Soft but stable demand is causing some tightness as produce season continues and DOT Week winds down. However, relatively calm economic conditions should help mitigate any major upside or downside movement beyond typical seasonal patterns.

Accepted contract volumes have been relatively strong in Q2 and are currently up year-over-year. Overall volumes are also up 1.0% month-over-month when adjusted for tender rejections, driven primarily by 6.8% reefer volume growth.

Figure 1: Contract Load Accepted Volume, SONAR

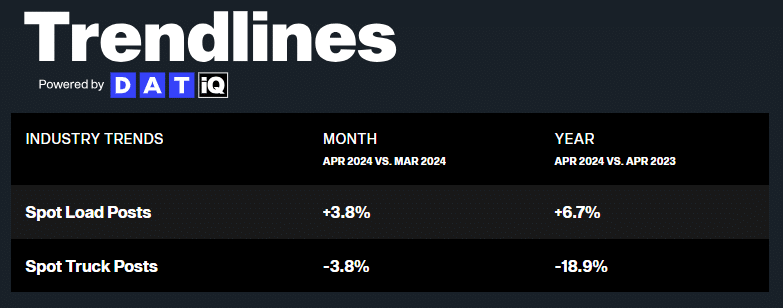

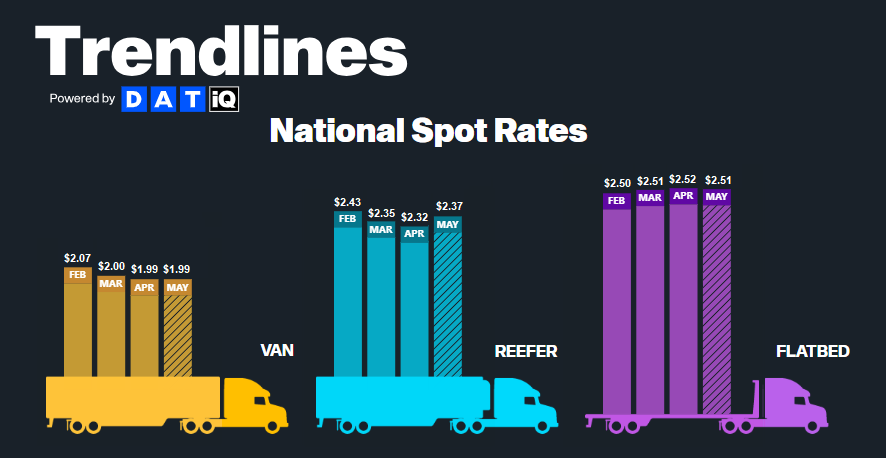

According to DAT, spot market activity ticked up month-over-month and year-over-year in April, indicating a slight demand increase compared to the same period last year. Truck postings declined by nearly 19% amid ongoing capacity attrition and strong contract tender compliance.

Figure 2: DAT Trendlines

Figure 2: DAT Trendlines

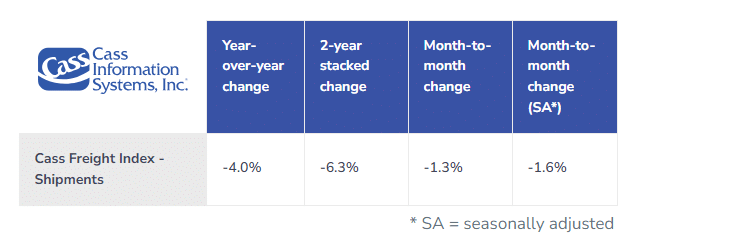

The Cass Freight Index shipments component is a good overall market health indicator because it encompasses both spot and contract freight based on bill data. The April reading showed a 1.3% month-over-month pullback (1.6% when accounting for seasonally adjusted terms) due to a soft for-hire market and volumes returning to cycle lows recorded in the second half of 2023.

Figure 3: Cass Freight Index Report – April 2024

Figure 3: Cass Freight Index Report – April 2024

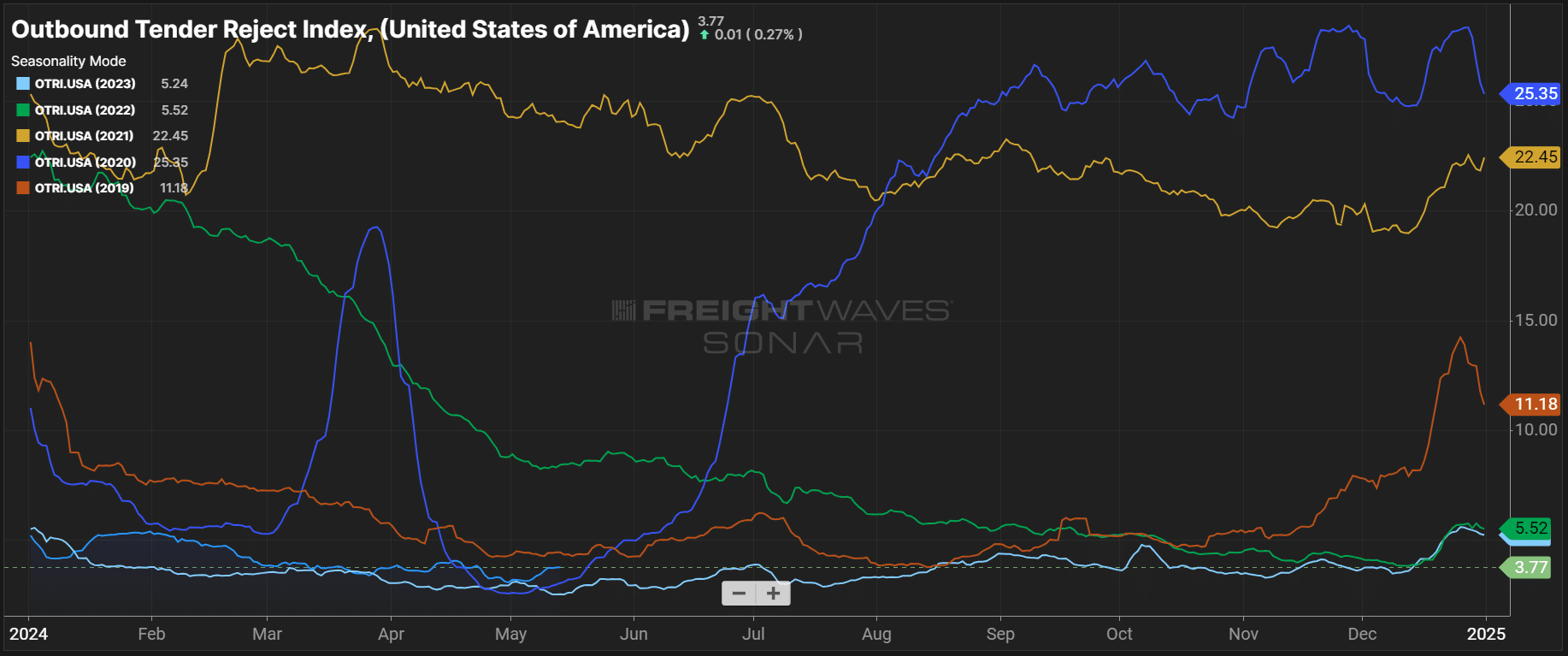

Though tracking total capacity is challenging, recent load-to-truck ratios and the April Outbound Tender Rejection Index reading indicate supply and demand are moving toward balance, leaving the market more vulnerable to seasonal pressures. Routing guides will see increased challenges due to the improved market balance but will remain intact overall and return to baseline after the Fourth of July.

