The mid-October demand narrative is slightly less optimistic than a month ago. At the time of this writing, available indices show a pullback in recent weeks; however, this is not uncommon during the transition from late September to early October.

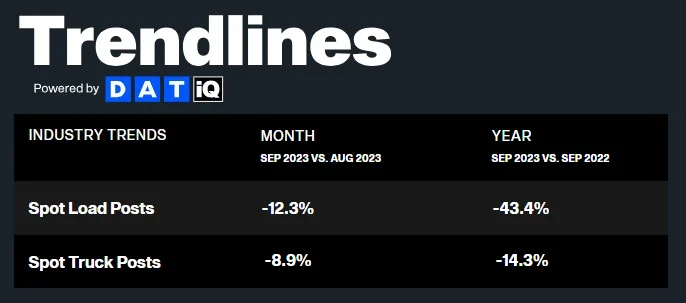

DAT reports exclusively on spot load trends and noted that posts were down 12.3% from August to September after increasing from July to August. The annual comps still showed a year-over-year decline, with spot load posts regressing slightly from -41.4% in August to -43.4% in September. Of additional note, spot load posts were down 15.7% from the last week of September to the first week of October, highlighting ongoing regression.

Figure 1: DAT Trendlines

Figure 1: DAT Trendlines

Cass reported September shipments decreased by 1.7%, which was the exact same when considering seasonal adjustment. The index remains down 6.3% year-over-year, an improvement from 10.6% in August but still a regression from the 4.7% year-over-year decline in June. Cass noted that signs are pointing to bottoming in the freight rate cycle and that ongoing carrier and OEM investment in and production of Class 8 equipment suggest a market shift may be further out on the horizon than expected.

Figure 2: Cass Freight Index

Figure 2: Cass Freight Index

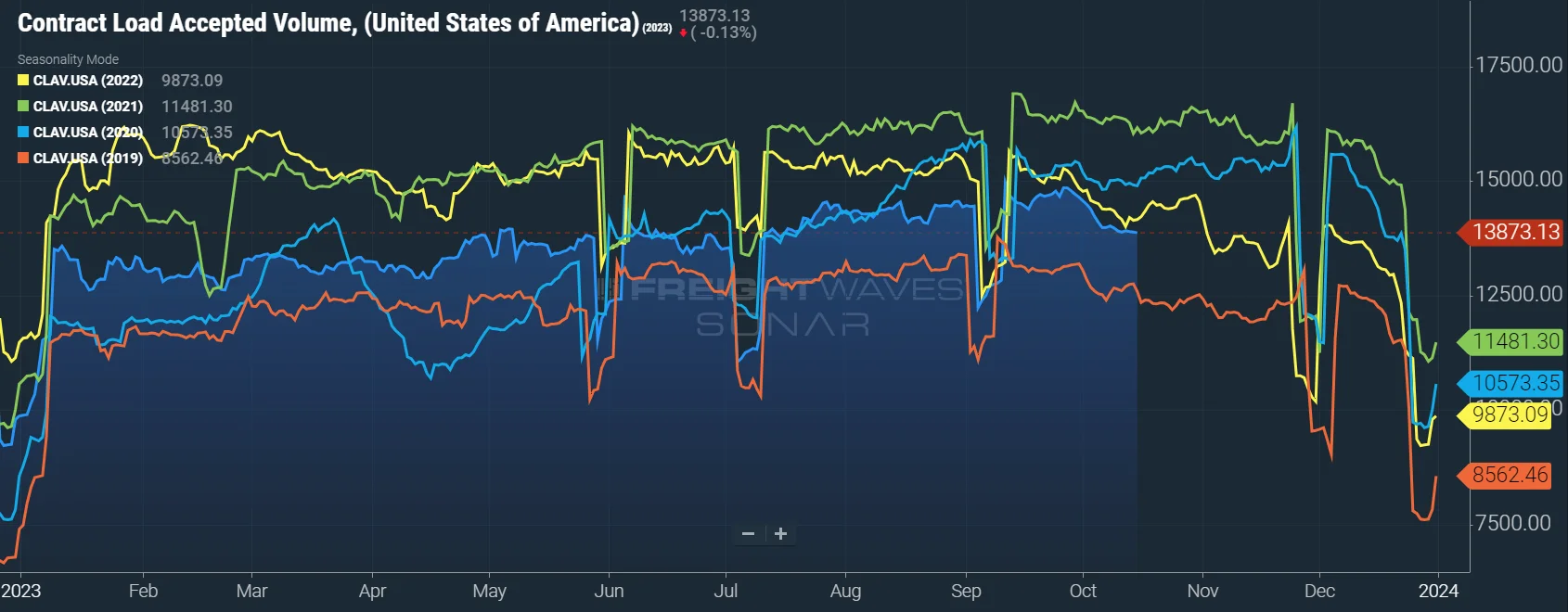

The FreightWaves SONAR Outbound Tender Volume Index (OTVI), which measures contract tender volumes across all modes, was down 3.1% year-over-year, or 1.4% when measuring accepted volumes after the significant tender rejection rate decline.

Accepted volumes were up 0.7% month-over-month as of October 1st, driven by a 4.9% increase in accepted dry van tenders and a 5.3% decrease in accepted reefer tenders. Contrary to the spot load declines reported in DAT’s data, it makes sense to see contract volumes remain relatively stable month-over-month. It is important to note that, similar to spot trends, accepted contract tender volumes have declined into mid-October, a sign that the contract trends are moving in line with the spot market.

Figure 3: Contract Load Accepted Volume, SONAR: Accepted contract volumes were down 1.4% y/y in early October but remained above historical pre-pandemic levels.

Figure 3: Contract Load Accepted Volume, SONAR: Accepted contract volumes were down 1.4% y/y in early October but remained above historical pre-pandemic levels.

