The Morgan Stanley Dry Van Freight Index measures relative supply; the higher the index, the tighter the market conditions. The black line with triangle markers on the chart provides a great view of what directional trends would be in line with normal seasonality based on historical data dating back to 2007.

The mid-September reading showed trends following the 10-year average: Tightening in early to mid-July and then softening. Based on historical patterns, we expect increasing challenges through the end of Q3, followed by easing pressure in early Q4. The index is also up year-over-year, indicating a similar story as tender rejection and load-to-truck ratio data.

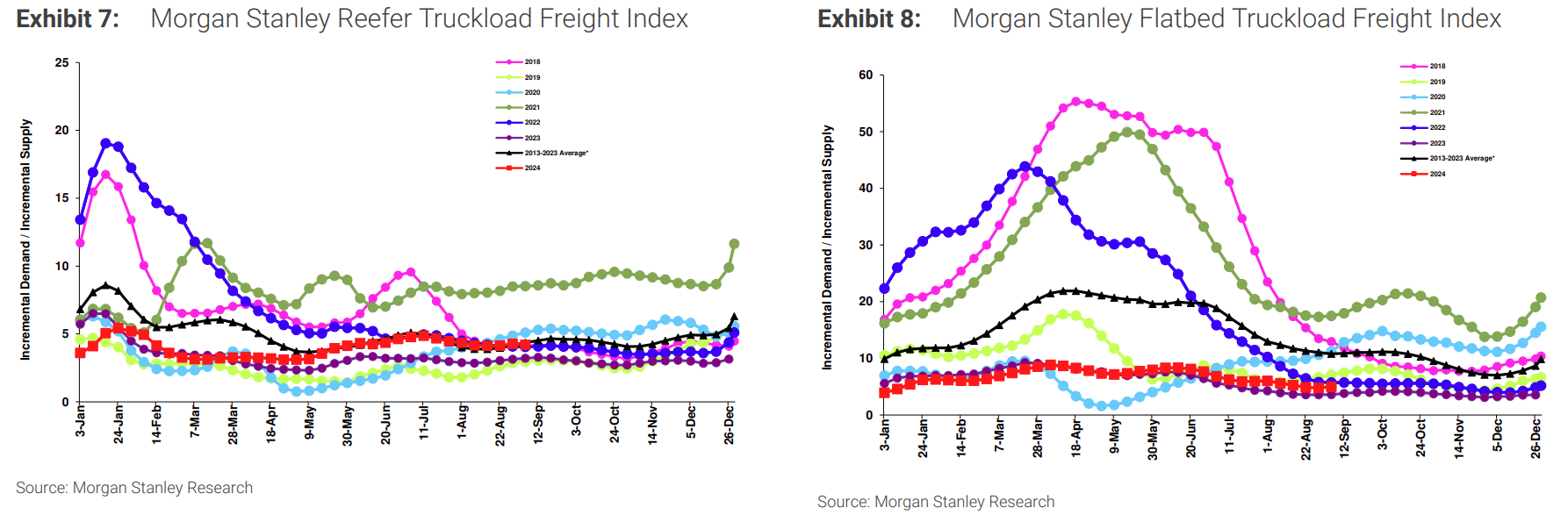

The reefer index continues to closely follow the 10-year average, while the flatbed index is well below the historical average but in line with 2023 levels.

Morgan Stanley Dry Van Truckload Freight Index

Morgan Stanley Reefer and Flatbed Truckload Freight Indices

Morgan Stanley Reefer and Flatbed Truckload Freight Indices

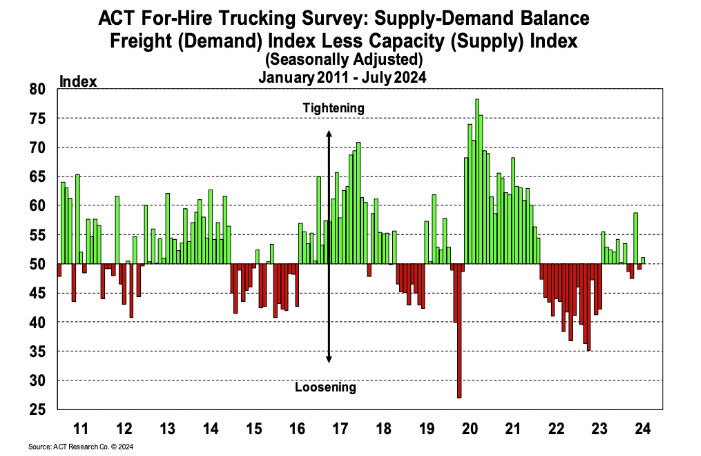

The ACT For-Hire Trucking Supply-Demand Balance Index rose from 49.0 in June to 51.1 in July, likely due to growing freight volumes and declining fleet capacity. However, it is important to note that ongoing private fleet expansion is not captured in this data. As the U.S. economy continues to rebound, increasing freight volume should be an upside risk in 2025.

ACT For-Hire Trucking Survey

ACT For-Hire Trucking Survey

Despite persistently low rates, resilient carriers have helped keep capacity steady and sufficient to service demand. Limited and low-rate spot market opportunities continue to encourage carriers with contractual volume to capitalize on strong rates by honoring their commitments. While obtaining precise capacity data remains challenging, recent trends and flattening rates indicate market stability as we move into Q4.