The latest Sonar Outbound Tender Reject Index (OTRI), which measures the rate at which carriers reject freight they are contractually required to take, confirms that the market is more vulnerable to disruption than a year ago. Trends are approaching what they were in 2020, meaning DOT Week and summer peak season could have a greater impact. However, recent rejection rate growth is unlikely to last beyond peak season due to the oversupplied market.

Figure 4: Outbound Tender Reject Index, SONAR: OTRI starting to move similar to 2020 trends, indicating that the market is slightly more vulnerable to supply and demand disruptions.

Figure 4: Outbound Tender Reject Index, SONAR: OTRI starting to move similar to 2020 trends, indicating that the market is slightly more vulnerable to supply and demand disruptions.

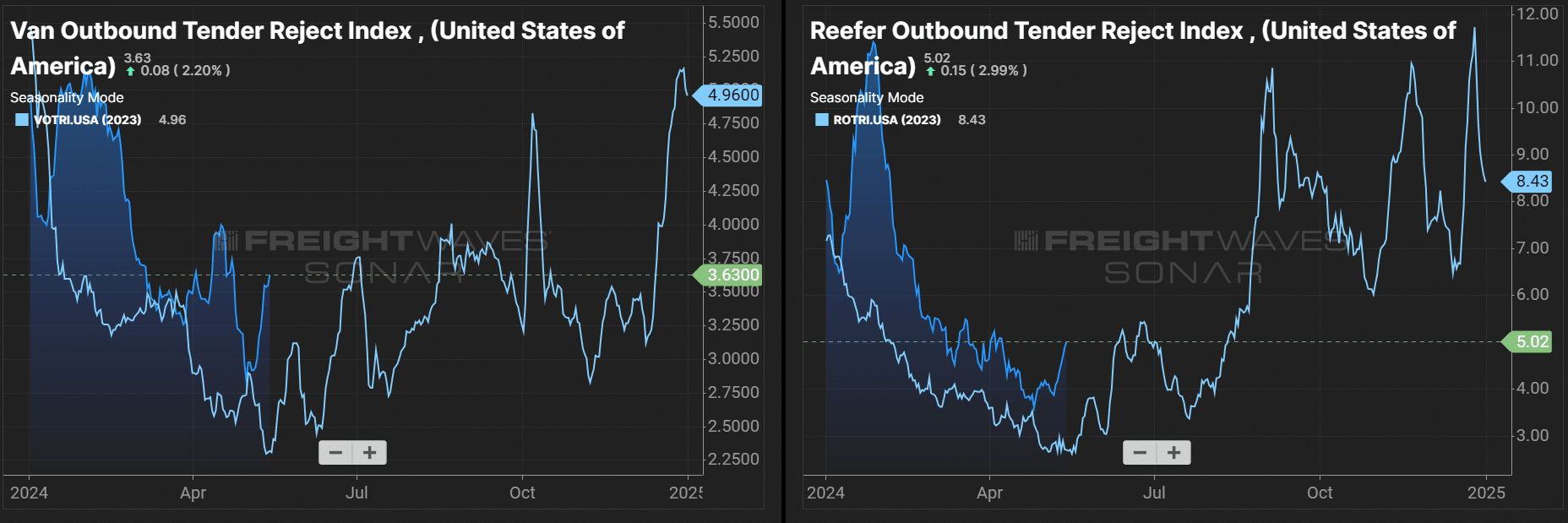

Figures 5 & 6: Van and Reefer Outbound Tender Reject Indices, SONAR: Dry van and reefer tender rejections were flat in March but have seen increases in early May.

Figures 5 & 6: Van and Reefer Outbound Tender Reject Indices, SONAR: Dry van and reefer tender rejections were flat in March but have seen increases in early May.

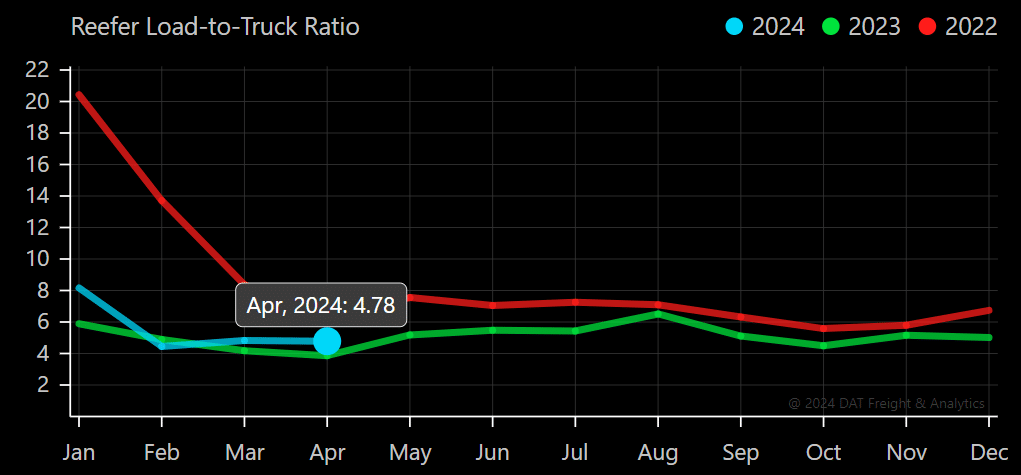

The DAT Load-to-Truck Ratio measures the total number of loads relative to the total number of trucks posted on its spot board. The April reading rose to 3.54 on the van side, slightly higher than April 2023 and in line with April 2022. Reefer load-to-truck ratios remained relatively flat month-over-month and slightly elevated year-over-year.

