Winter Storm Fern slammed much of the country just as freight market conditions began to settle in mid-January, causing major disruptions that sent tender rejections higher and pushed spot rates to multi-year highs through month-end. That volatility stretched into early February as more snow and frigid temperatures hit the Southeast, Carolinas, Mid-Atlantic and parts of the Northeast.

Similar storms in recent years did not generate nearly this level of volatility, particularly in February, when demand typically softens and weather-related disruptions subside relatively quickly. While the worst of the storm’s impact has now passed, it’s clear the market is rapidly approaching a tipping point.

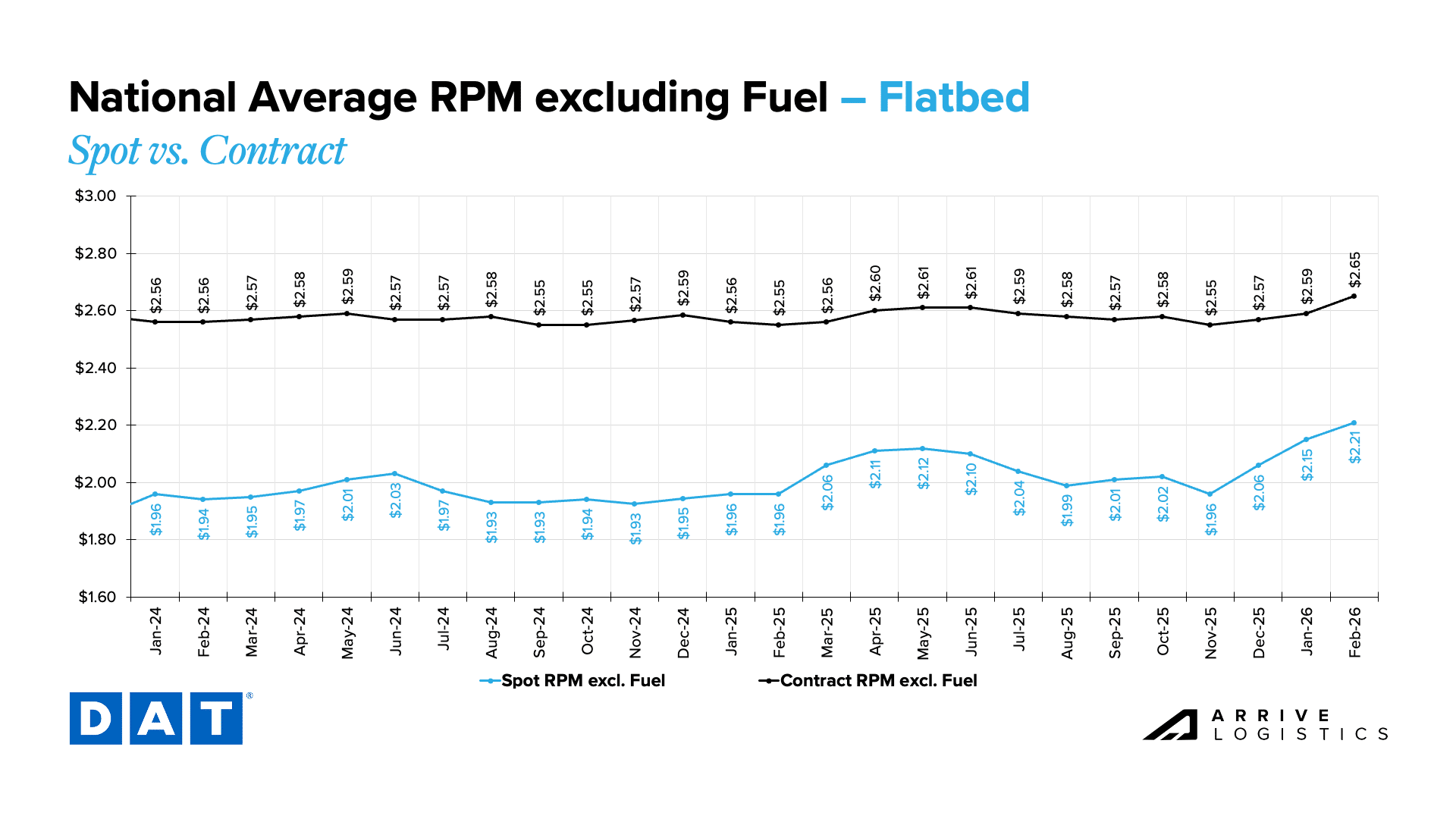

As of mid-month, spot rates across van, reefer and flatbed remain meaningfully elevated on a year-over-year basis, with some still sitting at or above contract levels. Even with volumes down year-over-year, supply is showing significant cracks as high operating costs, ongoing trucking employment declines and regulatory enforcement continue to reduce the driver count and shrink available capacity.

Looking ahead, spot rates will likely ease as the dust continues to settle in the coming weeks. However, even with a steeper-than-expected decline, they will enter the second quarter up significantly on a year-over-year basis. The longer spot rates remain elevated, the higher the floor for the year is set ahead of periods of increased seasonal demand.

In turn, pressure on contract rates will increase and routing guide challenges will become more common as the year progresses. This trend will likely first materialize when produce season ramps up in March, and how the market responds will offer insight into what to expect during the stretch from DOT Week in May through the peak summer shipping season in June and July.

If the last few months are any indication, shippers should prepare for some of the most volatile conditions in several years. While this is unlikely to match the scale of disruption seen during the pandemic, a sustained period of spot rate inflation should now be expected, along with the challenges that typically accompany those environments.

For more data and insights on the key trends to watch as this transition unfolds, read on.