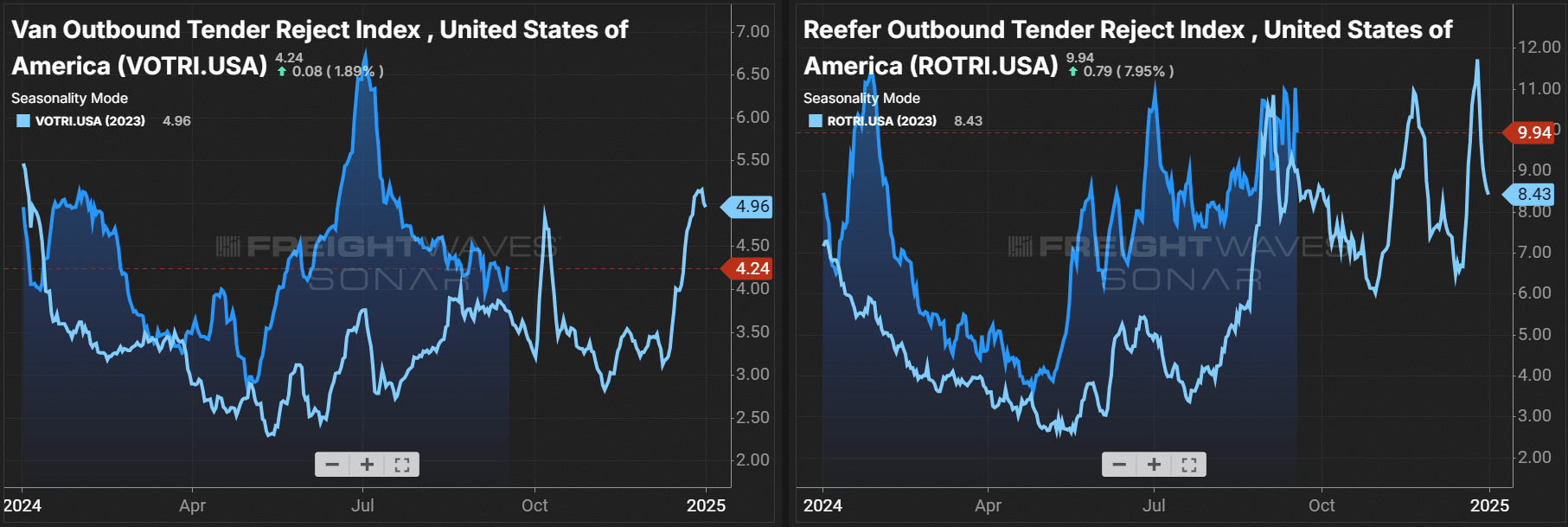

The Sonar Outbound Tender Reject Index (OTRI), which measures the rate at which carriers reject the freight they are contractually required to take, remains closely in line with September 2023. There has been no significant routing guide disruption since the Fourth of July, which should continue, save for any unforeseen events. 2023 curves on the van and reefer tender rejection charts are a strong predictor of routing guide challenges as the year progresses.

On a year-over-year basis, temp control equipment volatility increased through the summer peak season but was lower through Labor Day. This trend deviates from past peak seasons but aligns with typically soft dry van trends through mid-Q3. Despite the recent softness, we expect increased temp control tender rejections over the next few months, especially in the Pacific Northwest and Upper Midwest, ahead of Thanksgiving and Christmas.

Outbound Tender Reject Index (SONAR)

Outbound Tender Reject Index (SONAR)

Van & Reefer Outbound Tender Reject Indices

Van & Reefer Outbound Tender Reject Indices

The DAT Load-to-Truck Ratio measures the total number of loads relative to the total number of trucks posted on its spot board. The dry van reading continues to decline, reaching 3.64 in August. This aligns with expectations, as decreased volume and stable capacity lead to lower load-to-truck ratios. Reefer markets followed a similar trend, with load-to-truck ratios falling to 5.96 in August.

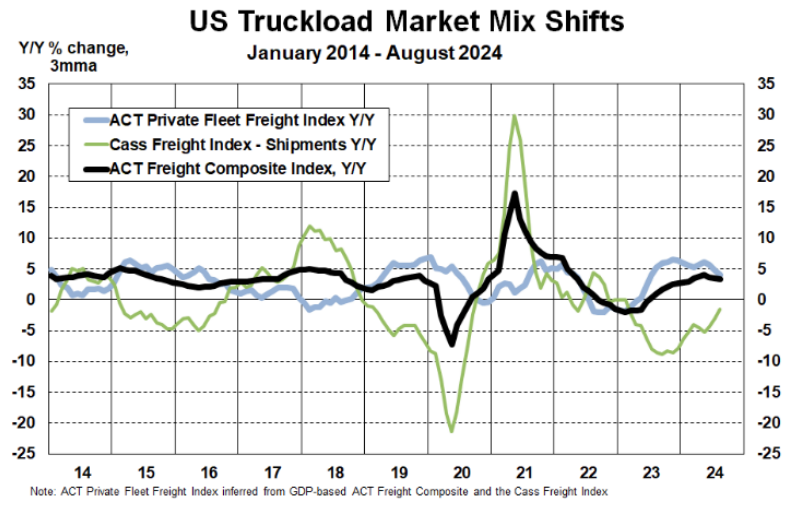

Private fleet investment in expanding tractor counts is boosting their share of truckload volumes. This growth is reducing spot market demand and contributing to excess capacity in the market.