Figure 7: DAT Van Load-To-Truck Ratio

Figure 7: DAT Van Load-To-Truck Ratio

Figure 8: DAT Reefer Load-To-Truck Ratio

Figure 8: DAT Reefer Load-To-Truck Ratio

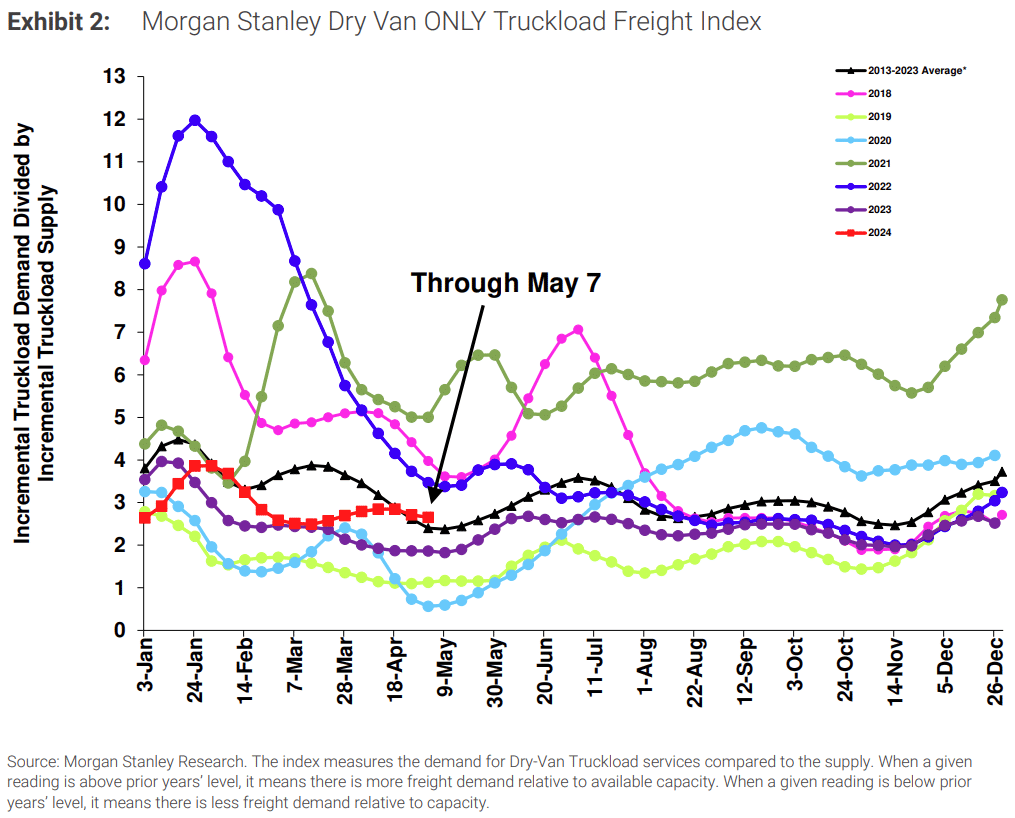

The Morgan Stanley Dry Van Freight Index is another measure of relative supply; the higher the index, the tighter the market conditions. The black line with triangle markers on the chart provides a great view of what directional trends would be in line with normal seasonality based on historical data dating back to 2007.

The most recent reading showed a small demand increase relative to supply in April. Though a slight deviation from seasonal expectations, this aligns with DAT spot posting data. As DOT Week concludes, the index remains in line with the historical averages for this time of year. Reefer data shows a similar deviation but is almost identical to 2023 from a year-over-year perspective.

Figure 9: Morgan Stanley Dry Van Truckload Freight Index

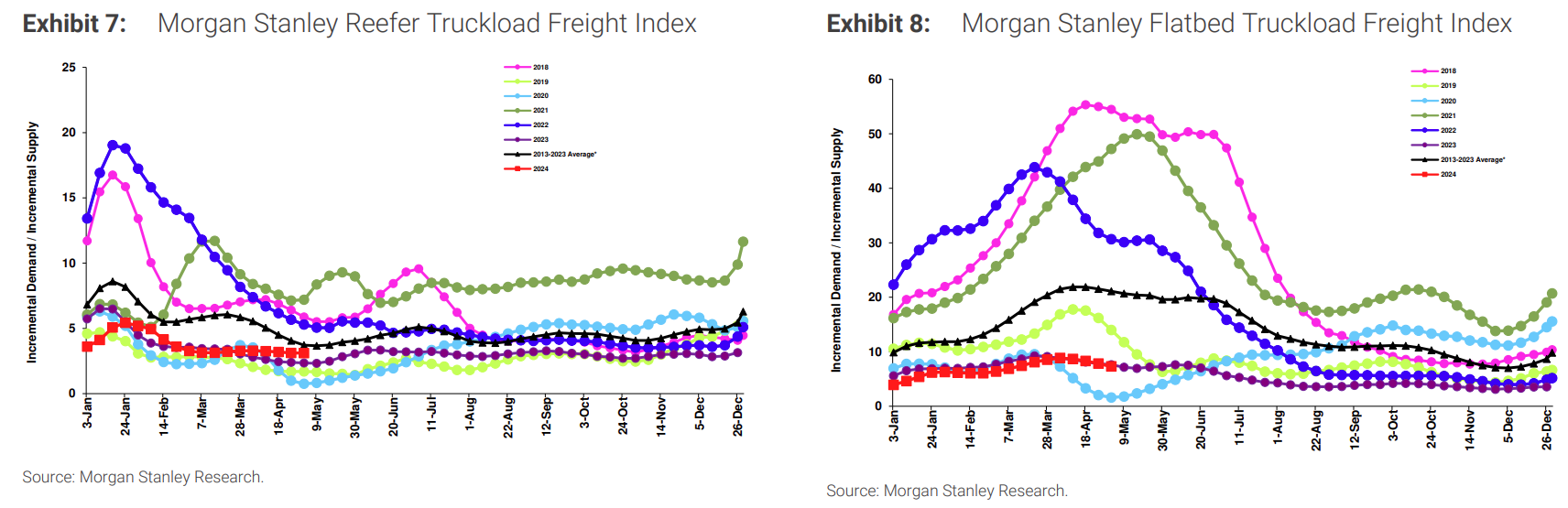

Figures 10 & 11: Morgan Stanley Reefer and Flatbed Truckload Freight Indices

DOT Week spurred regional rate volatility, particularly for reefer capacity. It is unclear how high rates will rise, but based on 2023 trends, we anticipate a return to normal seasonality by July rather than a sustained disruption.