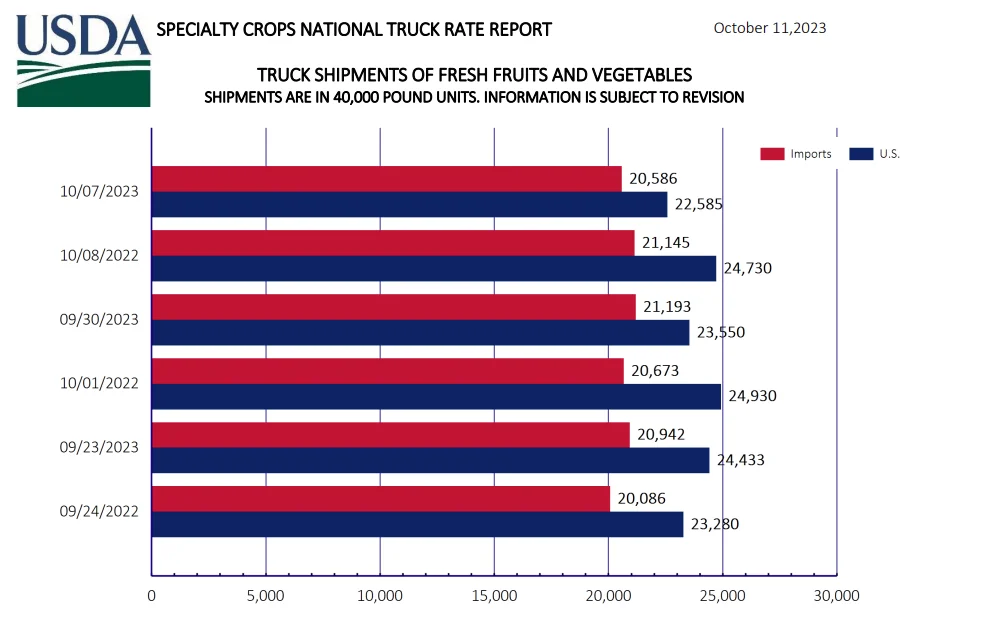

Like the reefer tender volume trends reported by FreightWaves, USDA truck shipment data for fresh fruits and vegetables showed pullbacks in total truck shipments and the year-over-year growth rate from a month ago. In mid-September, the three-week trend showed total shipments were down 3% year-over-year, with U.S.-grown shipments down 5% and imported crop shipments flat. In mid-October, the three-week trend shows total shipments are down just 1% year-over-year, with U.S.-grown shipments down 3% and imports up 1%.

Figure 4: USDA Specialty Crops National Truck Rate Report

Figure 4: USDA Specialty Crops National Truck Rate Report

As the lull between the summer peak season and Q4 peak retail season continues, it remains clear that capacity is largely sufficient to meet current demand. Seasonal demand surges lead to regional pockets of rate volatility throughout the summer, and this trend will likely continue through this quarter.

At a national level, conditions have eased following the consecutive impacts of Hurricane Idalia and Labor Day, though they are still not as soft as earlier in the year. This is especially true for reefer equipment, which is currently seeing tender rejections at nearly double the rate of van equipment.

The Sonar Outbound Tender Reject Index (OTRI) measures the rate at which carriers reject the freight they are contractually required to take. The numbers fluctuated between a high of 4.38% on the first day of the month and a low of 3.65% by month-end, indicating routing guide compliance on shippers’ contractual freight continually improved from already historically high levels.

Figure 5: Outbound Tender Reject Index, SONAR: OTRI remains below 4% and 2019 levels — a sign capacity is still sufficient to support demand and carriers are protecting their contract freight despite increases in spot.

Figure 5: Outbound Tender Reject Index, SONAR: OTRI remains below 4% and 2019 levels — a sign capacity is still sufficient to support demand and carriers are protecting their contract freight despite increases in spot.

Tender rejections followed a similar pattern for reefer equipment but spiked as high as 10.9% in early September and finished the month at about 8.5%. With a current value of 7.28%, it is clear that the early Q4 lull is affecting reefer equipment.

As stated a month ago, we agree with those forecasting a muted peak season as Q4 begins; however, the reefer environment could become more challenging as we approach Thanksgiving and Christmas.

Figures 6 & 7: Van and Reefer Outbound Tender Reject Indices, SONAR: Dry van rejections remain historically low, but a meaningful increase in the baseline for reefer tender rejections is a sign that the market is becoming more vulnerable for the equipment type.

Figures 6 & 7: Van and Reefer Outbound Tender Reject Indices, SONAR: Dry van rejections remain historically low, but a meaningful increase in the baseline for reefer tender rejections is a sign that the market is becoming more vulnerable for the equipment type.

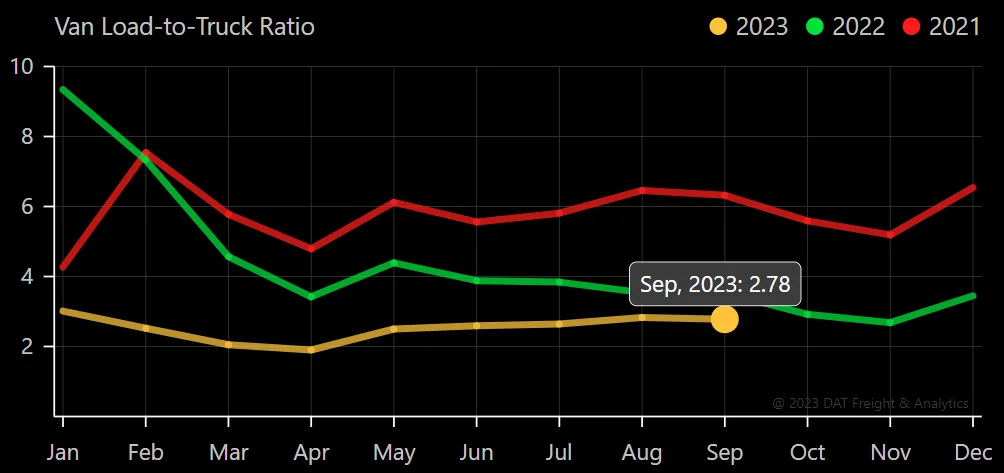

The DAT Load-to-Truck Ratio measures the total number of loads relative to the total number of trucks posted on their spot board. Despite a meaningful spot load decrease, September data showed relatively flat conditions, indicating truck posts were also down.

The Dry Van Load-to-Truck Ratio was down 1.7% month-over-month and remains down 21% year-over-year, whereas the Reefer Load-to-Truck Ratio was down 22% month-over-month and 45.8% year-over-year. This may seem like a divergence from reefer contract rejection trends, but overall, easing rejections means less spot demand. So, even though reefer rejections were higher, the fact that they were dropping throughout the month is the likely culprit of declining reefer load-to-truck ratios.