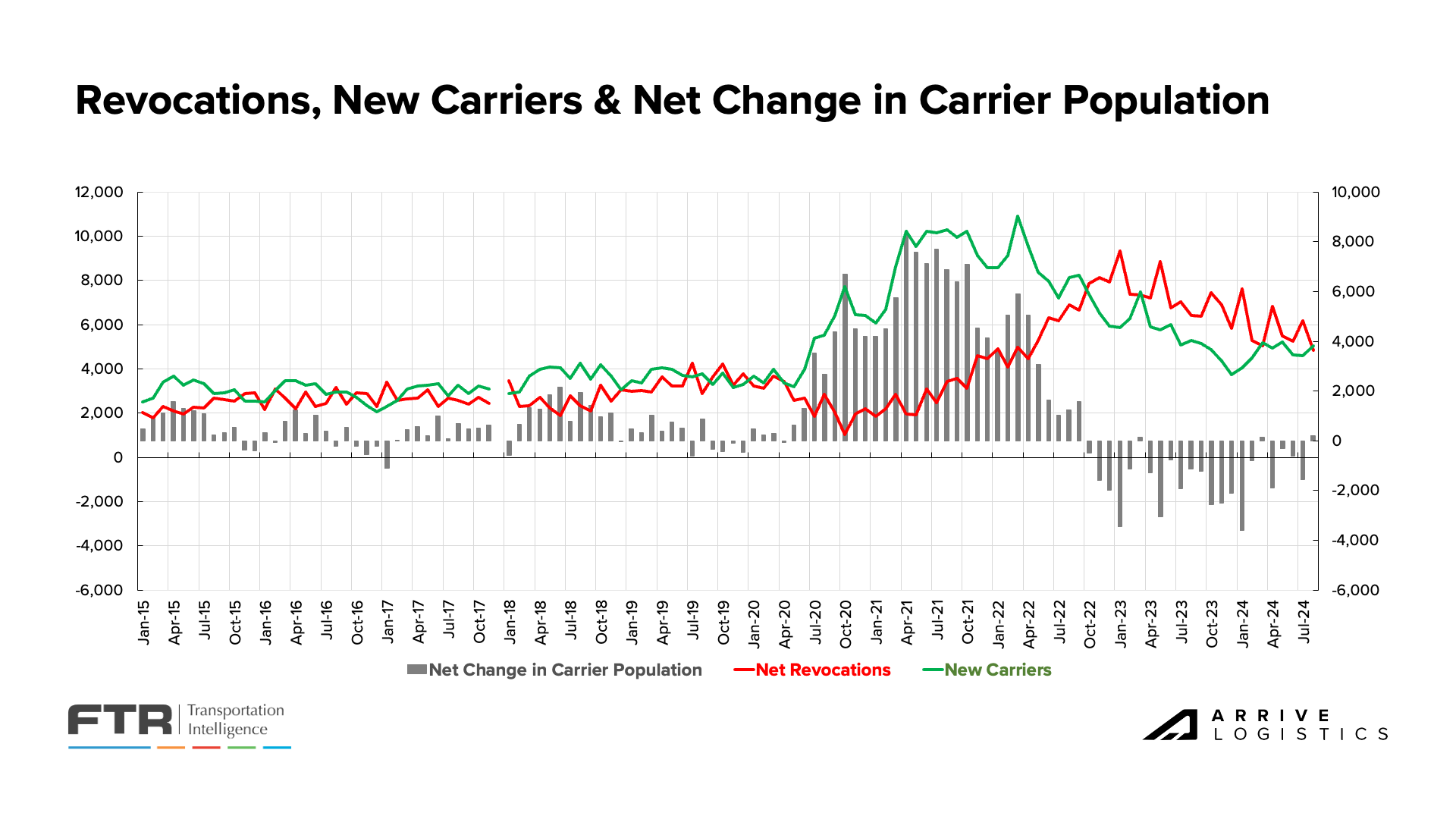

FTR’s latest revocation data showed a small carrier population increase for only the third time in the past 22 months. Revocations declined month-over-month amid increasing new carrier entrants, indicating the carrier population remains resilient despite low revenues and stable expenses. However, recent fuel price declines could offer carriers enough relief to hold out for potential revenue gains when rates tick up in Q4.

FTR’s Carrier Revocations, New Carriers & Net Change in Carrier Population

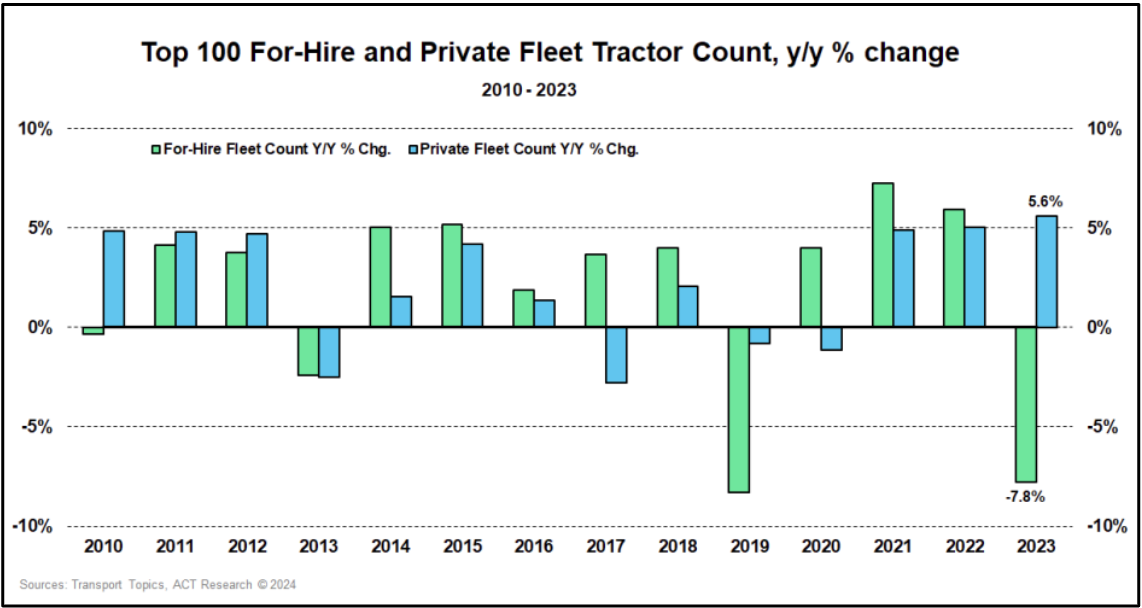

One of the more notable capacity trends of 2024 has been private fleets’ ongoing investments in expansion. In 2023, the top 100 private fleets grew tractor counts by 5.6%, while the top 100 for-hire fleets decreased tractor counts by 7.8%. Investments continued in 2024 based on anecdotes from Arrive’s private fleet network, who say expansion has helped them capture significant value. As a result, private fleet shipments are up around 5% year-over-year, while overall freight shipments are down around 1% year-over-year, indicating that private fleets have gained meaningful market share.

This trend could last deep into 2025 as private fleets continue to secure volumes that historically would be available in the for-hire market. In turn, for-hire spot market demand could suffer, as could opportunities for carriers seeking backhauls to their outbound markets. These factors would create downward rate pressure and easing spot market supply conditions.

Top 100 For-Hire and Private Fleet Tractor Count, Y/Y % Change, ACT Research

Top 100 For-Hire and Private Fleet Tractor Count, Y/Y % Change, ACT Research

US Truckload Market Mix Shifts, ACT Research & Cass Freight Index

US Truckload Market Mix Shifts, ACT Research & Cass Freight Index

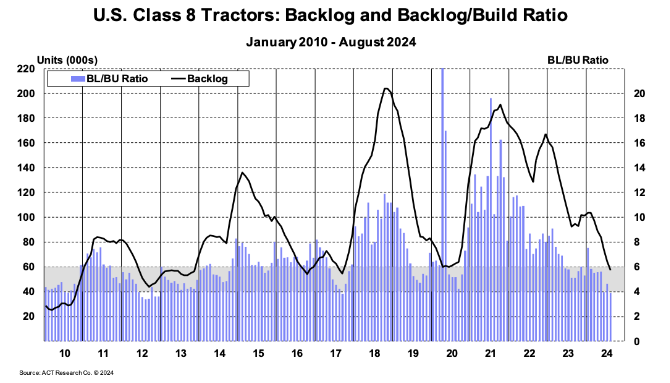

Based on the latest ACT Research data for U.S. Class 8 Tractors, the backlog-to-build (BL/BU) ratio dropped to 3.9 months in August. If this data holds, it would be the lowest BL/BU ratio since late 2017. Additionally, the Class 8 Tractor Backlog fell to 57,000 units at the end of August, marking a 7-year low and a meaningful decline from the 67,000 unit backlog reported at the end of July.

ACT Research, U.S. Class 8 Tractors: Backlog and Backlog/Build Ratio

ACT Research, U.S. Class 8 Tractors: Backlog and Backlog/Build Ratio

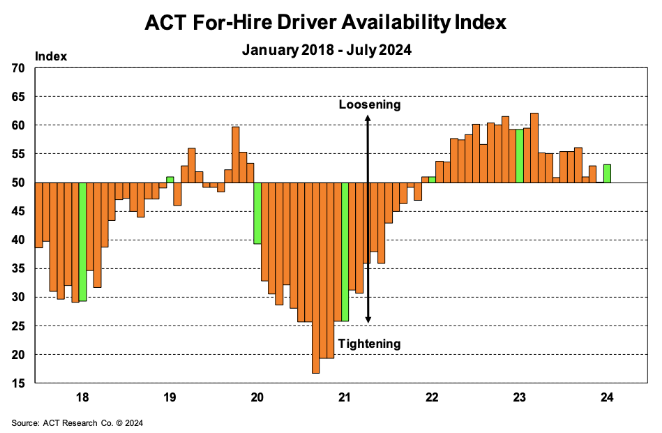

The ACT For-Hire Driver Availability Index rose to 53.1 in July from 50.0 in June, marking the 26th consecutive month the index has shown loosening conditions. The reason for the trend remains the same: Older drivers who are staying in the market to keep up with the higher cost of living combined with the influx of new CDLs issued during the pandemic.