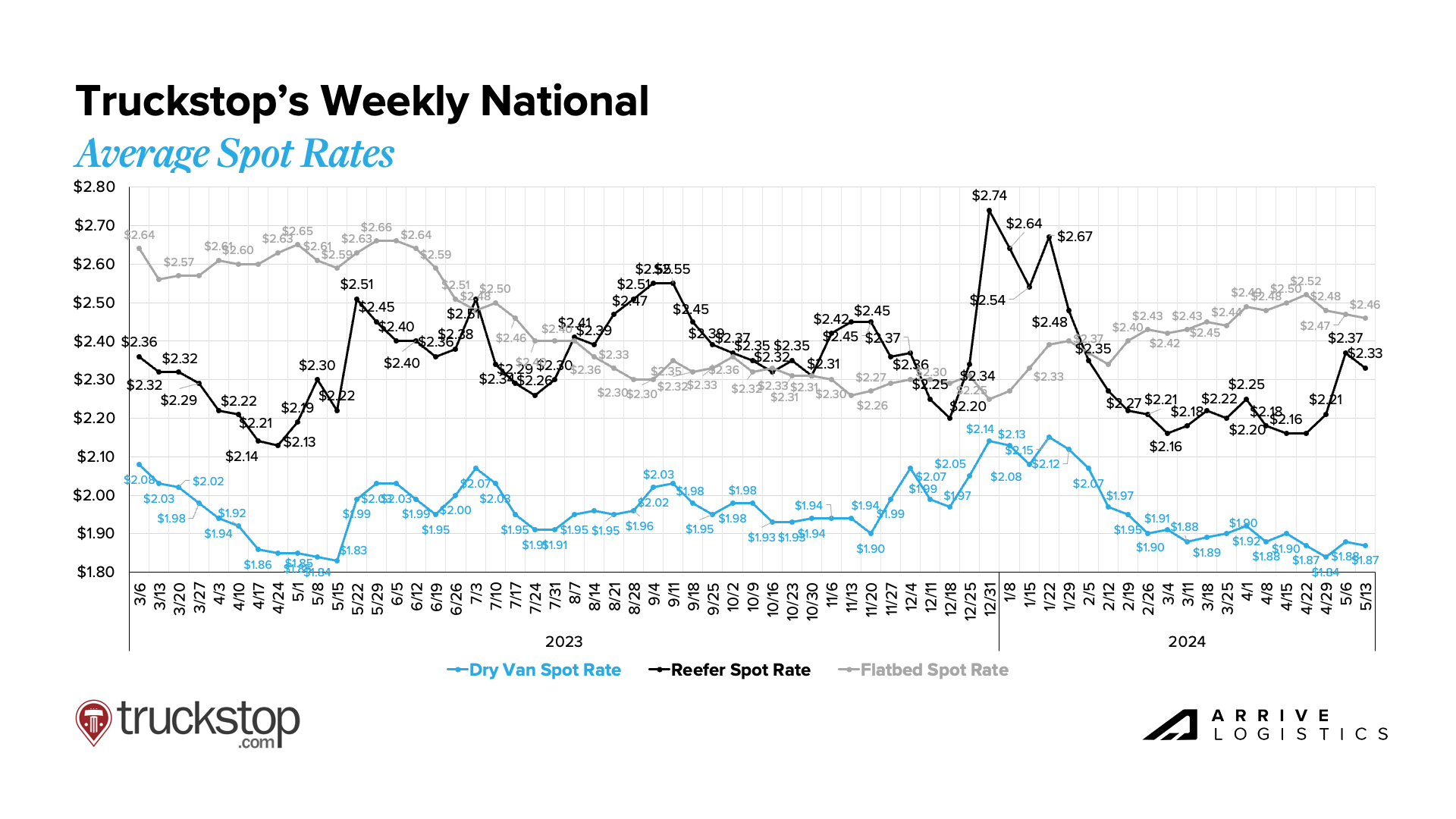

Truckstop’s Weekly National Average Spot Rates provide a detailed view of week-to-week movements and a real-time look into the current environment. Rates for all three equipment types are strikingly similar to this time last year, with van and reefer falling within just a few cents of 2023 levels. Given the year-over-year similarity of tender rejection and volume levels, rates will likely tick up this month, decline slightly in early June, and rise again around the Fourth of July and end of Q2. From there, rates should return to baseline levels as seasonal demand subsides.

Figure 12: Truckstop’s Weekly National Average Spot Rates

Figure 12: Truckstop’s Weekly National Average Spot Rates

With the produce season underway, reefer spot rates rose more sharply than any other mode in May. All-in dry van and flatbed rates did not increase to the same degree, but with fuel prices down $0.02 per mile and $0.03 per mile, respectively, linehaul rates are slightly higher.