Figure 8: DAT Van Load-To-Truck Ratio

Figure 8: DAT Van Load-To-Truck Ratio

Figure 9: DAT Reefer Load-To-Truck Ratio

Figure 9: DAT Reefer Load-To-Truck Ratio

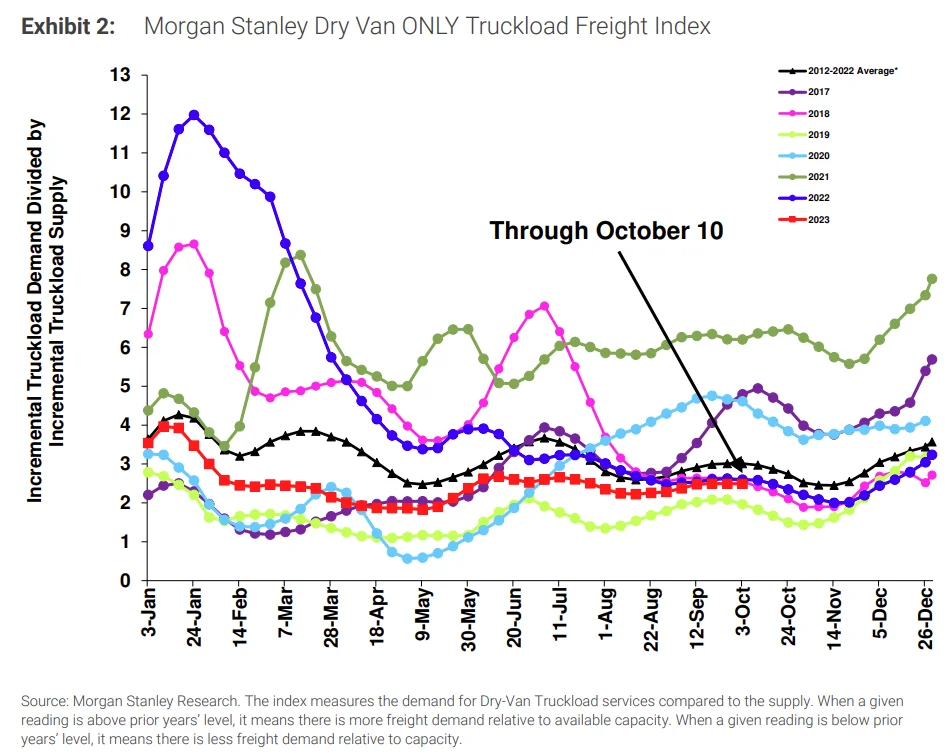

The Morgan Stanley Dry Van Freight Index is another measure of relative supply; the higher the index, the tighter the market conditions. The black line with triangle markers on the chart provides a great view of what directional trends would be in line with normal seasonality based on historical data dating back to 2007.

Conditions were relatively stable throughout September, underperforming historical seasonality and indicating supply is still largely sufficient to support demand. Historical data points to potential easing conditions through Thanksgiving before tightening through the end of the year.

