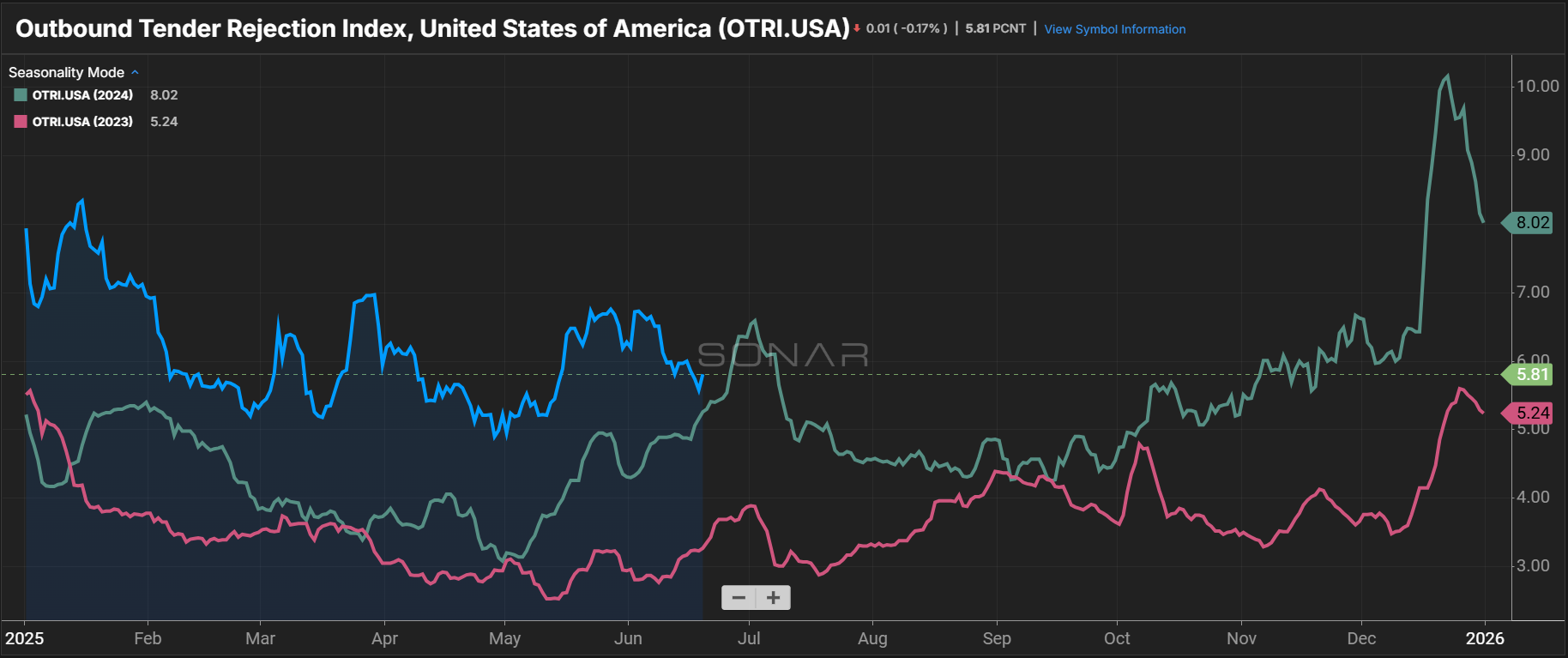

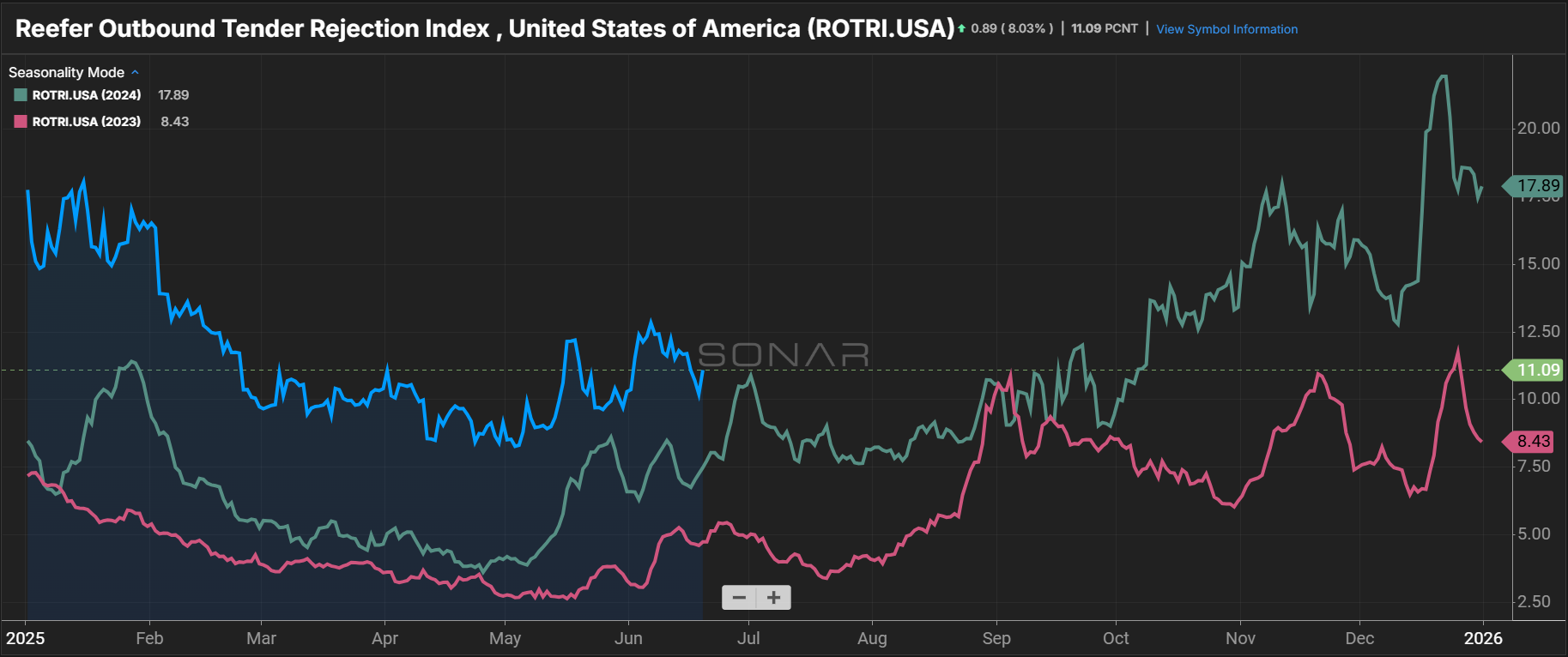

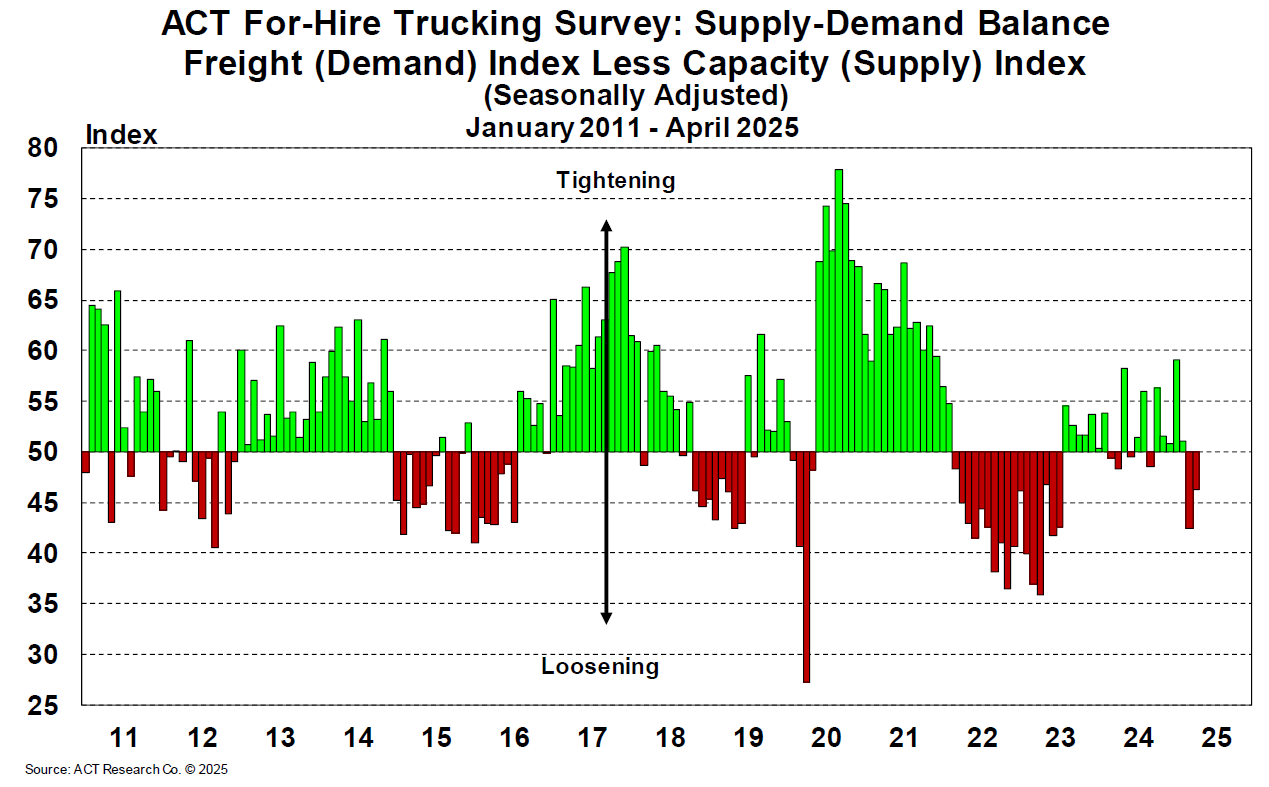

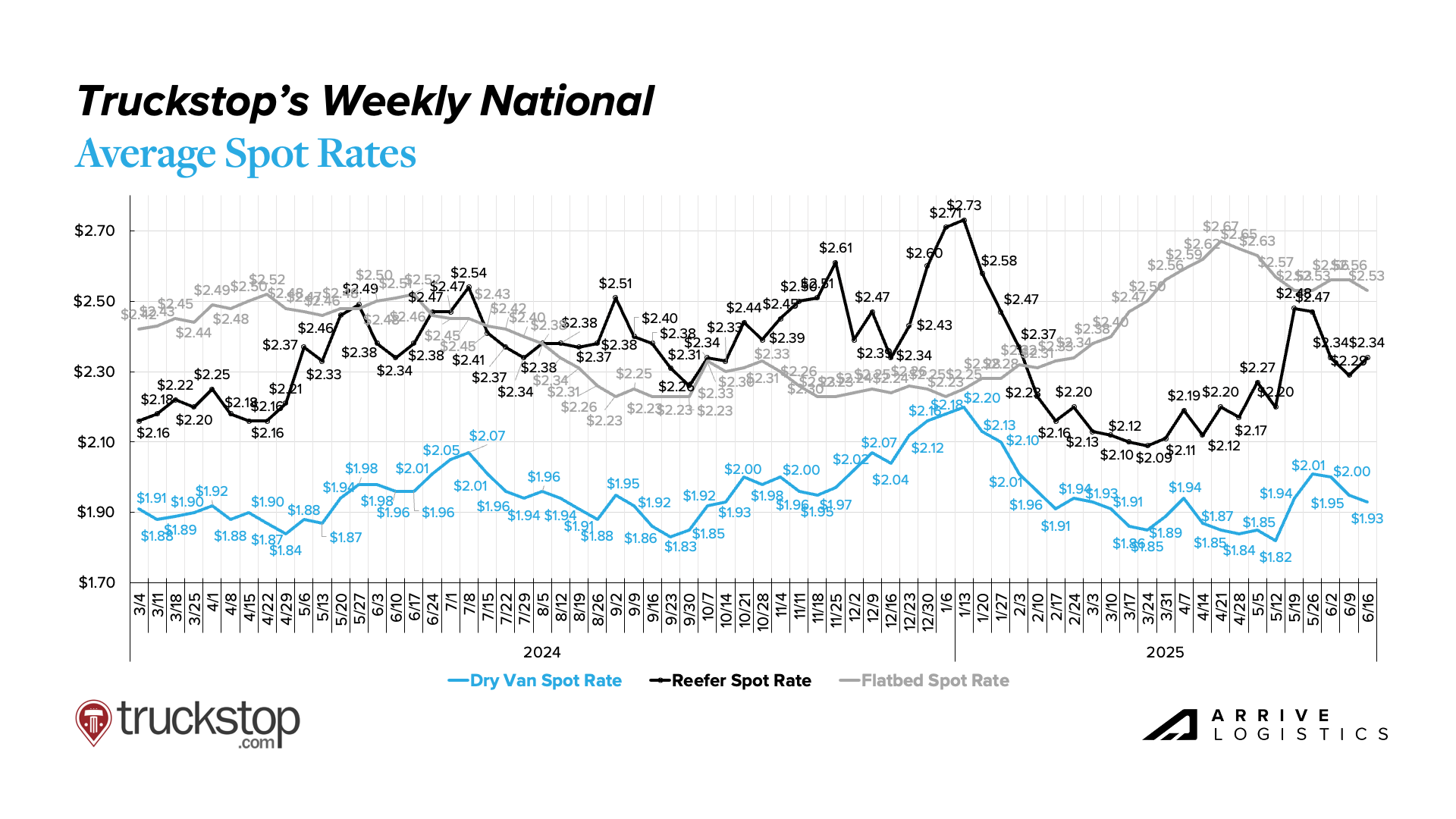

May data showed continued seasonality in a freight market that remains in somewhat of a holding pattern. Aside from temporary volatility as supply contracted around Roadcheck Week, the narrative of the last few months held true: low volume, persistently strong supply and spot rates that settle as quickly as they spike.