Figure 13: DAT Monthly Rate Trends

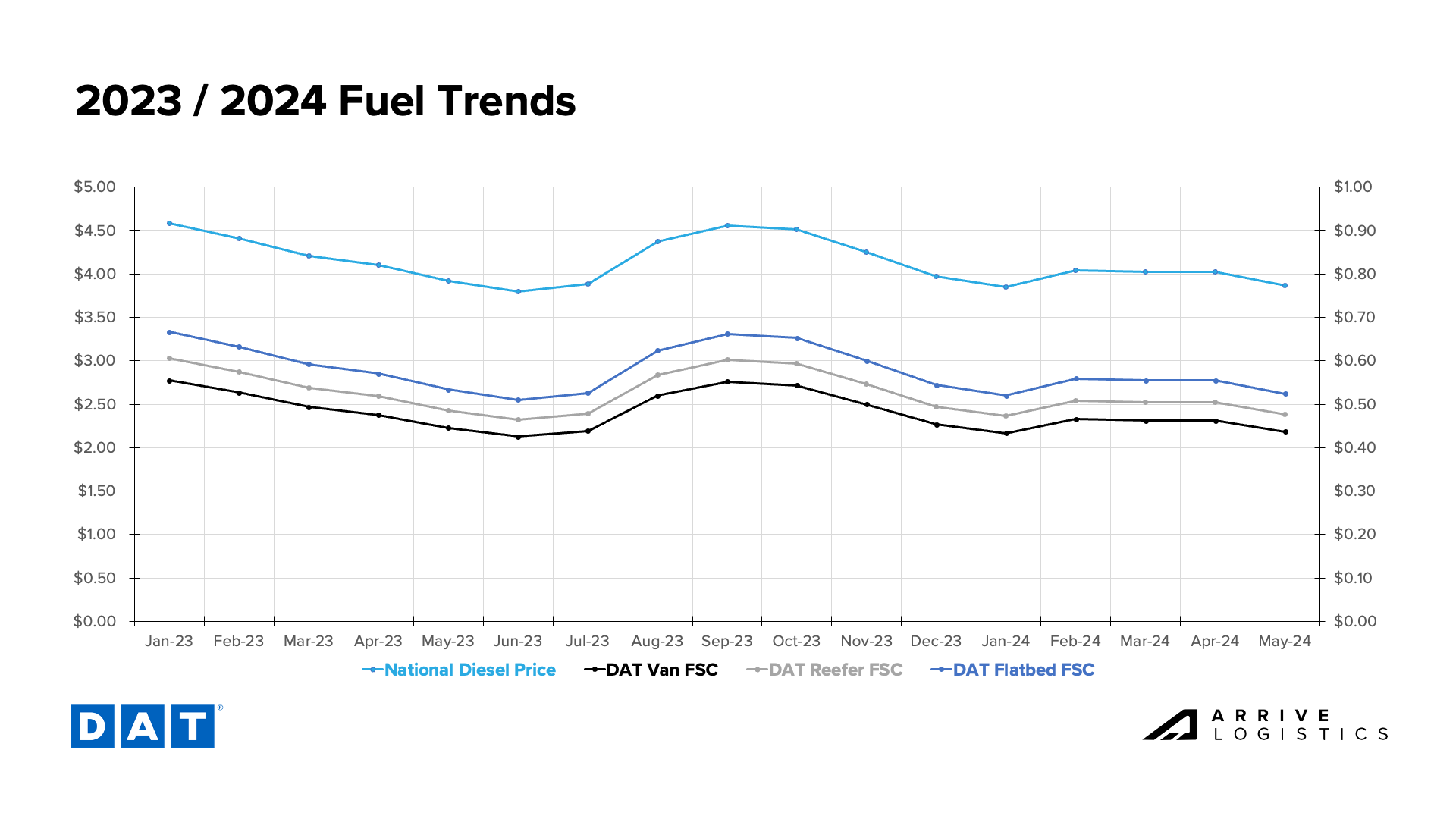

National diesel prices started to decline again in early May, with the average falling below $4.00 per gallon for the first time since January. Declining fuel costs benefit carriers facing financial pressure due to increased operating costs and low revenue. However, prices could increase again as summer demand ramps up and tensions in the Middle East escalate.

Figure 14: DAT Fuel Trends

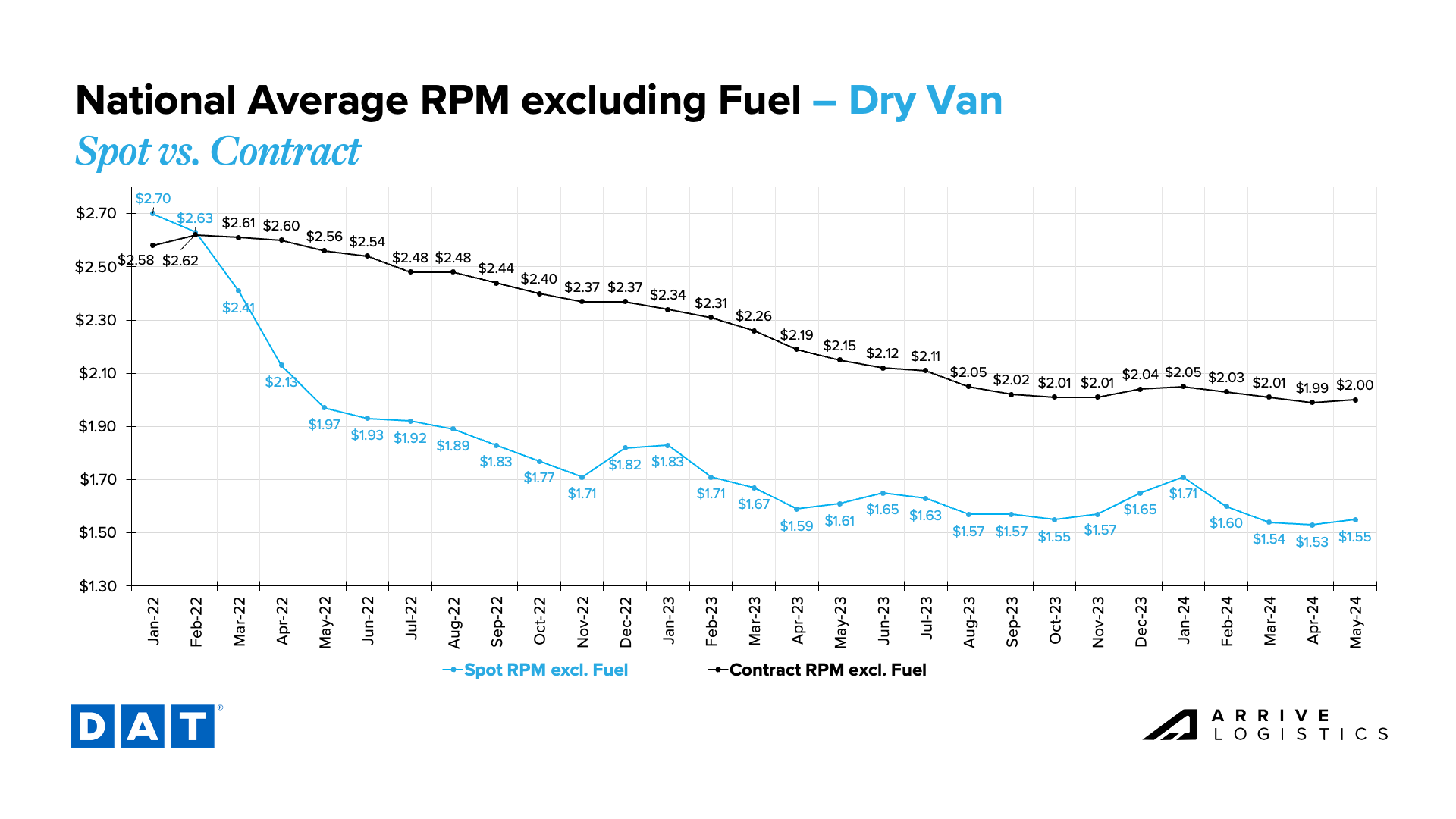

DAT data shows dry van spot rates increased by $0.02 to $1.55 per mile in May, excluding fuel. Contract rates also rose by $0.01 to $2.00 per mile. While national data shows minimal rate movement overall, there is still volatility on a lane-by-lane basis, such as on outbound freight in the Southeast. On the contrary, inbound Southeast rates have decreased as carriers look to capitalize on opportunities in the region.