Figure 10: Morgan Stanley Dry Van Truckload Freight Index

Figure 10: Morgan Stanley Dry Van Truckload Freight Index

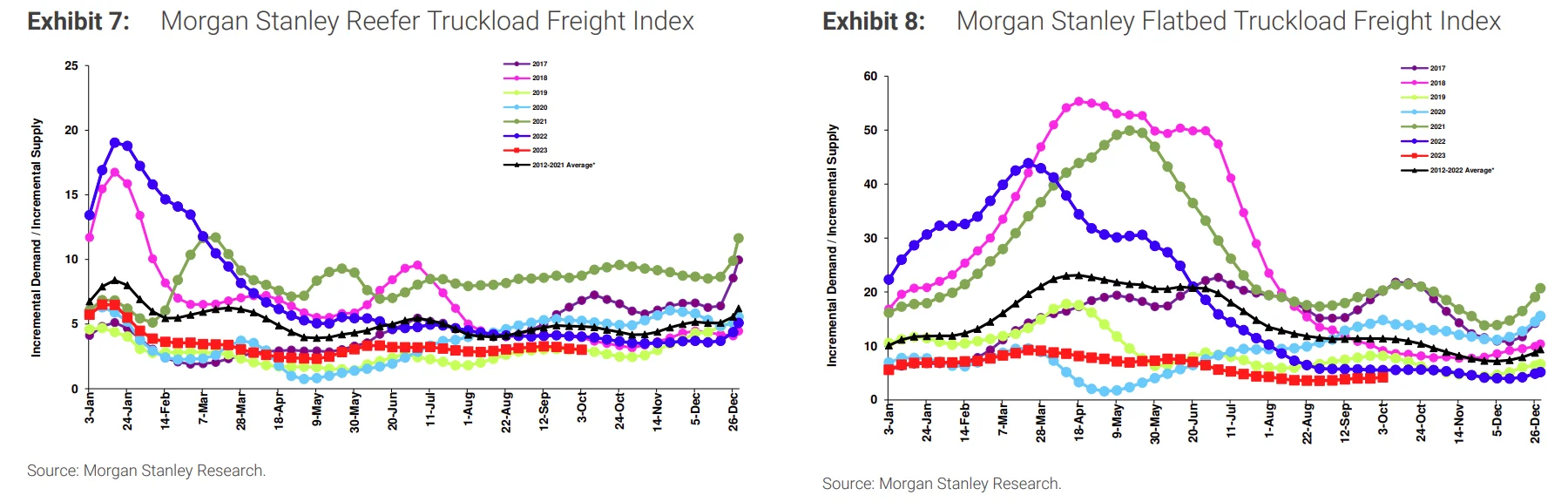

Figures 11 & 12: Morgan Stanley Reefer and Flatbed Truckload Freight Indices

Figures 11 & 12: Morgan Stanley Reefer and Flatbed Truckload Freight Indices

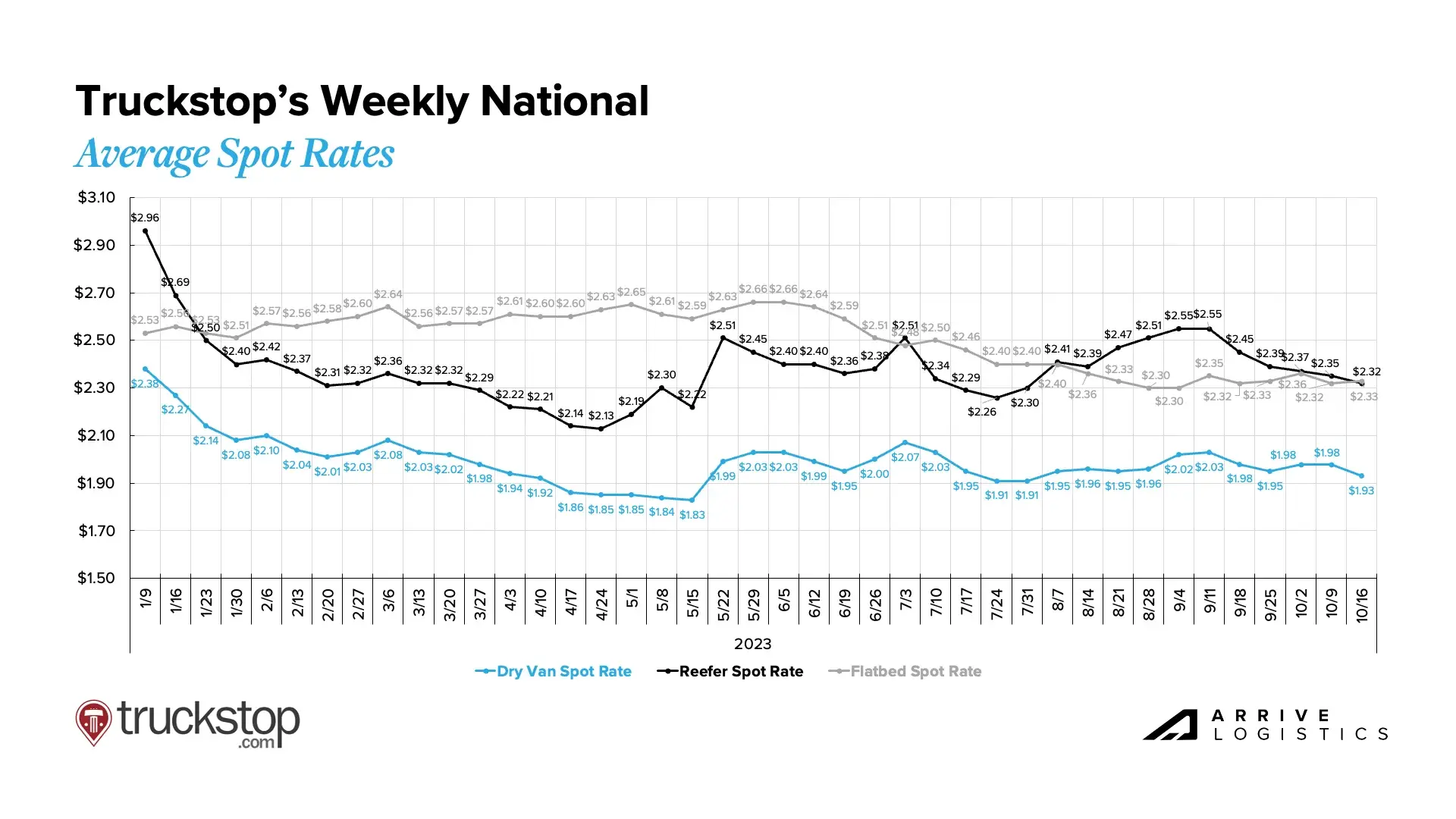

Truckstop’s Weekly National Average Spot Rates provide a detailed view of week-to-week rate movements and a real-time look into the current rate environment.

Following tender rejection trends, rates for van and reefer equipment are showing signs of easing early in Q4, while flatbed rates appear to have found a floor. Soft market conditions should continue for all three equipment types through at least mid-November when peak retail seasonality begins.

Figure 13: Truckstop Weekly National Average Spot Rates

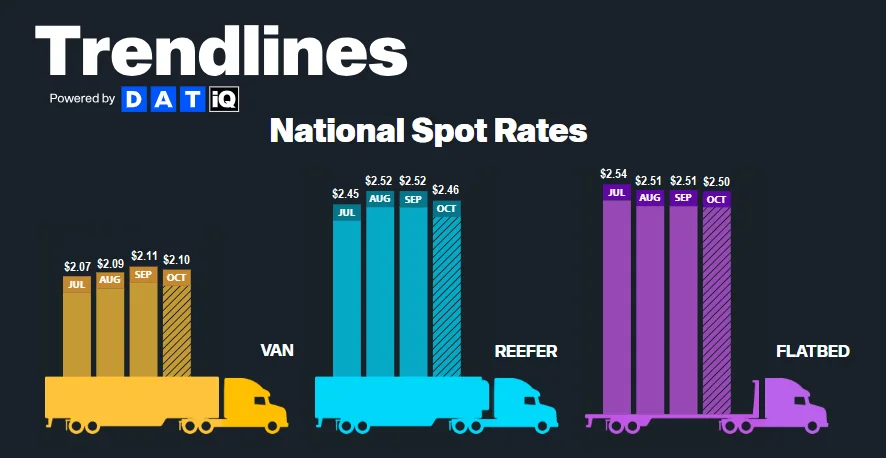

According to DAT, all-in spot rates, including linehaul and fuel costs, are down slightly for all three equipment types month-over-month. Since September, van and flatbed rates are down $0.01 per mile, and reefer rates are down $0.06 per mile.

Relatively stable fuel surcharges month-over-month mean that linehaul rates moved closely in line with all-in rates. That could change as the war in the Middle East threatens to disrupt oil markets.

Figure 14: DAT Trendlines National Spot Rates

Figure 14: DAT Trendlines National Spot Rates

The month-over-month van rate spread increased slightly from $0.48 in September to $0.50 month-to-date in October.

All-in dry van spot rates are down 13.6% year-over-year in October, while linehaul spot rates are down 11.9%, the lowest negative growth rate since April 2022. All-in dry van contract rates are down 15.0% year-over-year, and linehaul contract rates are down 14.2%. These improvements continue to illustrate that peak deflationary pressures are behind us.

