat year-over-year but increased over 27% from December to January, helping to offset contract volume declines. The year-over-year results showed significant improvement from January 2024, when spot postings were down nearly 40% from January 2023.

Truck postings tell a different story. They were relatively unchanged month-over-month but down significantly year-over-year, indicating that capacity reductions were the main driver of greater rate volatility during the 2024 holiday peak season.

Truckstop’s weekly spot market rate data shows sharp seasonal declines for van and reefer in early February. Rates for both modes reached their 2024 peak amid a year-end demand surge. However, around mid-January, rates rapidly returned to pre-holiday averages. This pattern is normal and closely resembles the trend observed around the same time last year.

Truckstop Weekly National Spot Rate Average

Truckstop Weekly National Spot Rate Average

Fuel prices fell for most of 2024 but rose in January and remained high in February. The February average is $3.66 per gallon, with a $0.40 dry van surcharge. Despite recent increases, prices are still lower than last year’s $4.04 per gallon average and $0.47 surcharge. Prices are expected to remain steady, but U.S. tariffs could create volatility.

DAT Fuel Trends

DAT Fuel Trends

DAT dry van data shows linehaul spot rates increased during the 2024 holiday season. They remained elevated into the new year, with the $1.76 per mile average in January being the highest monthly average since January 2023. Contract rates also rose to $2.05 per mile, matching the previous high in January of last year. Rates have since normalized. The spot average is currently $1.68 per mile, excluding fuel, and further declines are likely through the end of the month.

After closing to a cycle low in January, cooling spot rates caused the spot-contract rate gap to expand again in February. This shift supports our view that a sustained inflationary flip is not imminent.

DAT Dry Van National Average RPM Spot vs. Contract

DAT Dry Van National Average RPM Spot vs. Contract

Reefer spot rates, excluding fuel, increased month-over-month from October 2024 to January 2025. They peaked at $2.11 per mile in January, the highest mark since January 2023, before declining rapidly in early February. Rates are currently $1.95 per mile, excluding fuel, mirroring a similar downward trajectory as a year ago. Barring a major disruption, we anticipate rates will follow trends similar to 2024 for the next few months, remaining near a floor until May. Contract rates remain stable despite recent spot rate volatility.

DAT Temp Control National Average RPM Spot vs. Contract

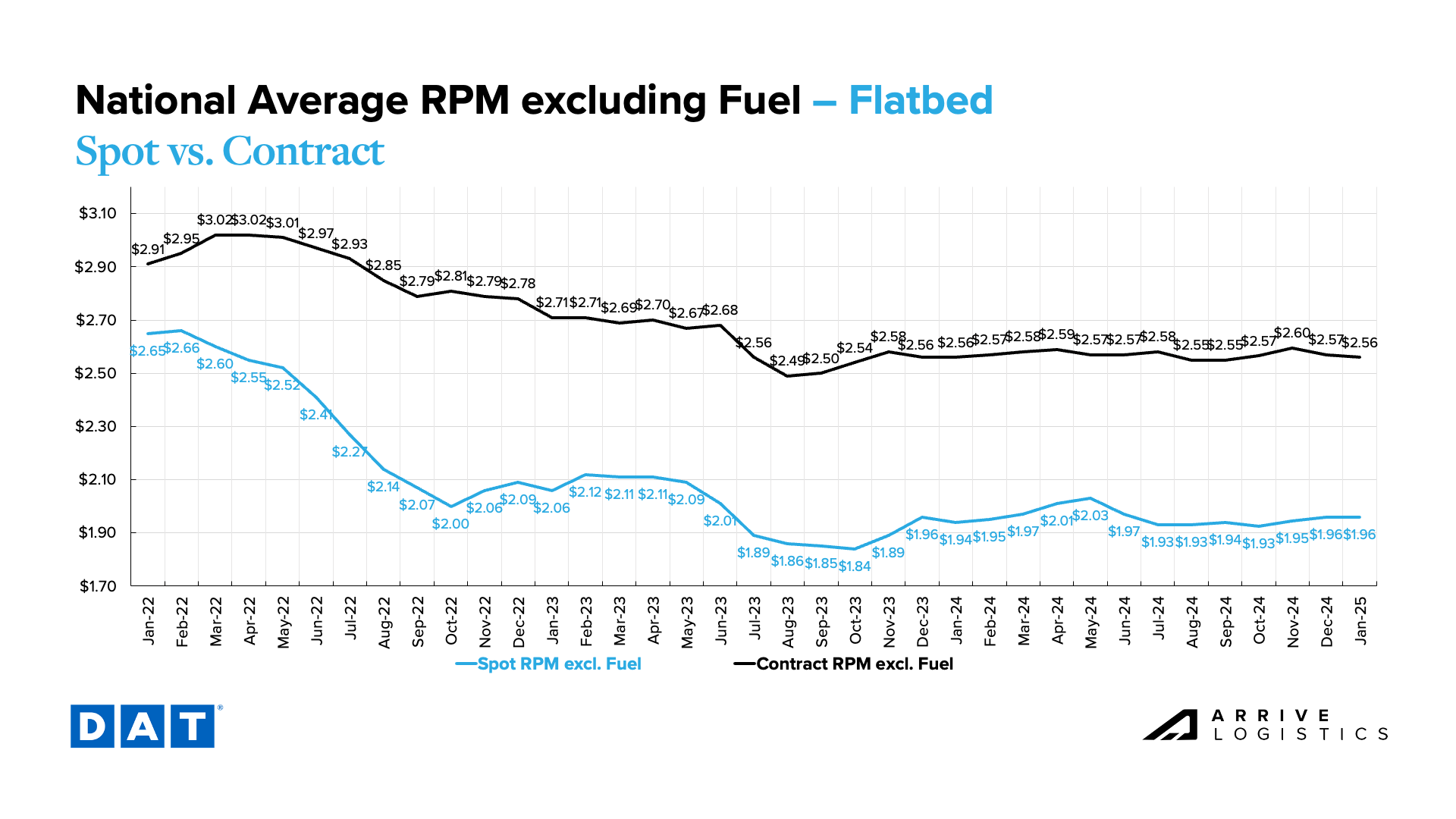

The flatbed market remains significantly more stable than van and reefer, with spot and contract linehaul rates sitting at $1.96 per mile and $2.56 per mile, respectively. The significant $0.60 per mile rate spread suggests the market is unlikely to experience any disruption in the near future. However, that could change as the building season drives increased activity in the spring.

Inflation ticked up to 3.0% in January due to increased food and energy prices. Core inflation, excluding food and energy, remained at 3.5%. While this raises speculation about potential interest rate cuts in 2025, the robust labor market and stubborn core inflation suggest that the Fed may keep interest rates higher for an extended period, presenting a downside risk to freight demand.

Bank of America credit card data reveals that household spending rose 1.9% year-over-year in January, following a 2.2% increase in December. Seasonally adjusted spending dipped 0.4% month-over-month, but the three-month annualized rate (SAAR) climbed 2.8%. Because services spending outpaced goods, the freight market is unlikely to benefit much.

Bank of America, Total Card Spending per Household

Bank of America, Total Card Spending per Household