ACT For-Hire Trucking Index: Driver Availability

ACT For-Hire Trucking Index: Driver Availability

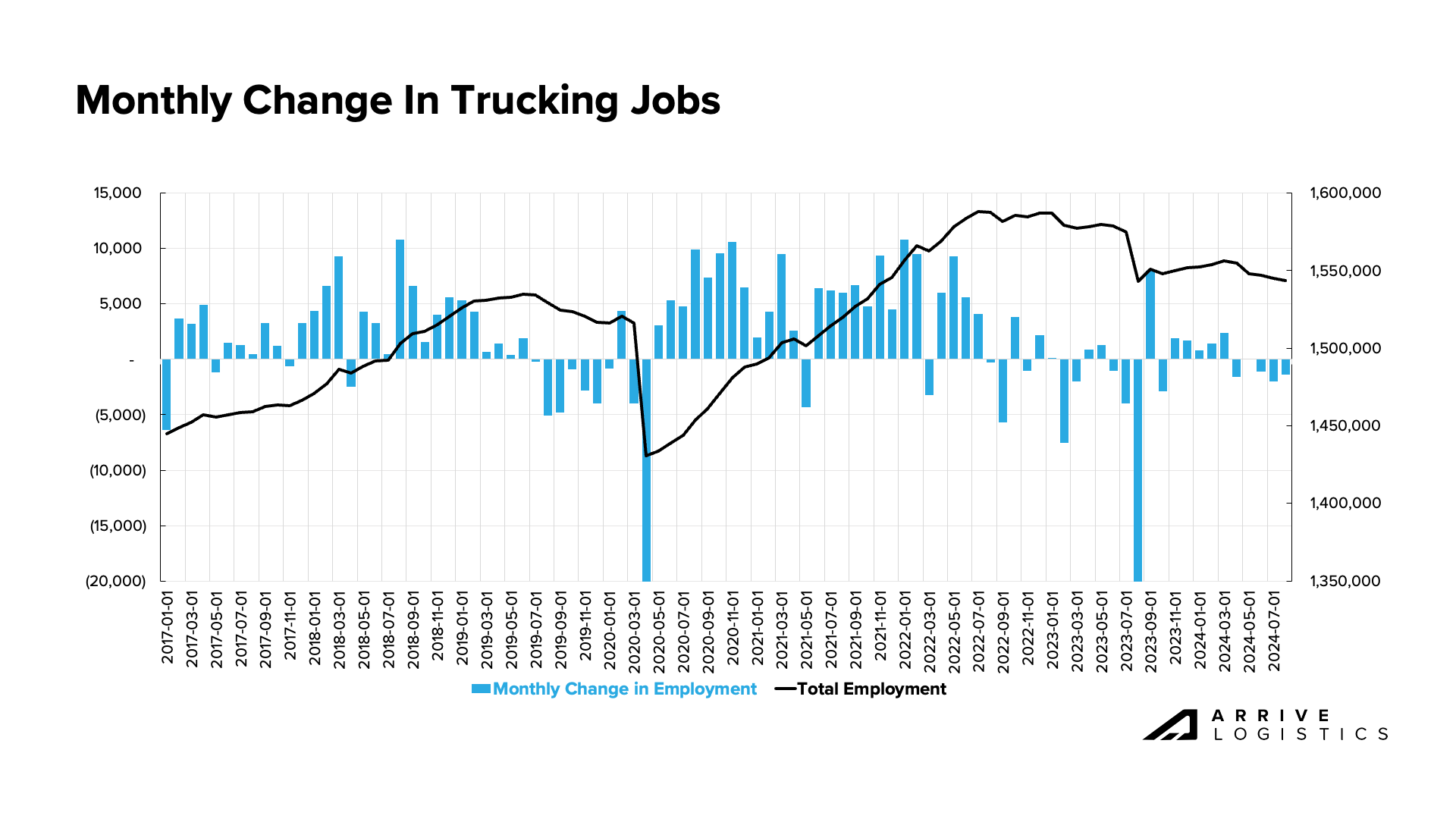

Trucking jobs fell by 1,400 in August due to persistently poor spot rate conditions and increased competitiveness on contractual rates. This was the fifth consecutive month of seasonally adjusted job losses, with nearly 13,000 jobs lost since the April report. Anecdotally, there is no reason to expect much volatility in the spot market through the remainder of the year based on how easily supply handled Labor Day demand. Our forecast shows that significant rate recovery is still some time away, so we expect a continued reduction in carrier market participants.

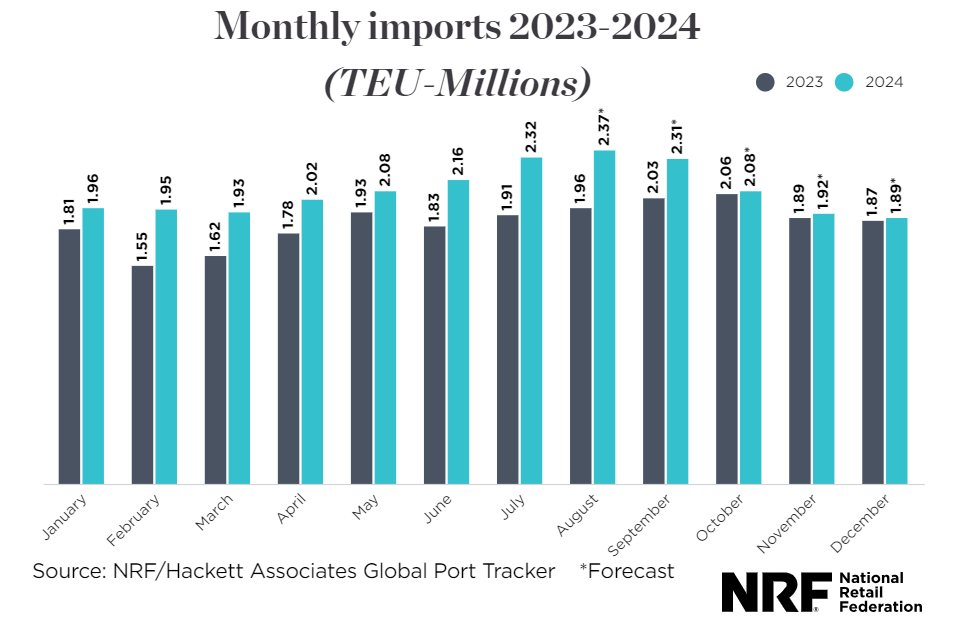

Forecasts continue to show stable freight volumes. Both upside and downside risks are present, but there is no clear indication that demand shifts will impact the market in the near term. The latest National Retail Federation’s (NRF) forecast calls for year-over-year import increases for the remainder of 2024, with 25 million TEUs expected in total. This would be an increase of 12.1% from 2023 and half a million less than in 2022.