Figure 15: DAT Dry Van National Average RPM Spot vs. Contract

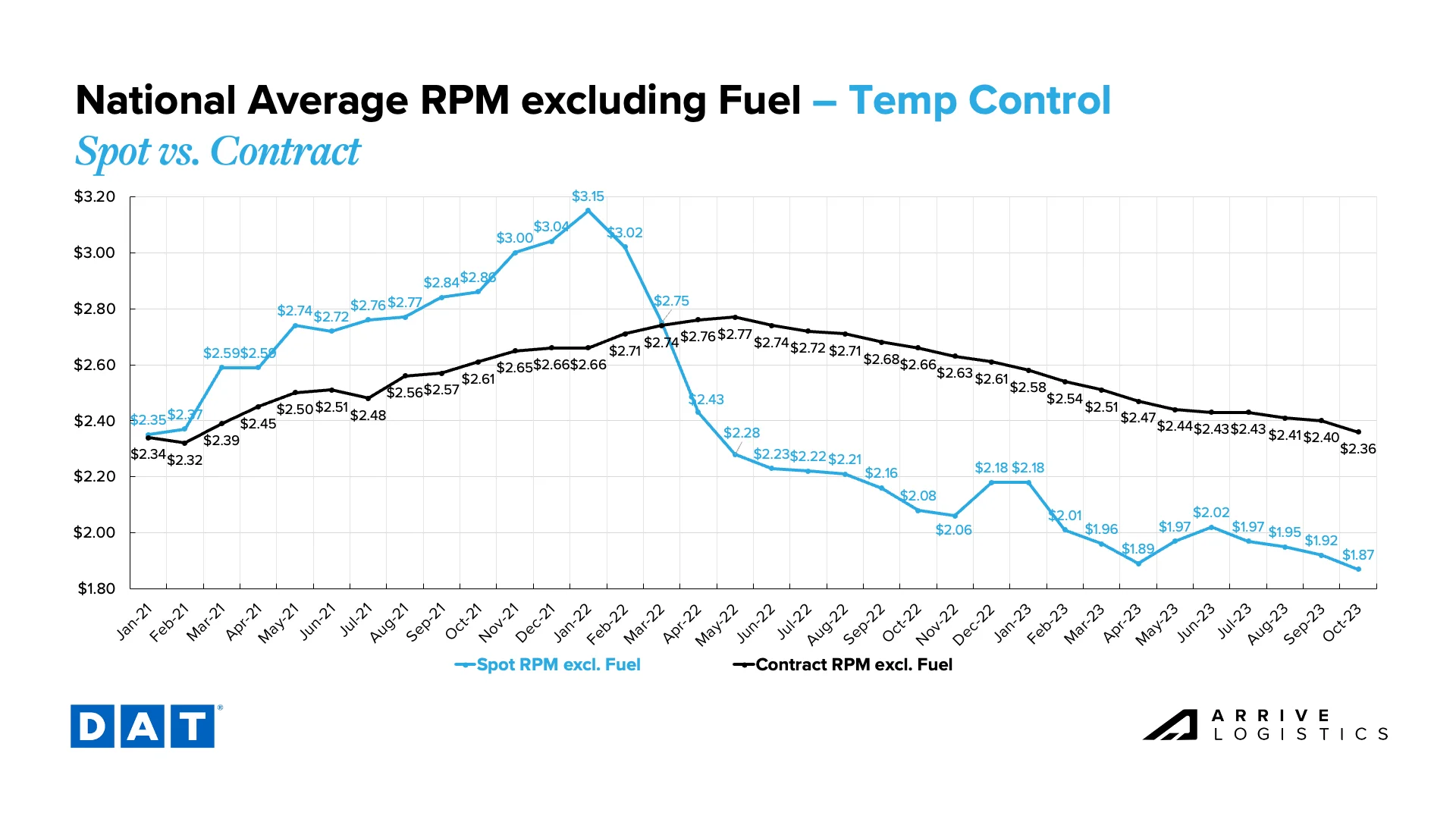

Monthly reefer rates fell for the fourth consecutive month, pointing to a new floor for spot rates early in October. This is a little misleading when considering the weekly rate trends, however, it still indicates that the market is in a lull typical for this time of year.

After hitting an April high of $0.58, the reefer spot-contract rate spread dipped as low as $0.41 when spot rates peaked in June but is back up to $0.49 in early October. Reefer spot rates will likely find a floor relatively quickly, enabling the gap between spot and contract rates to close again as contract rates continue to undergo downward pressure.

The current reefer contract rate is down 11.3% year-over-year to $2.36 per mile, excluding fuel, while the current reefer spot rate is down 10.1% year-over-year to $1.87 per mile, excluding fuel.

Figure 16: DAT Temp Control National Average RPM Spot vs. Contract

Figure 16: DAT Temp Control National Average RPM Spot vs. Contract

After stabilizing in the first half of 2023, flatbed rates declined rapidly from June through August and have since found a new floor. Contract rates fell at a similar rate, keeping the spot-contract gap near an all-time high of $0.66 per mile after dipping to a cycle low of $0.58 in April. In October, spot rates are currently $1.85 and contract at $2.51 per mile, excluding fuel.

Figure 17: DAT Flatbed National Average RPM Spot vs. Contract

Figure 17: DAT Flatbed National Average RPM Spot vs. Contract

Declining spot rates in early Q4 are a harsh reminder to carriers with high spot exposure that they won’t see significant market improvements for some time. Easing fuel costs are providing some relief, but risks for further fuel price volatility remain high. Although we have not yet seen revocations of operating authorities accelerate as result, we expect the lagging impact will set in later this year or early next.

Larger carriers and those running on a majority contractual basis can still operate at mostly profitable rates. They are also less vulnerable to fuel price fluctuations since contract rates are typically negotiated with a variable fuel component.

The fact that some carriers are profitable while many others are struggling makes this market cycle unique. It also makes revocation and employment data difficult to interpret due to larger asset carriers and private fleets continuing to expand their operations. That said, revocation and employment trends represent broader industry momentum swings and show an indisputable shift in where opportunity exists today.