While we don’t anticipate a near-term demand disruption significant enough to trigger sustained inflationary conditions, several variables could shape the market’s trajectory through the remainder of peak season.

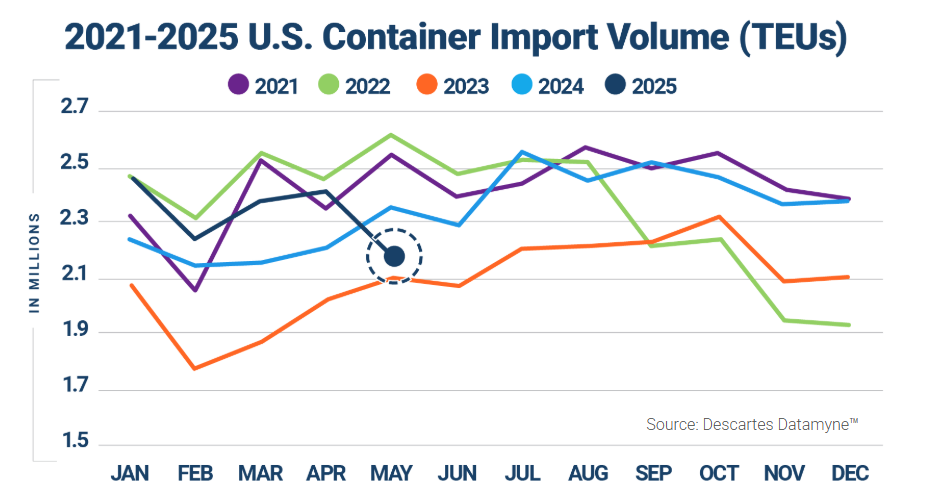

First, while it’s challenging to predict a precise outcome, the pending court decision on the legality of elevated U.S. tariffs could prove to be a critical turning point in the ongoing trade war. The impact of increased U.S.-China tariffs has started to materialize in the data, particularly on the import side. That said, the recent reduction of some tariffs has temporarily eased pressure, and forward-looking import data—on orders placed but not yet shipped—suggests a volume recovery may be on the horizon.

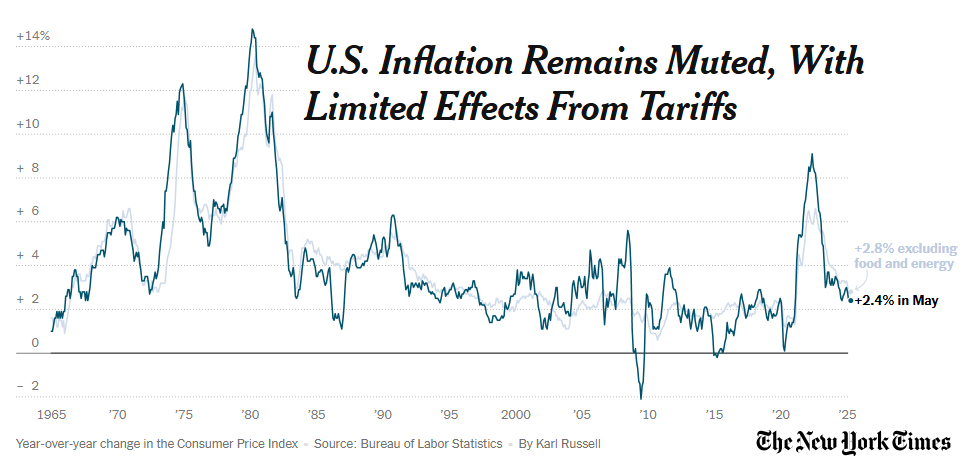

However, economic headwinds are also a key factor, as rising prices have led to cooling consumer spending that could put demand at greater risk of faltering.

Meanwhile, resilient carriers are supporting strong supply levels amid ongoing volume declines, limiting upward rate pressure even as spot activity briefly increased last month. If sluggish demand and elevated capacity levels persist, it could limit any upside market potential in the coming months.

New and forthcoming regulations from the Federal Motor Carrier Safety Administration—such as identity verification and English proficiency requirements—might also begin to reduce available capacity, though the exact timing and impact of the changes remain uncertain.

With the May market test behind us, all eyes now turn to how conditions will shape up amid these variables ahead of the Fourth of July holiday.

For a closer look at what’s happening across demand, supply and rates, keep reading.