However, delays are expected due to the port strike. Some retailers rushed to bring in shipments ahead of the strike or rerouted them to West Coast ports. If the strike lasts longer than a few days, a large backlog could build and create significant volatility when ports reopen.

NRF Monthly Imports

NRF Monthly Imports

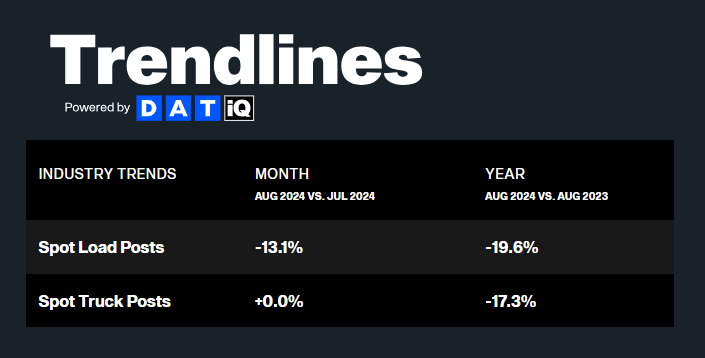

DAT reports that spot load postings fell by 13.1% month-over-month in August and were down nearly 20% from August 2023. The month-over-month decline follows seasonal expectations as August tends to be quieter than July. While the year-over-year decline seems large, it significantly improved from the 41.4% year-over-year decline in August 2023. This trend indicates that traditional spot load boards are experiencing reduced activity due to not only lower truckload volumes but other factors as well, such as theft risk, rate API utilization and private fleet insourcing.

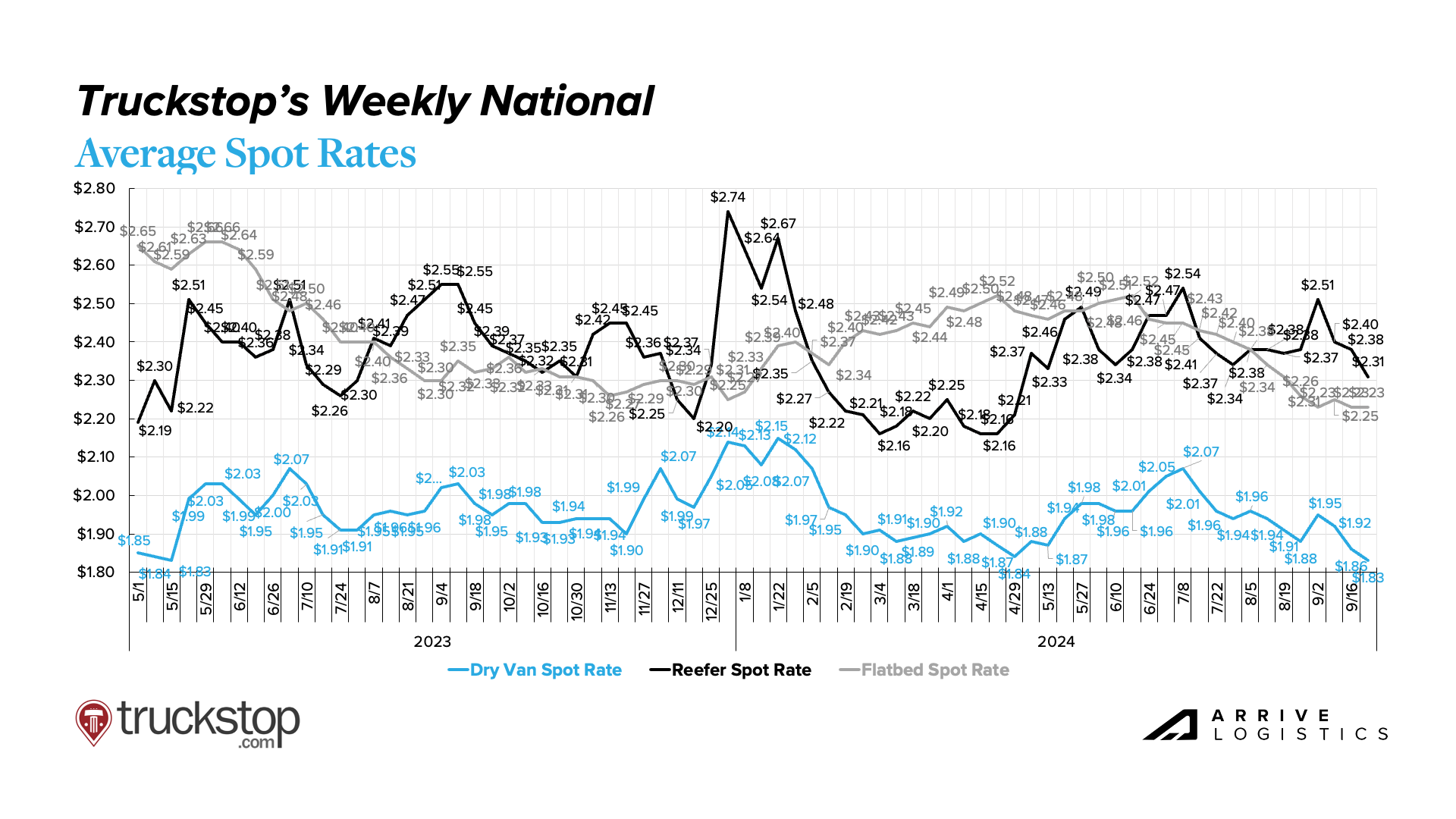

As supply and demand find balance, rates are following the floor and deviating in line with typical seasonality. Rates rose around Labor Day but fell shortly after, as expected.

We anticipate rate fluctuations similar to 2023 as Q4 begins, with volatility increasing in certain regions. However, the East and Gulf Coast port strikes and more fallout from hurricane season could cause routing guide shake-ups if the right conditions materialize.