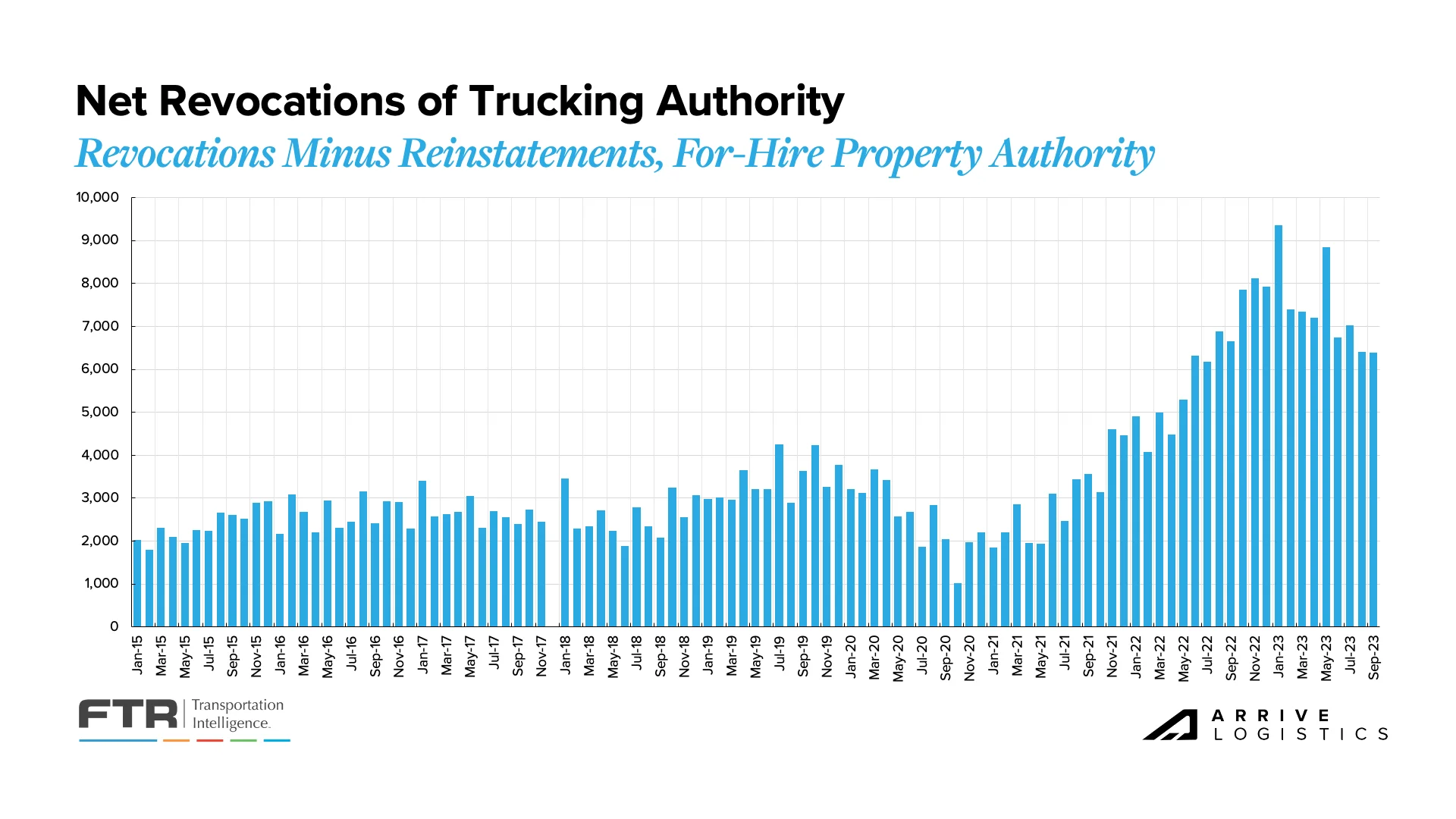

Monthly revocations continue to ease from this year’s peaks but remain highly elevated compared to historical norms. This month, significant revocations again led to a negative net change in the carrier population. Strong contract service numbers indicate the correction is far from over, but this trend will inevitably lead to a capacity crunch, as it always does in the market cycle.

Increased operating expenses are the primary culprit causing carriers to close, as overall rates are still high compared to historical (pre-pandemic) levels. This trend continues to drive record-high revocations of authority, although October totals were the lowest in more than a year at just under 6,400 carriers.

Figure 18: Net Revocations of Trucking Authority: FTR Analysis of FMCSA Data

Figure 18: Net Revocations of Trucking Authority: FTR Analysis of FMCSA Data

A key trend we’re still watching is revocations outpacing new carriers entering the market for 11 of the last 12 months, reducing the total number of carriers. A significant amount of capacity that entered the market over the last few years remains under-utilized, so we expect this disparity to continue for at least the near term.

Figure 19: Net Change in Carrier Population: FTR Analysis of FMCSA Data

Figure 19: Net Change in Carrier Population: FTR Analysis of FMCSA Data

New equipment orders typically slow during freight recessions, making the recent spike more intriguing. As OEM’s opened up 2024 build slots, carriers moved quickly to secure new orders. This likely points to the financial strength of larger carriers and private fleets’ ongoing investment in growth. It also represents the possibility of a much slower capacity reduction than in previous cycles. Overall, freight demand is healthy, so larger fleets are adding capacity to insource volume back from smaller for-hire fleets and owner-operators.

Figure 20: New Truck Order, Class 8: FTR Analysis of FMCSA Data

Figure 20: New Truck Order, Class 8: FTR Analysis of FMCSA Data

Although recent October truckload demand data is discouraging, an early Q4 lull is not unusual. The broader trend shows seasonally adjusted tonnage growth since earlier in the year. This is largely due to consumer spending enabling retailers to shift from destocking to normal ordering patterns as the inventory cycle resets.

Downside demand risks remain, including concerns about manufacturing trends, how long strong consumer spending will continue, the potential impact of student loan payment resumption on 2024 housing and construction, and the possibility of an extended period of elevated interest rates.

The National Retail Federation (NRF) recently reported that while the consumer remains strong, spending growth underperformed expectations and may worsen. In turn, low retail import volumes will likely last through year-end.

Consumer behavior through this year’s peak retail season should be a strong indicator of retail import volumes in 2024. NRF Vice President Jonathan Gold said, “Cargo volumes will still be strong the rest of the year, but not as high as we expected a month ago.” This means we are unlikely to see any surprises during peak season.

If import volumes trend as expected through Q4, the 13.5% year-over-year decline in July could flip to a nearly 9% increase in year-over-year import growth by December. This gives some context to how the inventory cycle’s reset could impact demand and just how large a step back retailers took a year ago to correct their overstocked inventories.