Figure 15: DAT Dry Van National Average RPM Spot vs. Contract

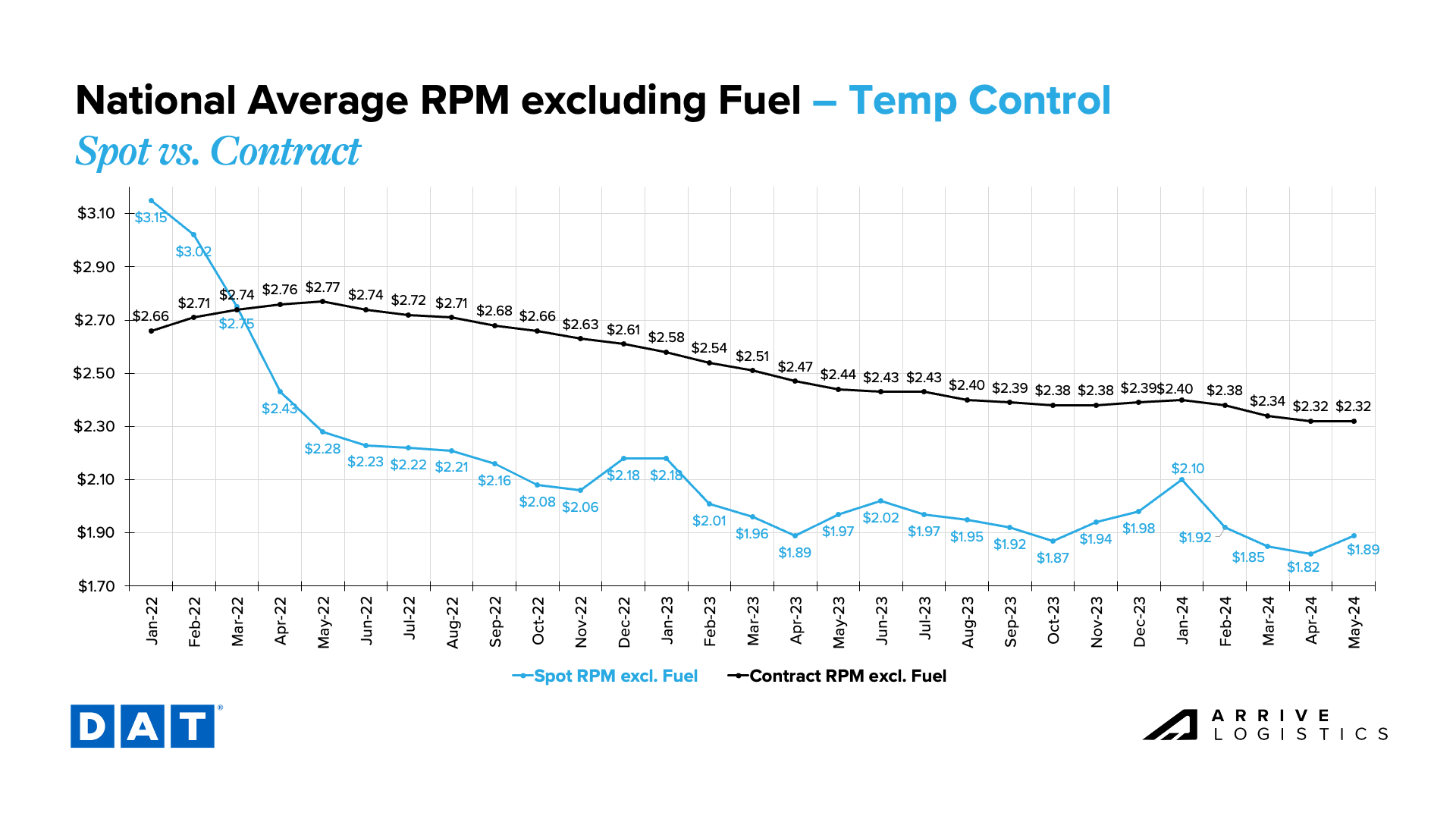

Reefer linehaul spot rates increased by $0.07 to $1.89 per mile in May, aligning with typical seasonal trends for this time of year. Contract rates were flat at $2.32 per mile, excluding fuel. Like dry van, some lanes were more volatile than others; rates out of California and other parts of the West Coast are rising, while inbound rates to the same region declined.

