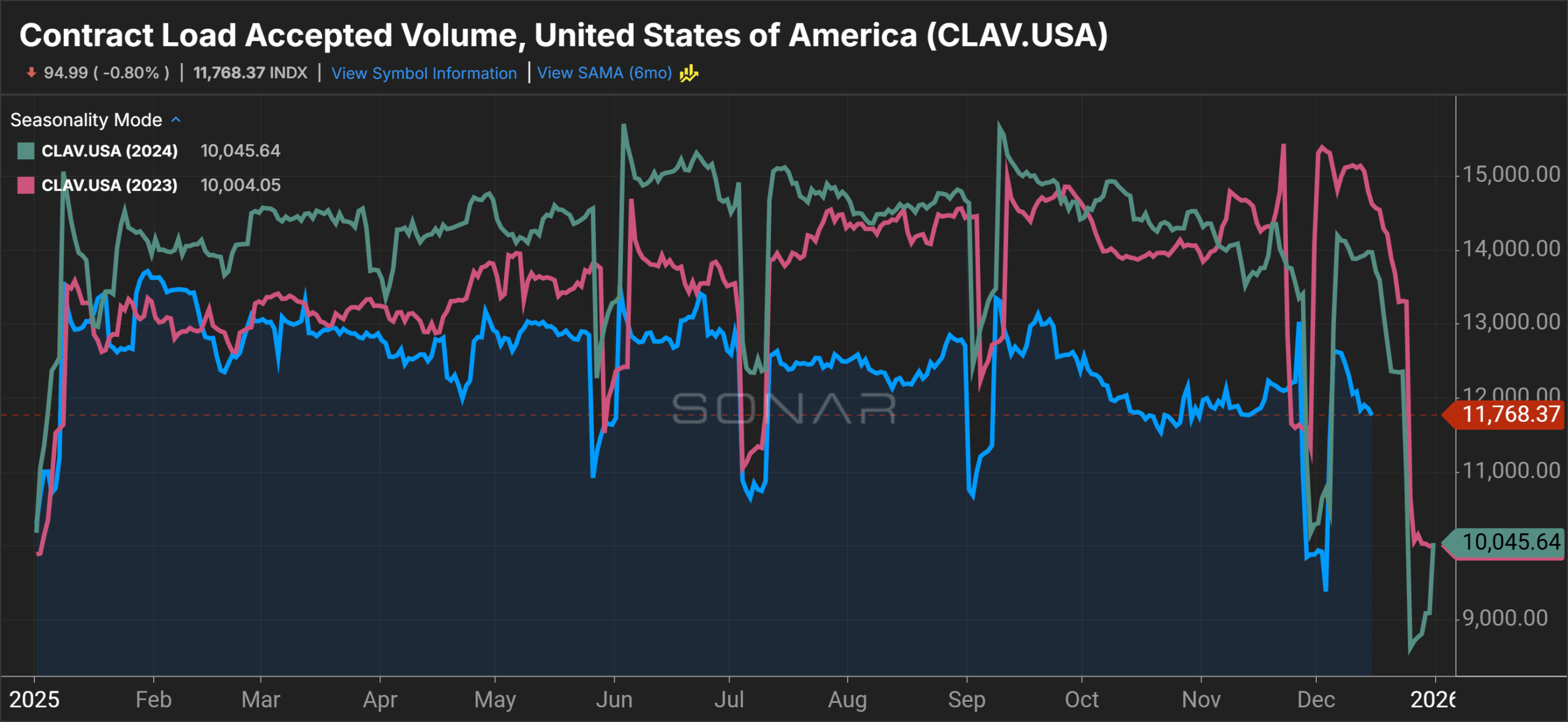

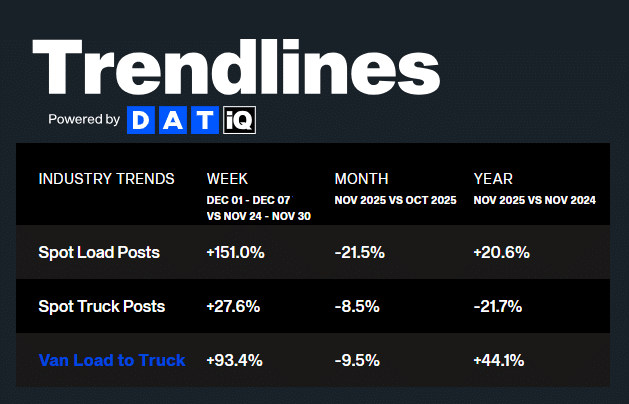

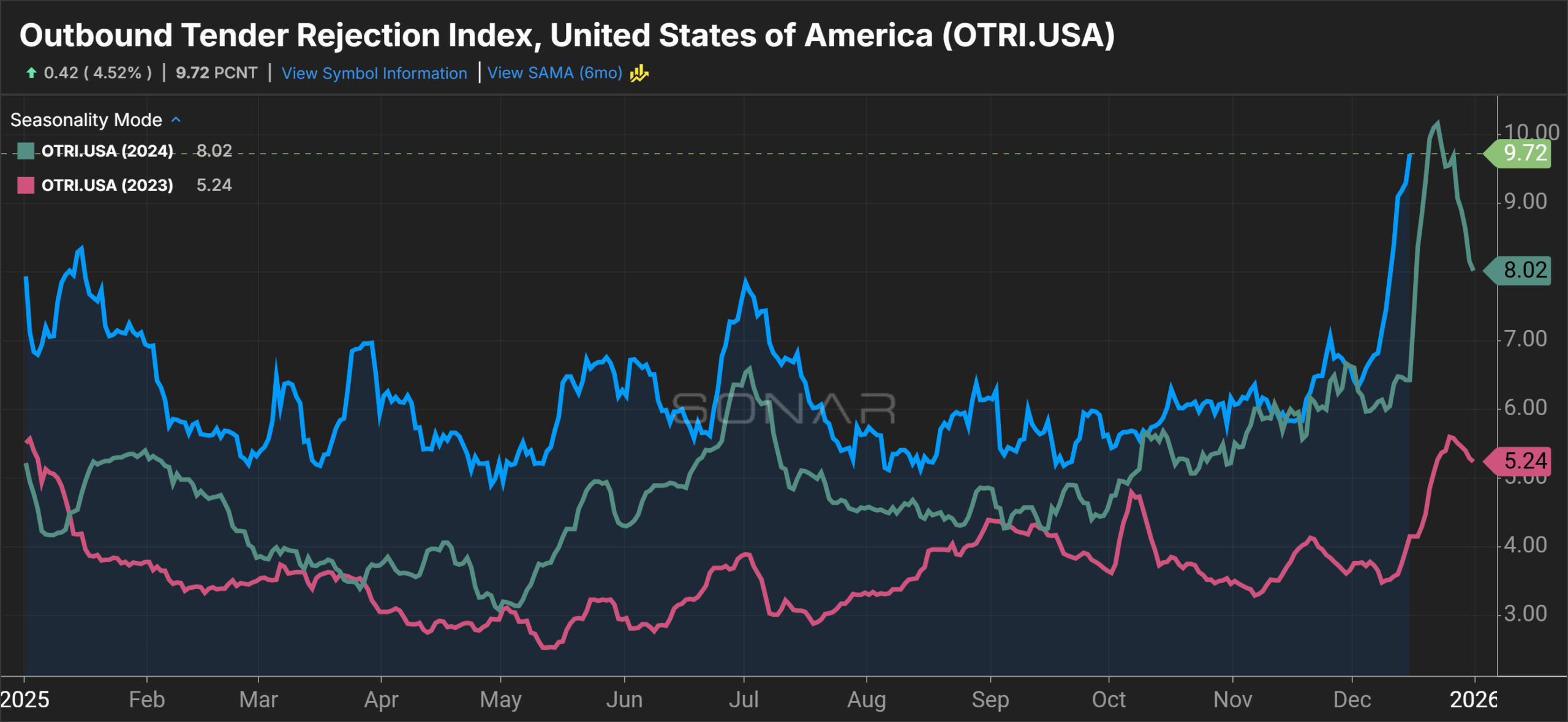

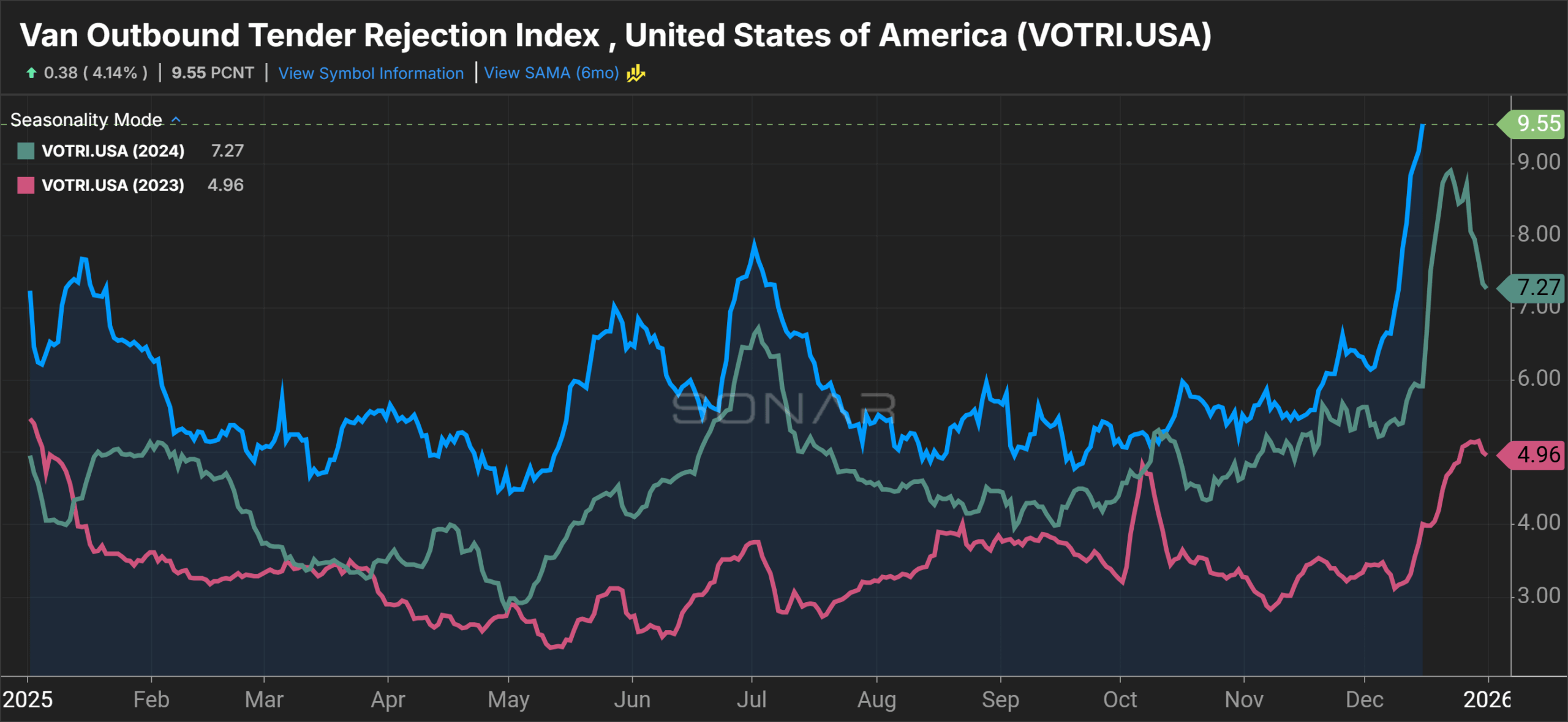

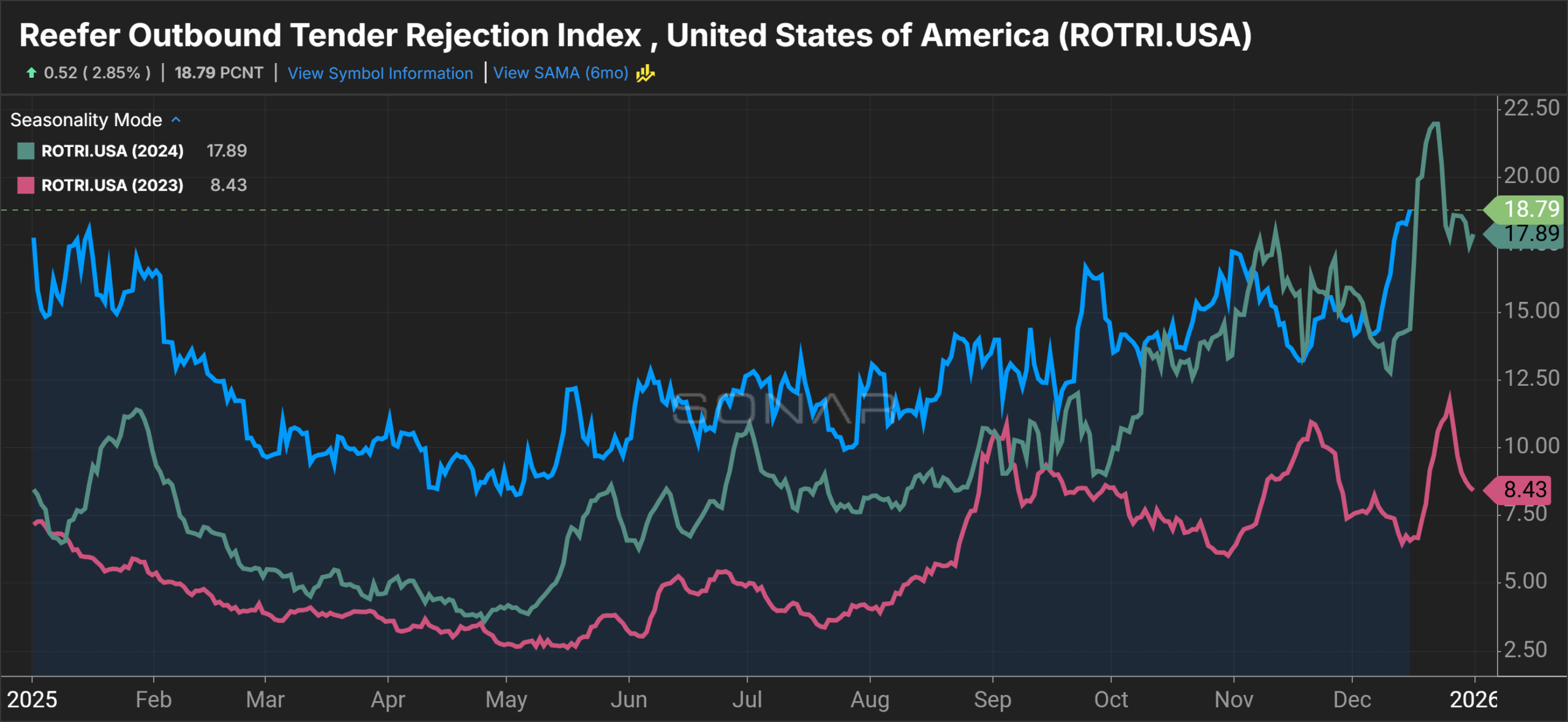

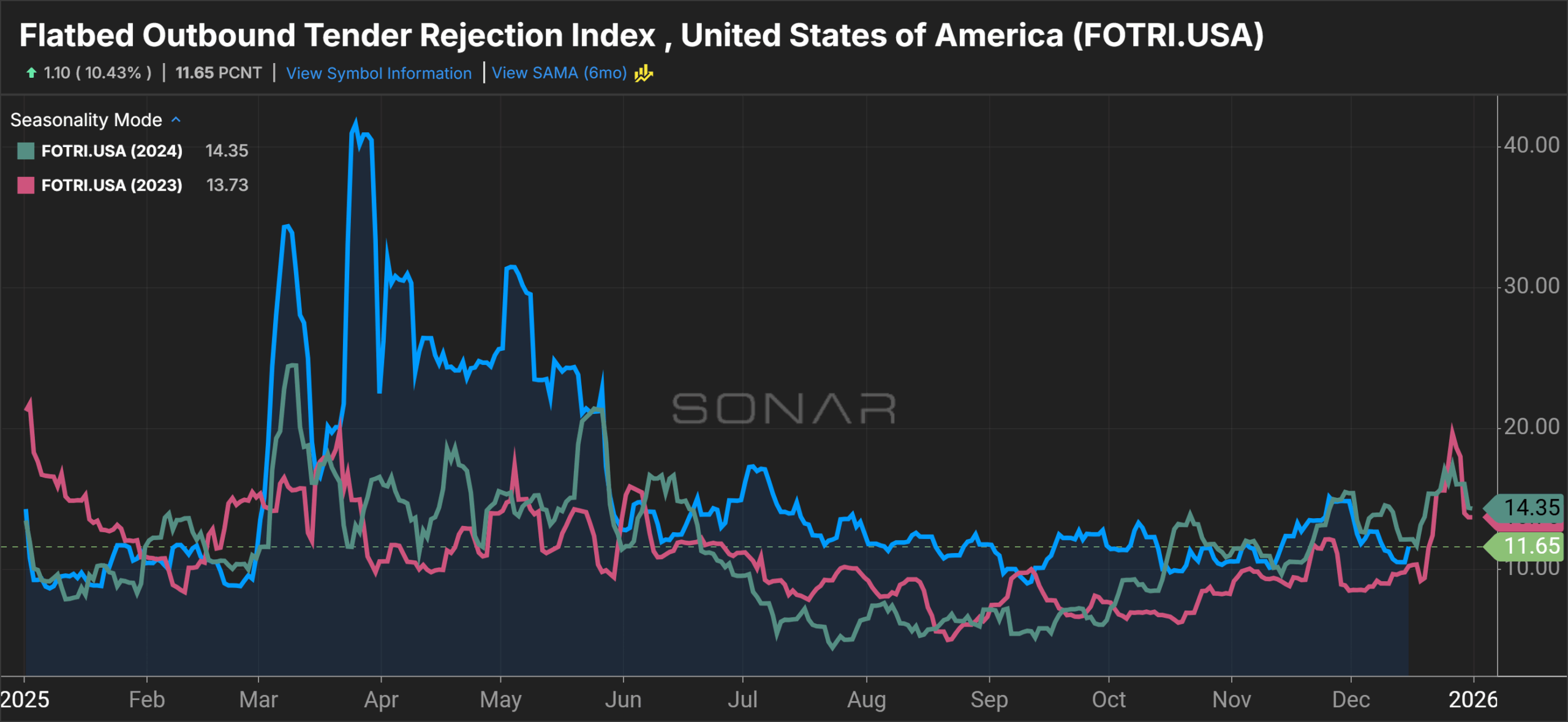

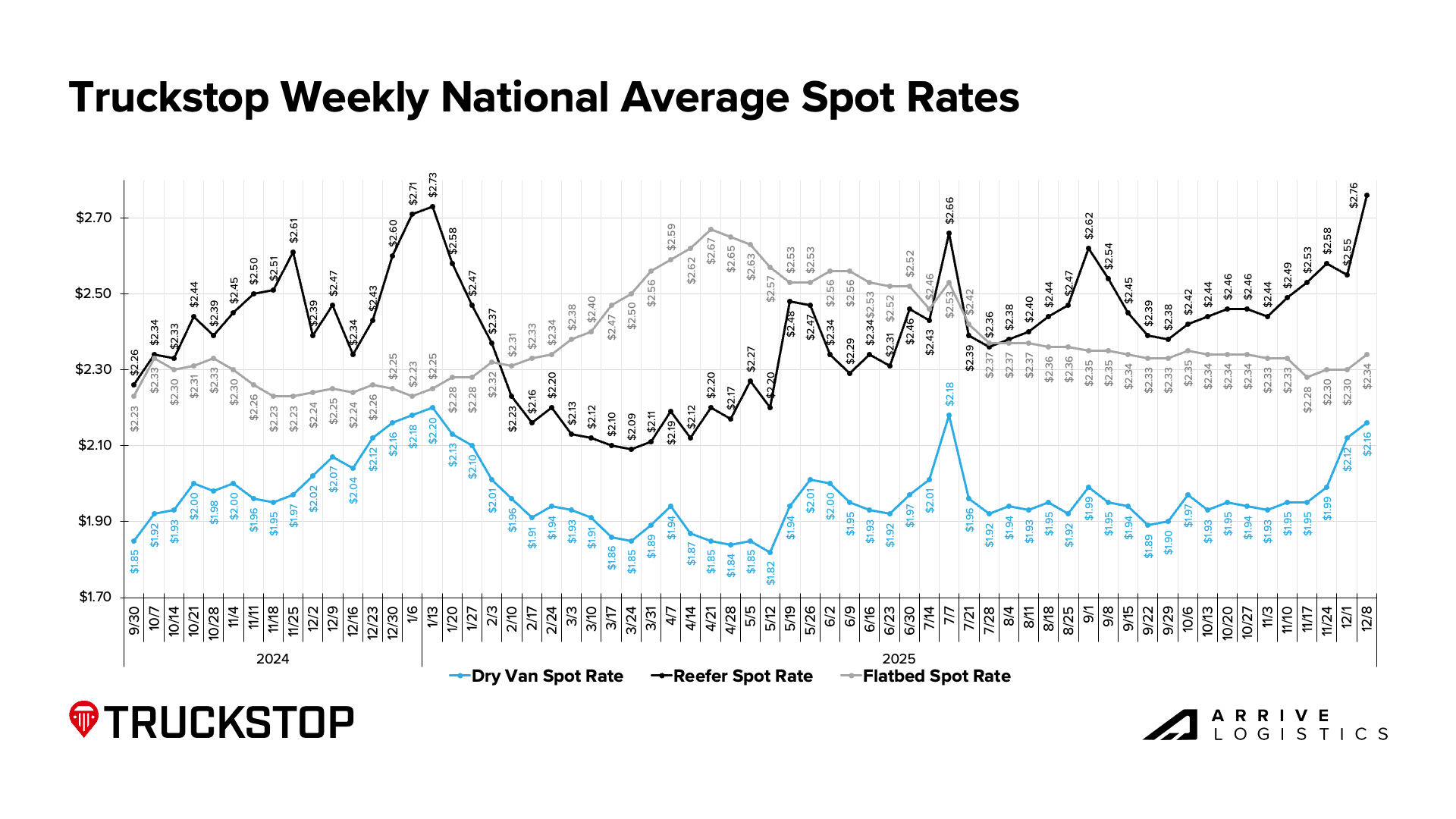

The holiday peak season has been anything but quiet. Despite weak overall demand, a stretch of seasonal bumps and winter weather events in early December sent tender rejections