![]()

Figure 21: NRF Monthly Imports

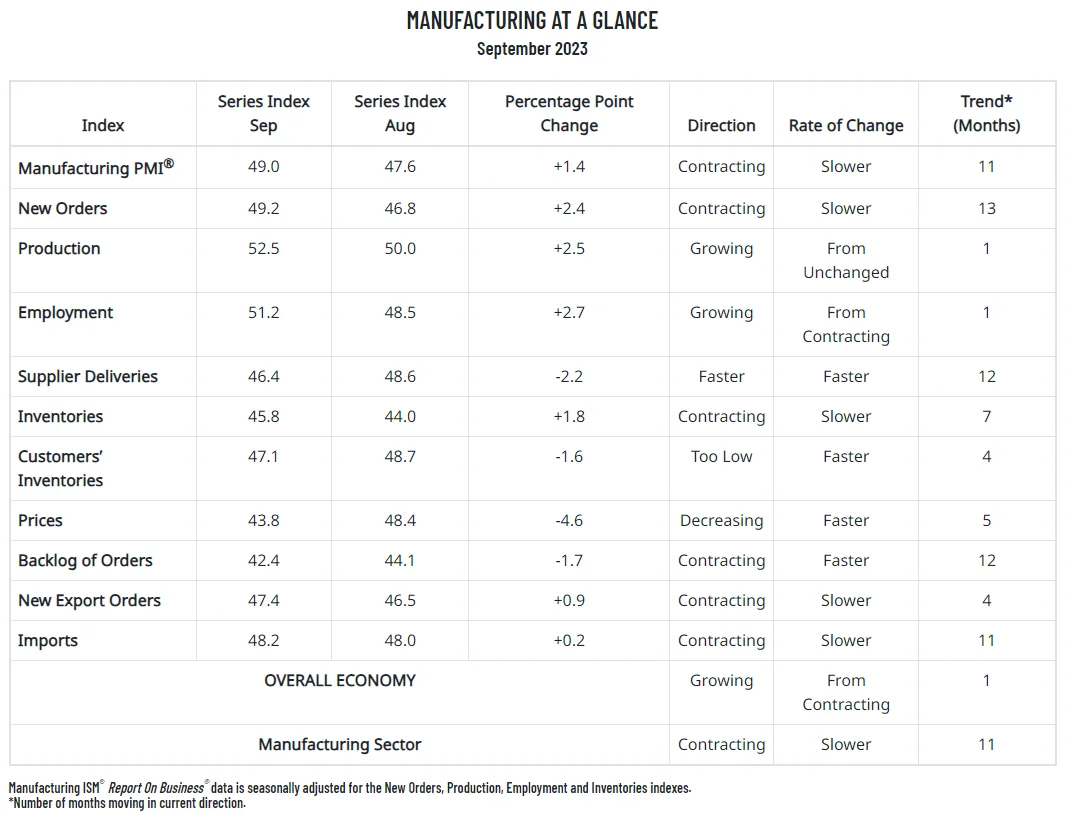

The latest ISM manufacturing report indicated more easing backlogs as new orders contracted for the thirteenth consecutive month amid slowing production. The new orders index contracting adds further uncertainty about future backlogs and, in turn, truckload demand. Although backlogs are contracting at an increasing rate, higher production levels indicate the sector still has pent-up demand, which should enable healthy volumes in the near term.