Figure 16: DAT Temp Control National Average RPM Spot vs. Contract

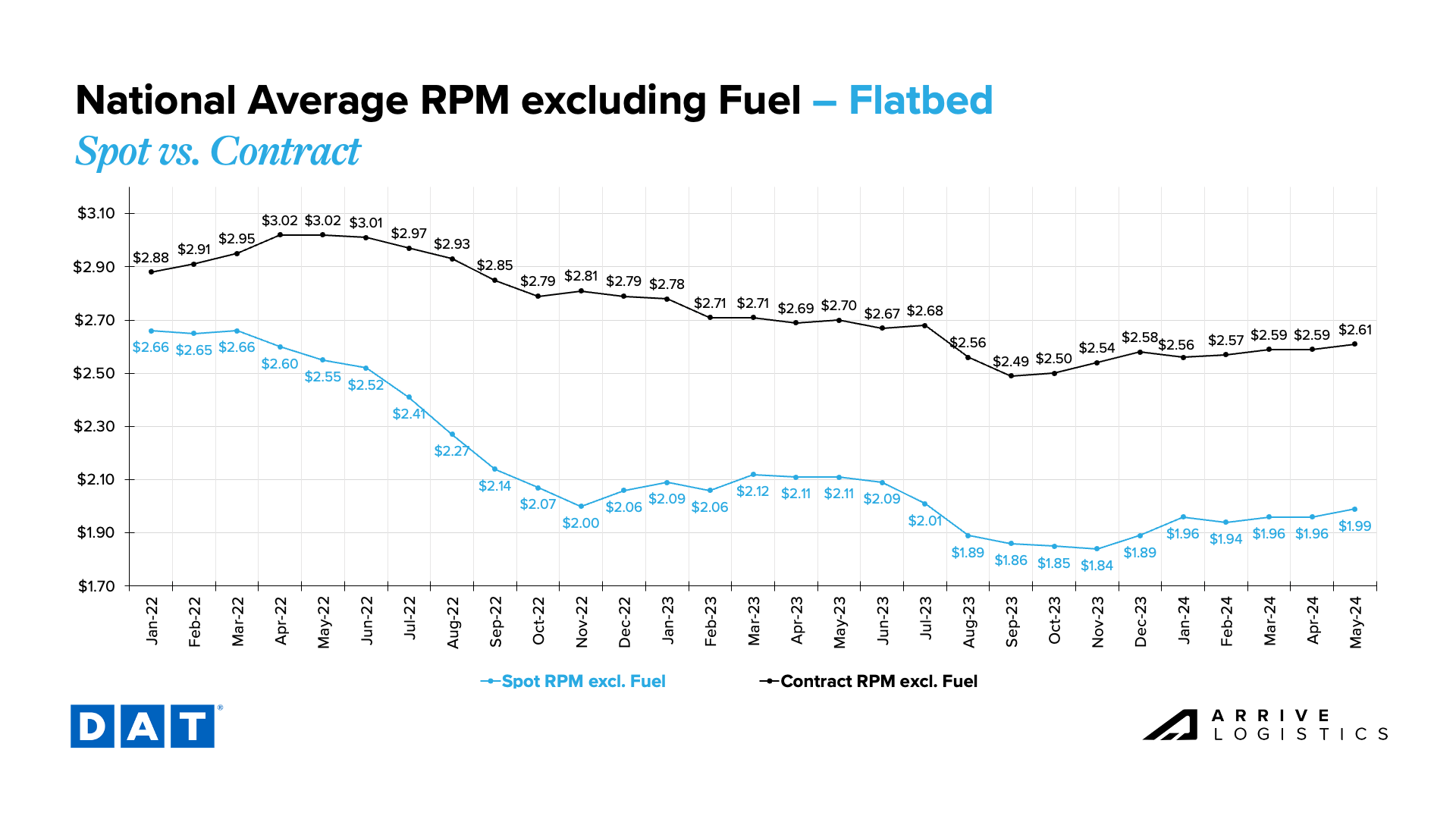

During the first half of May, flatbed spot and contract rates rose by $0.03 per mile and $0.02 per mile, respectively, driven by increased project-related freight demand for heavy equipment and commodities like steel. The gap between spot and contract rates remains large.

Figure 17: DAT Flatbed National Average RPM Spot vs. Contract

Figure 18: Inbound Ocean TEUs Volume Index, China to Mexico, SONAR

Figure 18: Inbound Ocean TEUs Volume Index, China to Mexico, SONAR

According to the latest revocations report, the for-hire carrier population has declined in 17 of 19 months. Though significant, the streak is still well short of The Great Recession, when the population fell in 28 of 30 months between October 2007 and March 2010. Despite the steady decline, there are 92,000 more active for-hire trucking firms today than before July 2020, when a massive wave of new carriers entered the market.

Figure 19: FTR’s Carrier Revocations, New Carriers & Net Change in Carrier Population

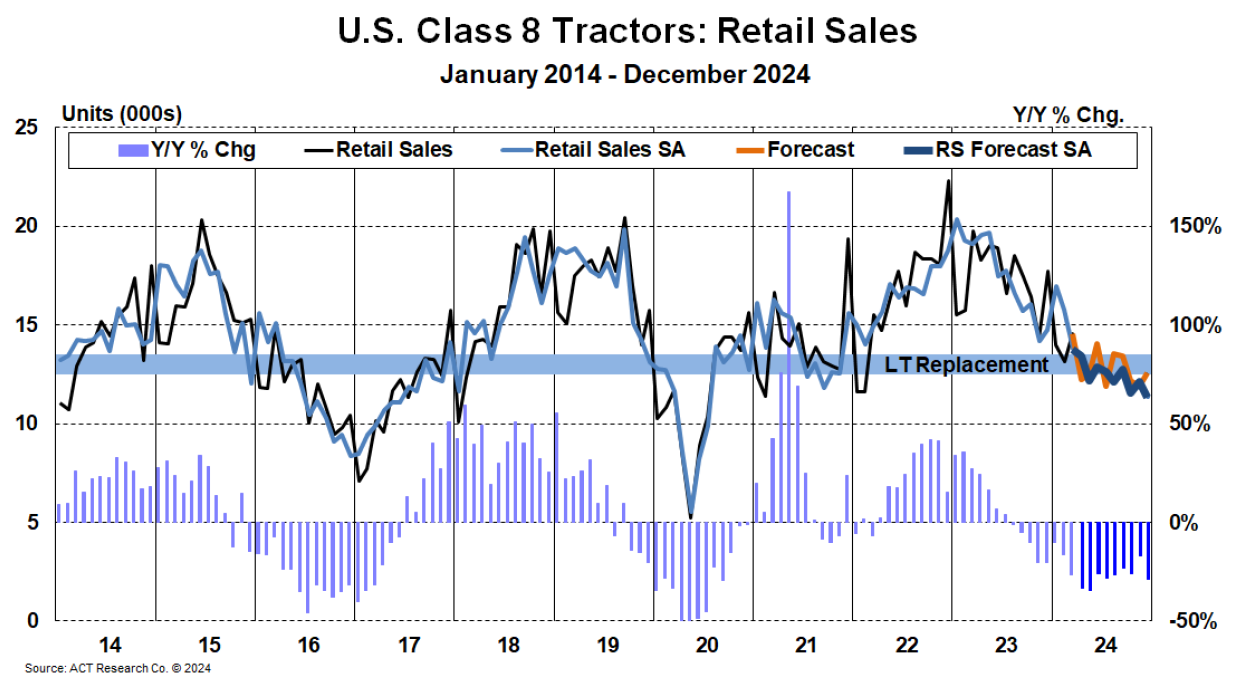

According to ACT Research, Class 8 Tractor sales have returned to replacement levels. While the for-hire market seems to have stopped adding to its fleets, private fleets continue to add equipment. However, increasing cost pressures and low revenues continue to strain carriers’ financial health, indicating that new tractor orders may continue to decline this year. Ultimately, this trend would create tightness and drive rates up.

Figure 20: Class 8 Orders vs. Spot Rates – ACT Research

Figure 20: Class 8 Orders vs. Spot Rates – ACT Research

FTR’s truck utilization forecast shows that utilization bottomed out during 2023 and will continue to increase in 2024. Capacity continues to exit the market, albeit slower than expected. As low revenues and high operating costs persist, the capacity exit rate could increase in the upcoming months.

Figure 21: Active Truck Utilization, FTR

Figure 21: Active Truck Utilization, FTR

The National Retail Federation (NRF)’s import outlook remains positive for the summer and fall, with over two million monthly TEUs forecasted. The most recent (March) import data showed U.S. ports handled around 1.93 million TEUs, down 1.4% from February but up 18.7% year-over-year.

While the large year-over-year increase is encouraging, it is important to note that Asian exports were slow in March 2023 due to the Lunar New Year. Nonetheless, the optimistic import forecast indicates retailers continue to order merchandise to meet strong consumer demand.