Truckstop Weekly National Spot Rate Average

Truckstop Weekly National Spot Rate Average

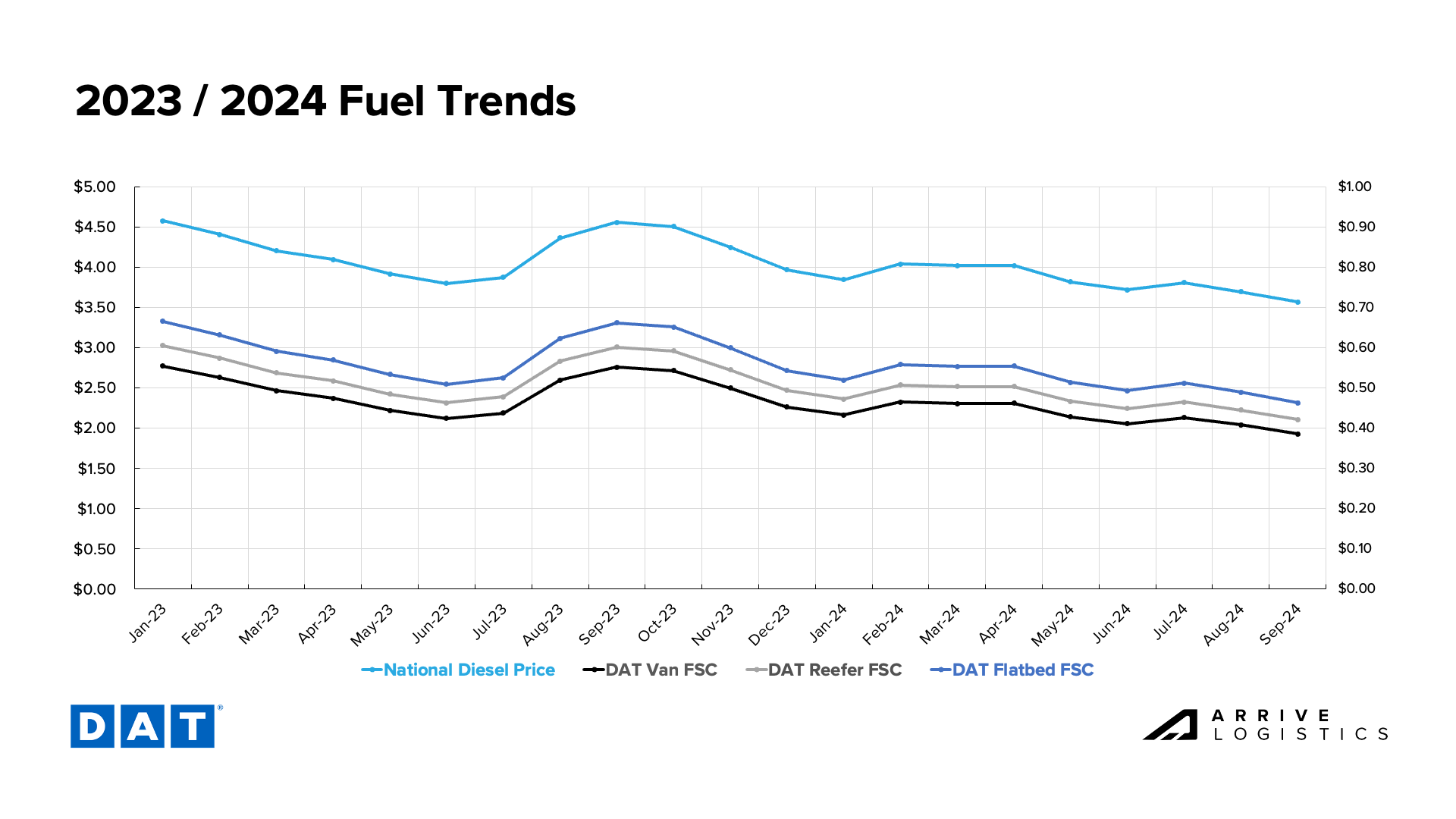

National diesel prices continue to decline steadily, offering relief to carriers with lower fuel efficiency. The decline comes amid elevated domestic fuel inventories, strong production and falling demand. Though Hurricane Helene created some temporary fuel price volatility, overall, prices should remain low.