Figure 22: ISM Manufacturing Report, Manufacturing at a Glance

Figure 22: ISM Manufacturing Report, Manufacturing at a Glance

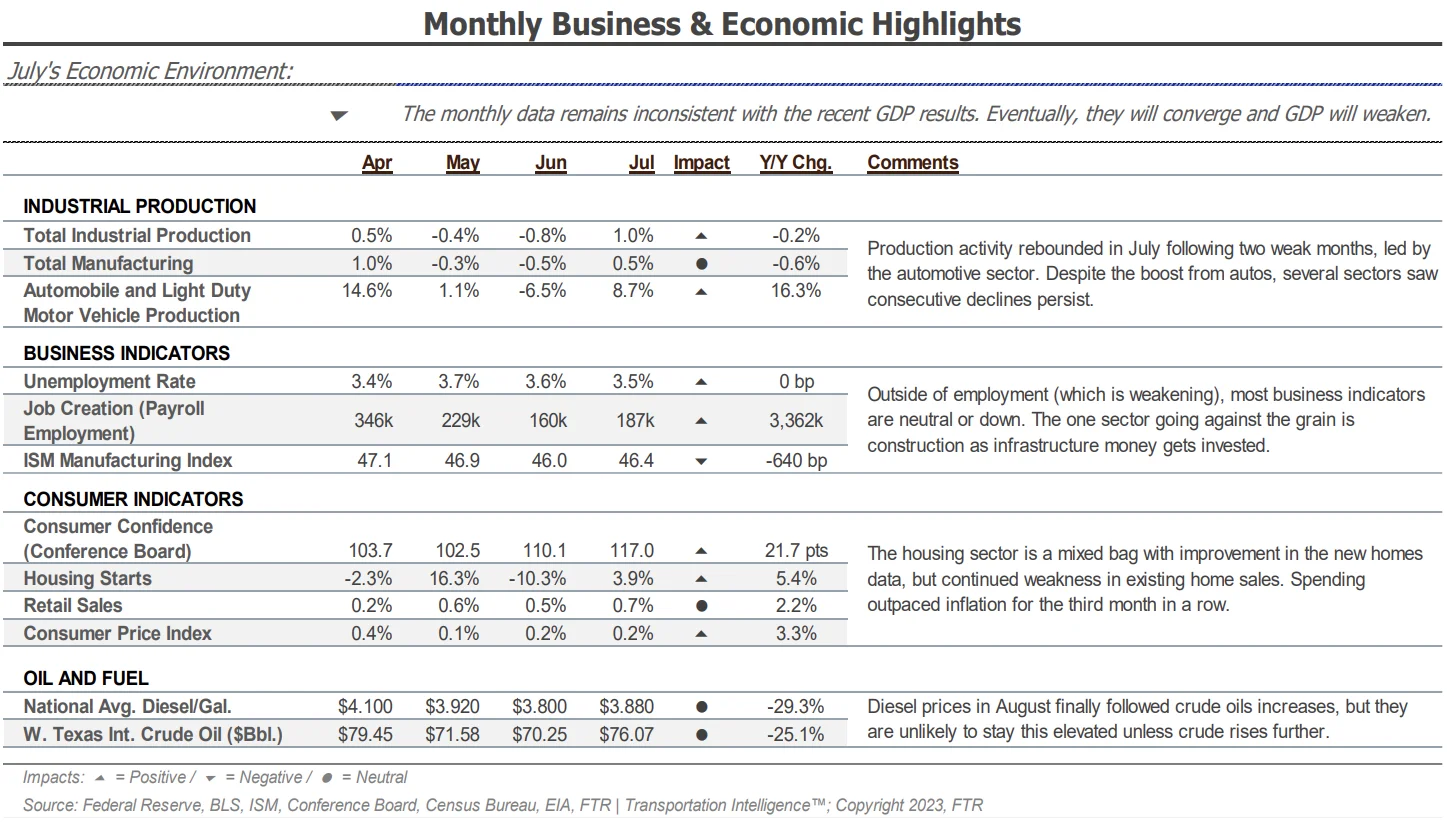

Figure 23: Monthly Business & Economic Highlights

Figure 23: Monthly Business & Economic Highlights

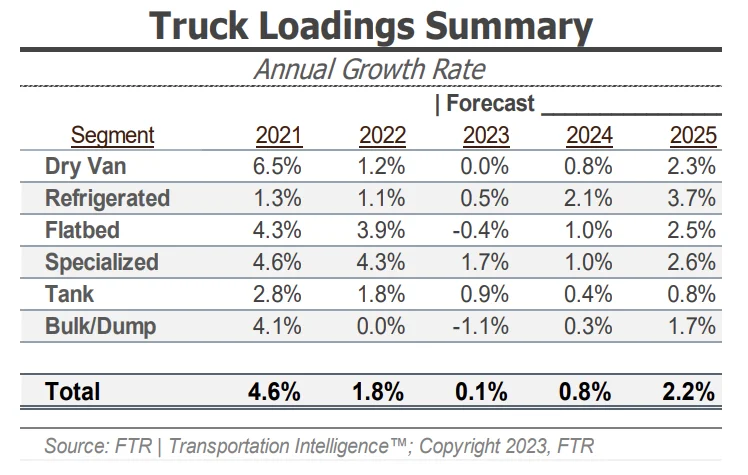

FTR’s latest truck loadings forecast for 2023 fell slightly from 0.2% year-over-year growth a month ago to 0.1%. FTR noted that the latest outlook indicates stronger activity for loadings related to construction, which offset the weaker outlook for food and bulk aggregates. The 2024 outlook revision showed growth easing from 0.9% to 0.8%, indicating a relatively unchanged perspective for the year ahead.

Figure 24: FTR’s Truck Loads Summary

Figure 24: FTR’s Truck Loads Summary

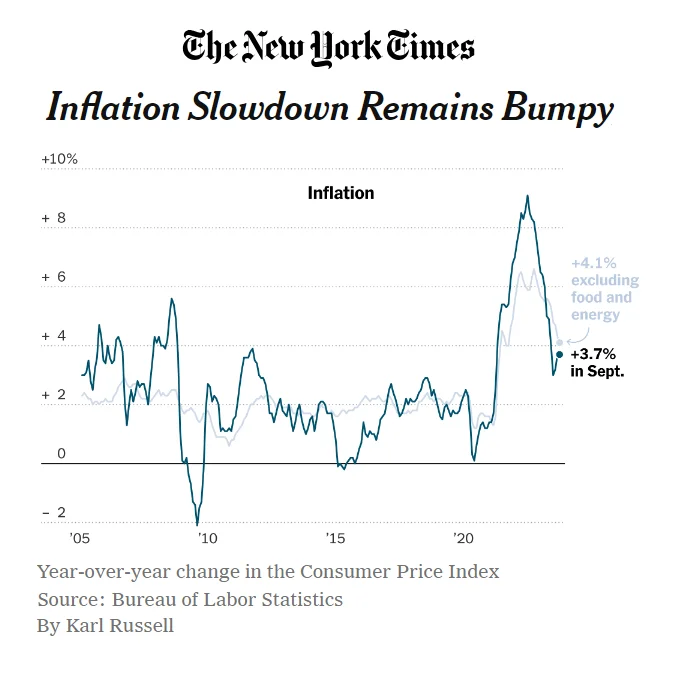

September CPI data showed that inflation will likely remain sticky even though price increases have cooled notably. This is the concern as we look toward 2024 because while there is no direct relationship to truckload demand, it is easy to make a connection between elevated interest rates and slowing freight volumes.

It is unlikely that the Fed will lower interest rates if inflation remains above the target, leaving questions about whether the inventory cycle reset will be enough to stabilize freight volumes. But inflation eases, the Fed could lower interest rates, which could bolster housing activity and manufacturing investment — two currently slumping sectors that contribute meaningfully to freight demand.

Figure 25: New York Times Inflation Data

Figure 25: New York Times Inflation Data

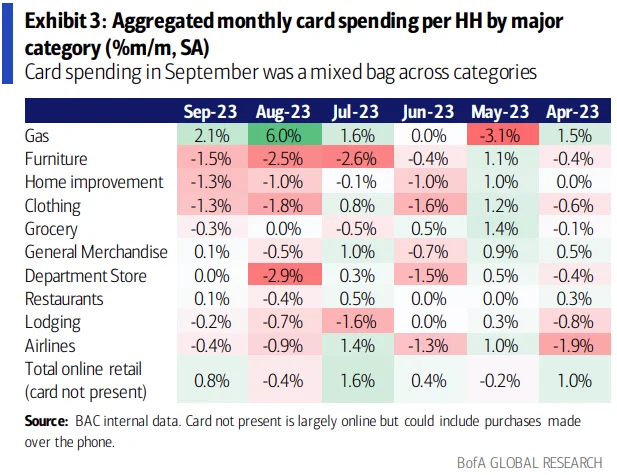

Bank of America card data showed consumer spending per household increased by 0.7% year-over-year in September, and card spending per household increased by 0.2% month-over-month on a seasonally adjusted basis. Spending was weak across most categories, particularly furniture, home improvement, and clothing. Gas spending remained strong, and spending growth at general merchandise stores and restaurants improved relative to August.

Bank of America noted that at least some of this improvement resulted from increased spending around Labor Day weekend. This is consistent with a larger bump around July 4th than normal, a sign that consumers may now be more prone to ramp up spending around the holidays, offering some hope for the Q4 outlook. They also noted that there does not yet seem to be any noticeable decline associated with the resumption of student loan repayments.

Figure 26: Bank of America Aggregated Monthly Card Spending

Figure 26: Bank of America Aggregated Monthly Card Spending