soaring to the highest levels since early 2022, sparking a surge of spot activity in turn. The resulting tightness will likely continue building through year-end as winter storms move across the Midwest and Northeast and more drivers take holiday time off.

While this stretch of volatility alone is unlikely to drive a meaningful shift in macro conditions, it does make clear that the market is firmly in balance and vulnerable to sustained disruption in 2026. Exactly when that might occur depends on several variables, starting with demand.

For now, volumes remain weak aside from seasonal influences and should return to pre-holiday levels once conditions normalize in mid to late January. Imports are also down more than 10% year-over-year in Q4 following the summer pull-forward boom, offering little to no near-term relief.

Looking ahead, tariff policy will be a key demand variable in 2026. Greater clarity around enforcement and progress toward a renewed North American trade agreement may help stabilize cross-border flows and spur a manufacturing recovery, but the broader implications for demand remain uncertain until tariff impacts fully work their way through the economy.

On the consumer side, the National Retail Federation expects holiday retail sales to exceed $1 trillion, meaning that spending continues despite inflation. That strength will support near-term demand, but it also carries the risk of pushing inflation higher once tariff-driven price increases reach shoppers, which could ultimately soften freight volumes. Political developments ahead of the 2026 midterms add another layer of uncertainty, with the administration floating potential stimulus measures that would temporarily boost economic activity.

Supply also faces several meaningful risks heading into the new year. Low equipment orders persisted through November, shrinking the tractor population and limiting the market’s ability to absorb future demand shocks. Regulatory uncertainty — from the FMCSA’s non-domiciled CDL rules to sweeping driving-school audits — could also have a significant impact on capacity, depending on how enforcement plays out.

For now, expect volatility to continue well into January before conditions settle into a delayed post-holiday lull. Read on for a detailed breakdown of demand, supply, rates and economic conditions as they stand mid-month.