DAT Fuel Trends

DAT Fuel Trends

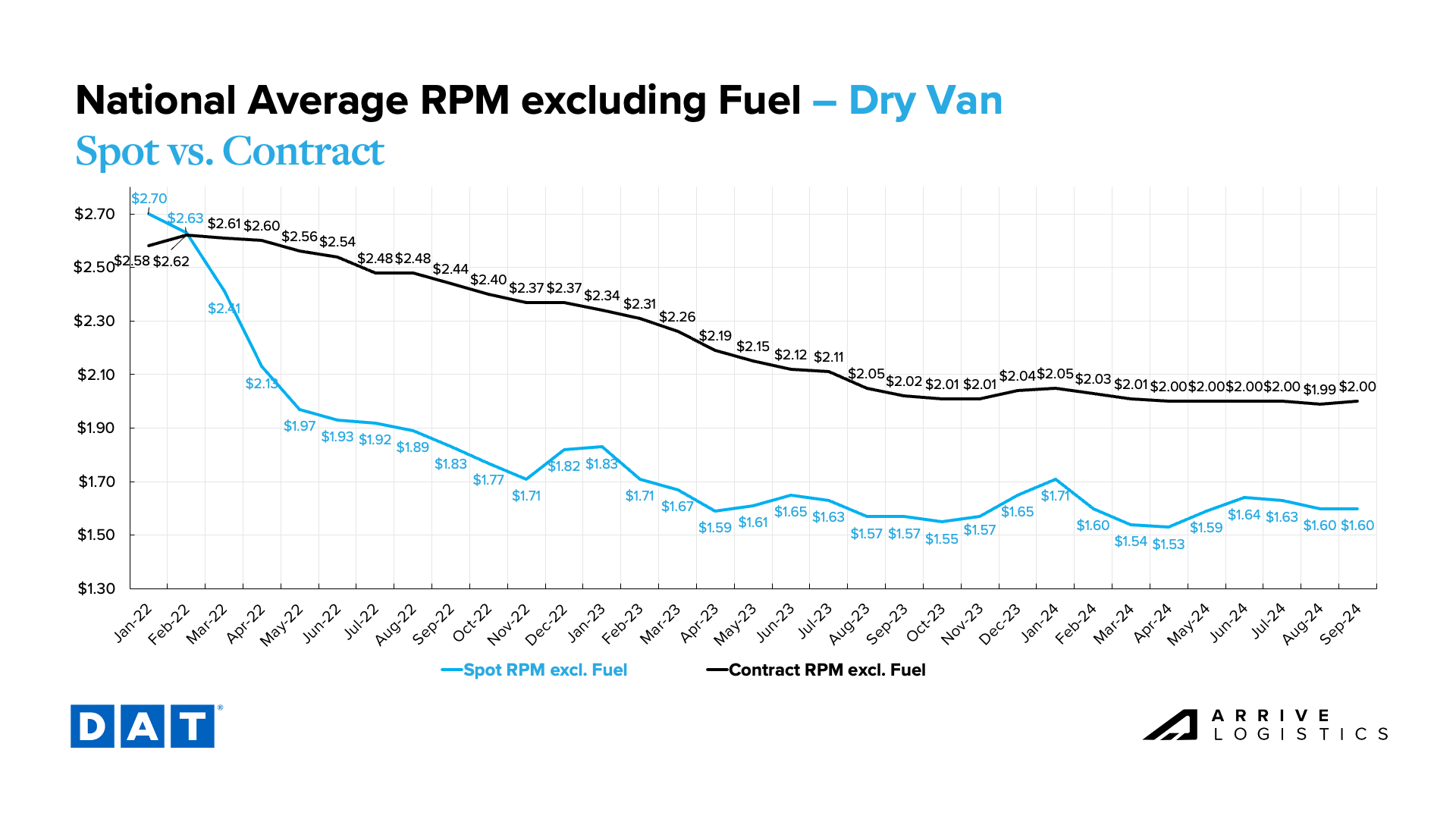

As fuel prices fell, DAT reported flat dry van linehaul rates of $1.60 per mile in September, reflecting spot market stabilization following the summer peak season. Contract rates are steady but have increased slightly through mid-September — if current rate trends hold, this would be the first month of sequential contract rate increases since January 2024. At $0.40 per mile, the spot-contract gap remains historically wide, leading to a highly resilient market environment.

DAT Dry Van National Average RPM Spot vs. Contract

DAT Dry Van National Average RPM Spot vs. Contract

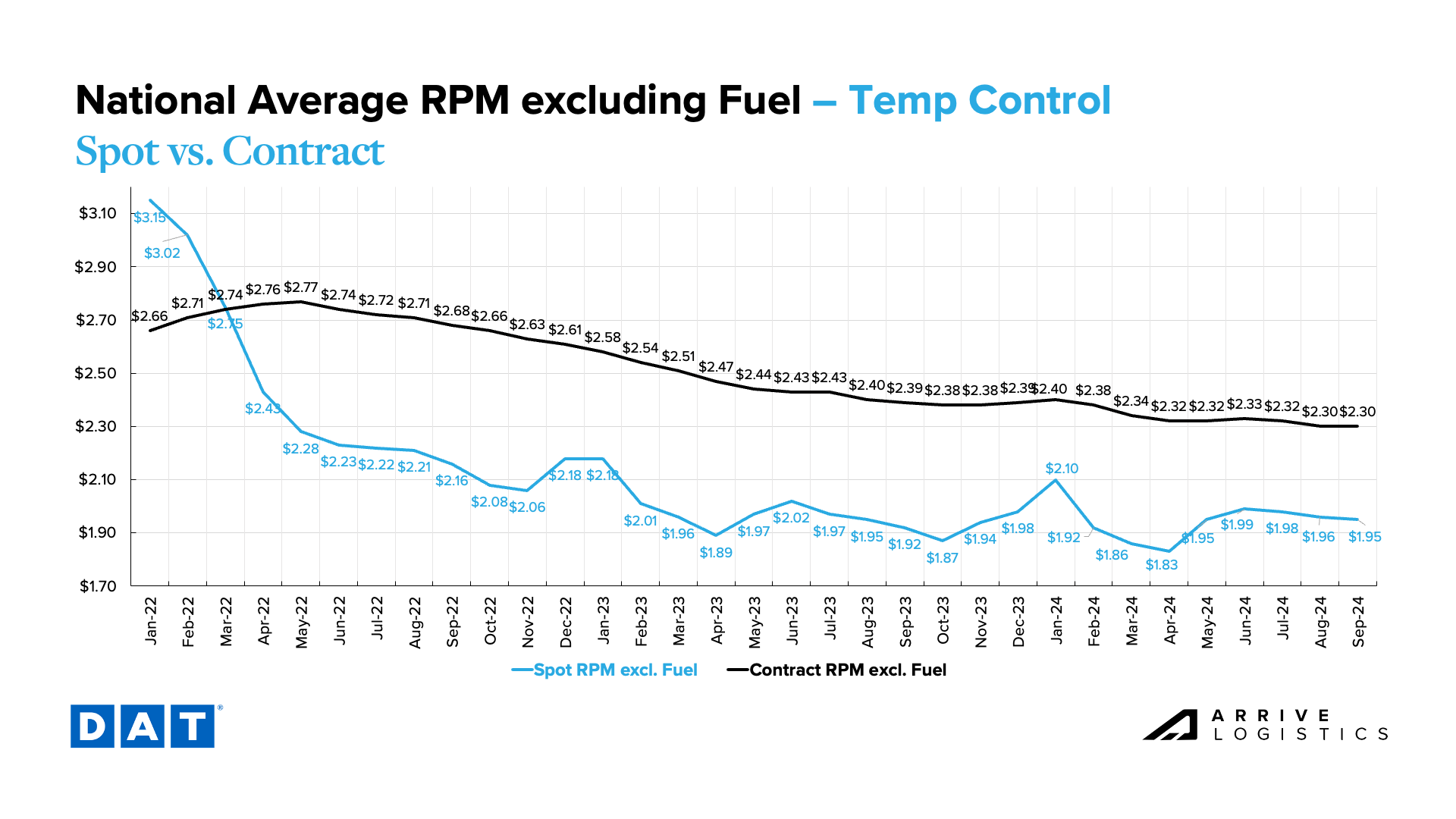

The reefer market has settled, with trends mirroring the dry van market. Month-over-month spot rates were flat through mid-September, hovering around $1.96 per mile. Temp control rates were flat through the summer, but we expect them to tick up later in Q4, especially in northern states. Contract rates have remained stable, limiting the pressure of a closing spot-contract rate gap, although conditions are slightly tighter than for dry van freight.