![]()

Figure 22: NRF Monthly Imports

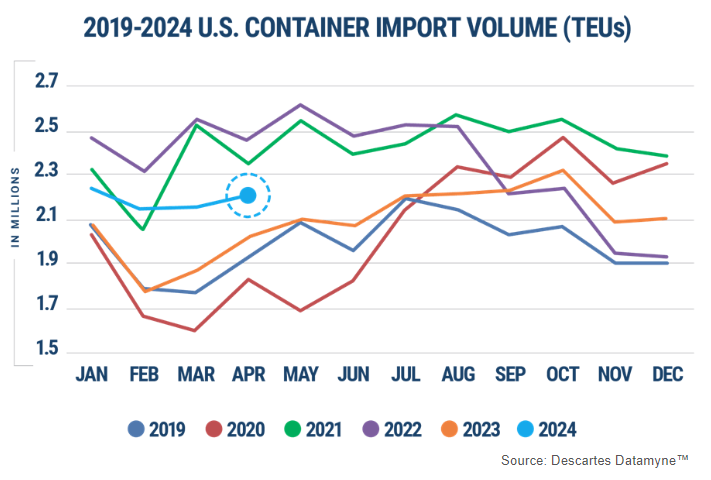

Aside from 2021 and 2022, April import levels have increased month-over-month every year since 2019. Additionally, April imports are 15% higher than before the pandemic, indicating continued economic growth. The percentage of total imports into the West Coast ports rose to 42.8% in April, while the percentage of total imports into the East and Gulf Coast ports fell to 43.9%. The top 10 ports had the largest month-over-month increase in over a year for the percentage of total freight, handling over 86% of total imports.

Figure 23: U.S. Container Import Volume 2019-2024, Descartes April 2024 Global Shipping Report

Figure 24: U.S. Container Import Volume, Descartes April 2024 Global Shipping Report

Figure 24: U.S. Container Import Volume, Descartes April 2024 Global Shipping Report

Consumer health remains strong overall. Industrial production increased by 0.4% month-over-month in March and was flat year-over-year. Manufacturing grew for the second consecutive month, increasing by 0.5% from February and by 1% year-over-year. While most indicators showed positive growth, housing starts declined by 14.7% month-over-month and 4.3% year-over-year.

Figure 25: Monthly Business & Economic Highlights, FTR

FTR’s latest truck loadings forecast calls for 0.3% year-over-year growth this year, down from 0.8% last month. The pullback comes on the heels of a revised flatbed growth forecast that now projects a 1.4% contraction compared to 2023. Dry van and reefer modes are expected to grow year-over-year by 1.7% and 2.5%, respectively.

Figure 26: Truck Loadings Summary, FTR

Figure 26: Truck Loadings Summary, FTR

April CPI data cooled to 3.4% from 3.5% in March, which may indicate interest rate cuts are still possible this year, but it is far from certain. Volatile energy costs like gasoline were the primary inflation drivers, while the cost of vehicles and some food items offset those increases. Housing inflation remained flat in April, which may concern policymakers who expected a better result.

Overall, the data is trending in the right direction. More positive readings could lead to interest rate cuts and drive freight demand. However, any near-term cuts are unlikely and could point to broader economic challenges. For now, the best-case scenario is sustained economic strength that allows for adjustment to higher interest rates and recovery in slow sectors.

Figure 27: New York Times Inflation Data

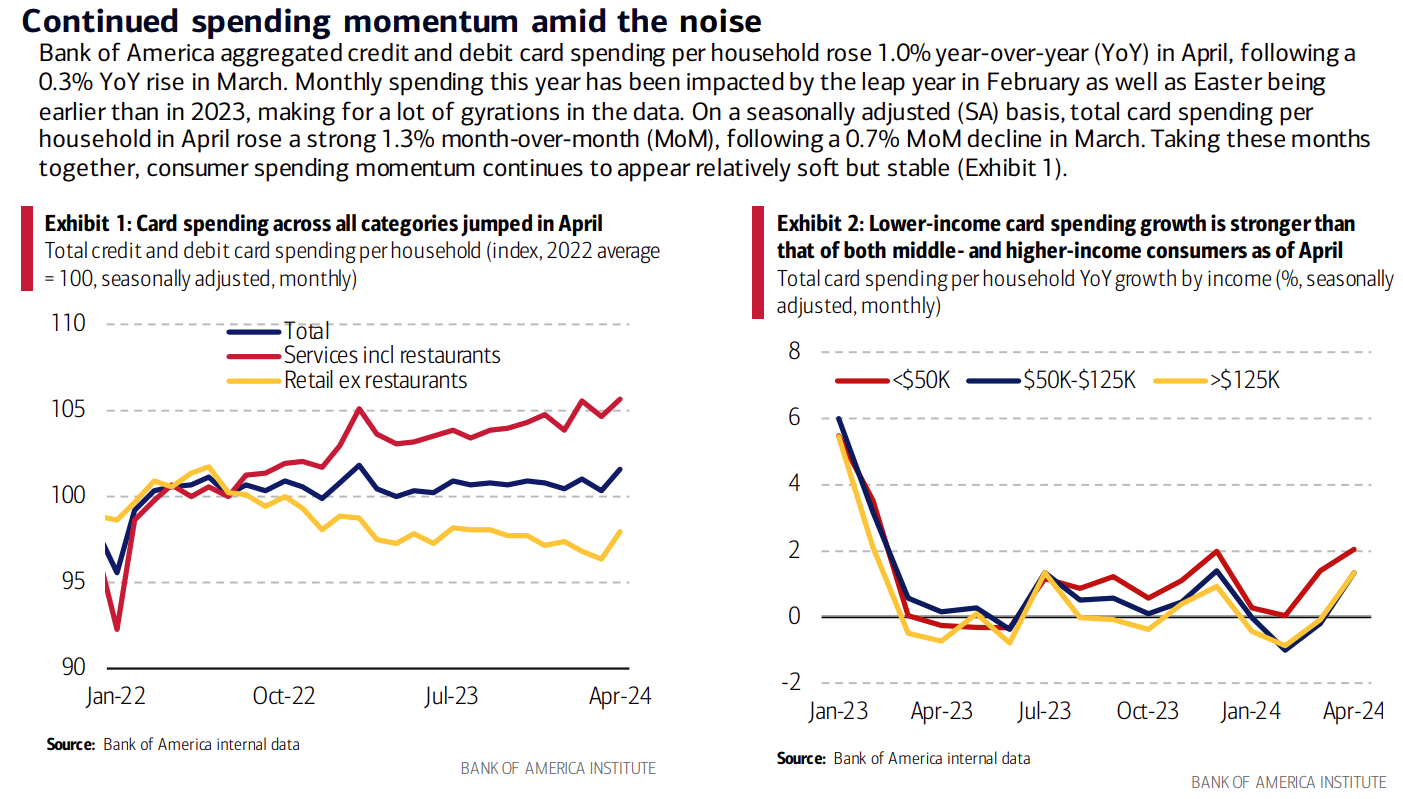

Bank of America card data showed a 1% year-over-year increase, with spending rising in the service and retail sectors, which should support a strong freight environment. Lower-income households’ after-tax wages and salaries increased, leading the growth rate to outpace middle and upper-tier income households. While encouraging, the cooling labor market could soon present new challenges, such as reduced spending on non-essential goods.

Figure 28: Bank of America Total Card Spending

Figure 28: Bank of America Total Card Spending