DAT Temp Control National Average RPM Spot vs. Contract

DAT Temp Control National Average RPM Spot vs. Contract

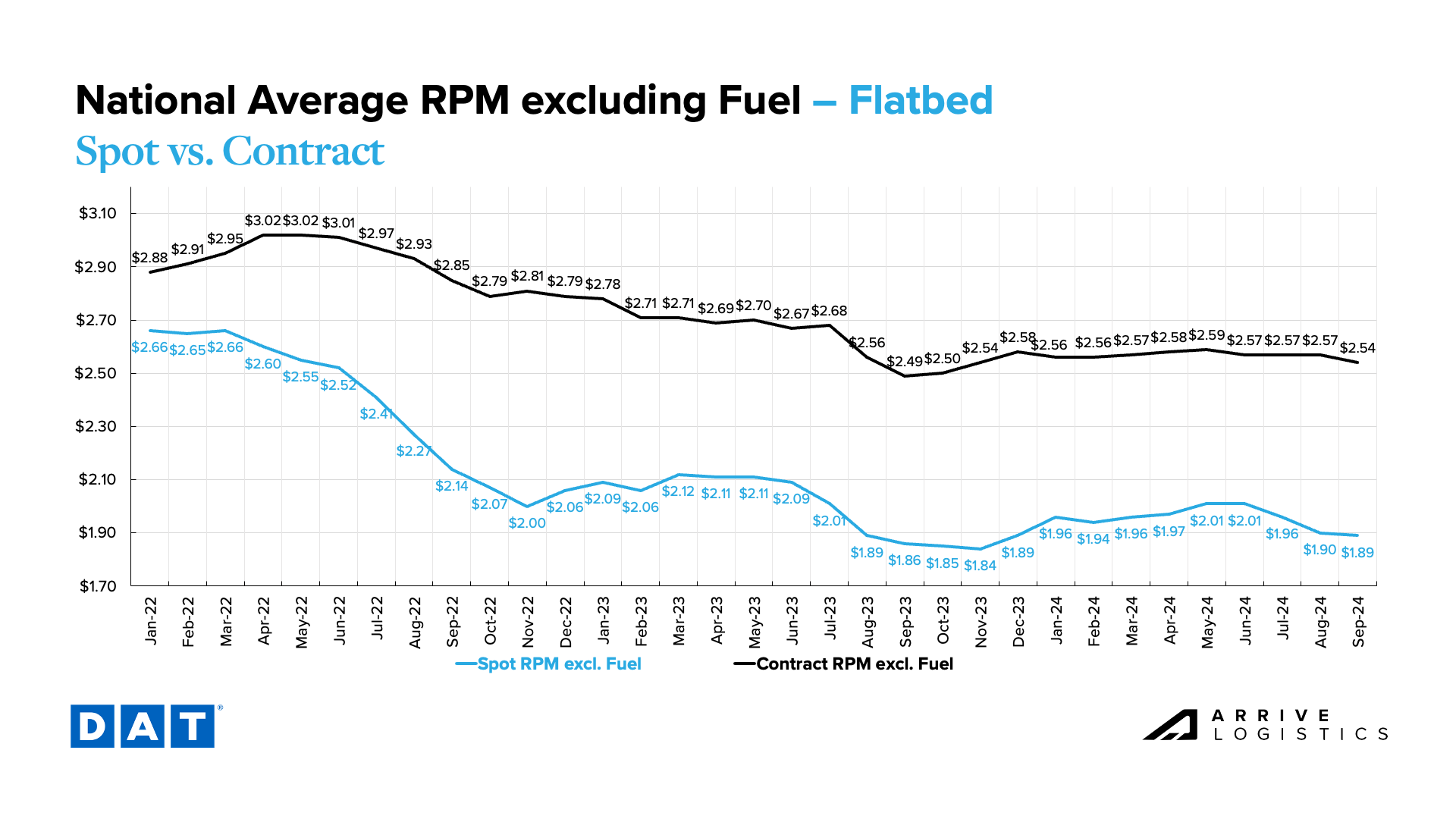

Flatbed rates continue to deviate from dry van and temp control trends. Open-deck spot rates are down from the summer peak as projects wrap up ahead of winter, but contract rates remain steady, hovering $0.66 per mile above current spot rates.

DAT Flatbed National Average RPM Spot vs. Contract

DAT Flatbed National Average RPM Spot vs. Contract

In September, the Fed cut interest rates for the first time in four years. The cut of 50 basis points indicates that the Fed believes the economy has slowed and they must now spur economic activity. Future cuts are the primary upside forecast risk, especially if several more happen this year. Lower interest rates should drive spending and positively impact freight volumes, but we are unlikely to see the impact until at least the first half of 2025.

Inflation continues to trend in the right direction, reaching 2.5% in August, the lowest level since the pandemic began. Falling inflation rates are a welcome sign for consumers, although it still may be some time before spending activity shifts meaningfully.

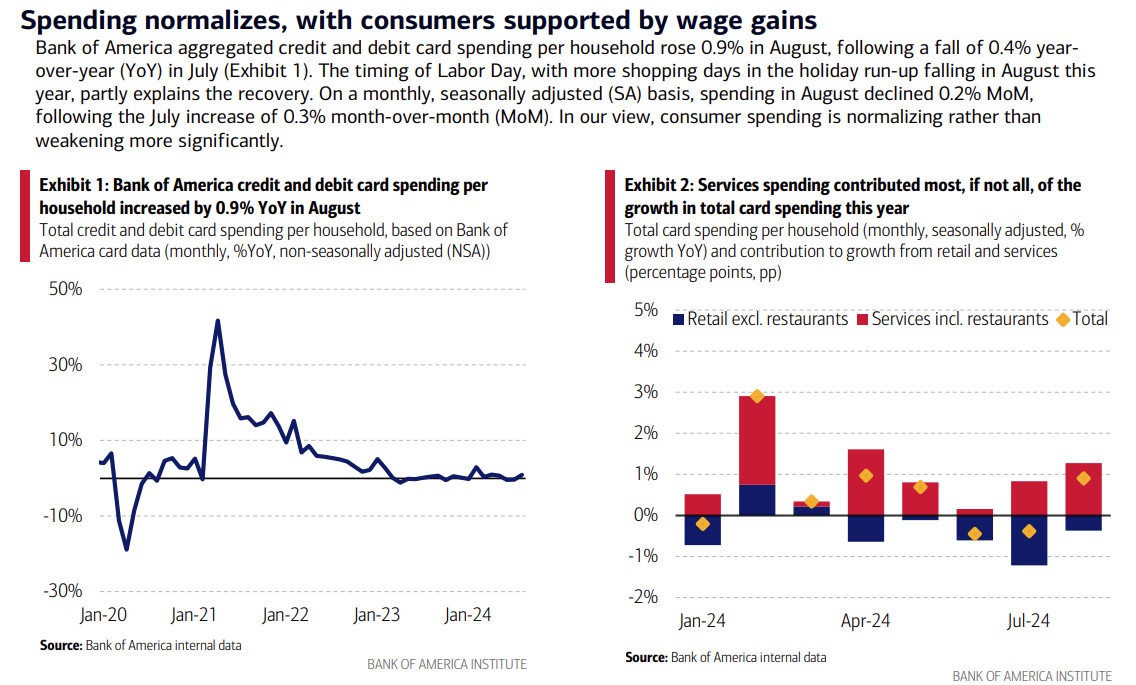

Bank of America continues to show credit card spending stability, reporting a 0.9% year-over-year increase in August that was aided by the timing of Labor Day, which allowed for more “shopping days” this year. As a result, seasonally adjusted spending was down 0.2% in August. Goods spending declined year-over-year, with only February and March showing year-over-year growth. Additionally, back-to-school spending was weaker than in 2023, which could have resulted from declining inflation.

Ultimately, economic spending trends look stable. Declining interest rates indicate potential spending growth in 2025, which would positively impact freight volumes.

Bank of America, Total Card Spending per Household

Bank of America, Total Card Spending per Household