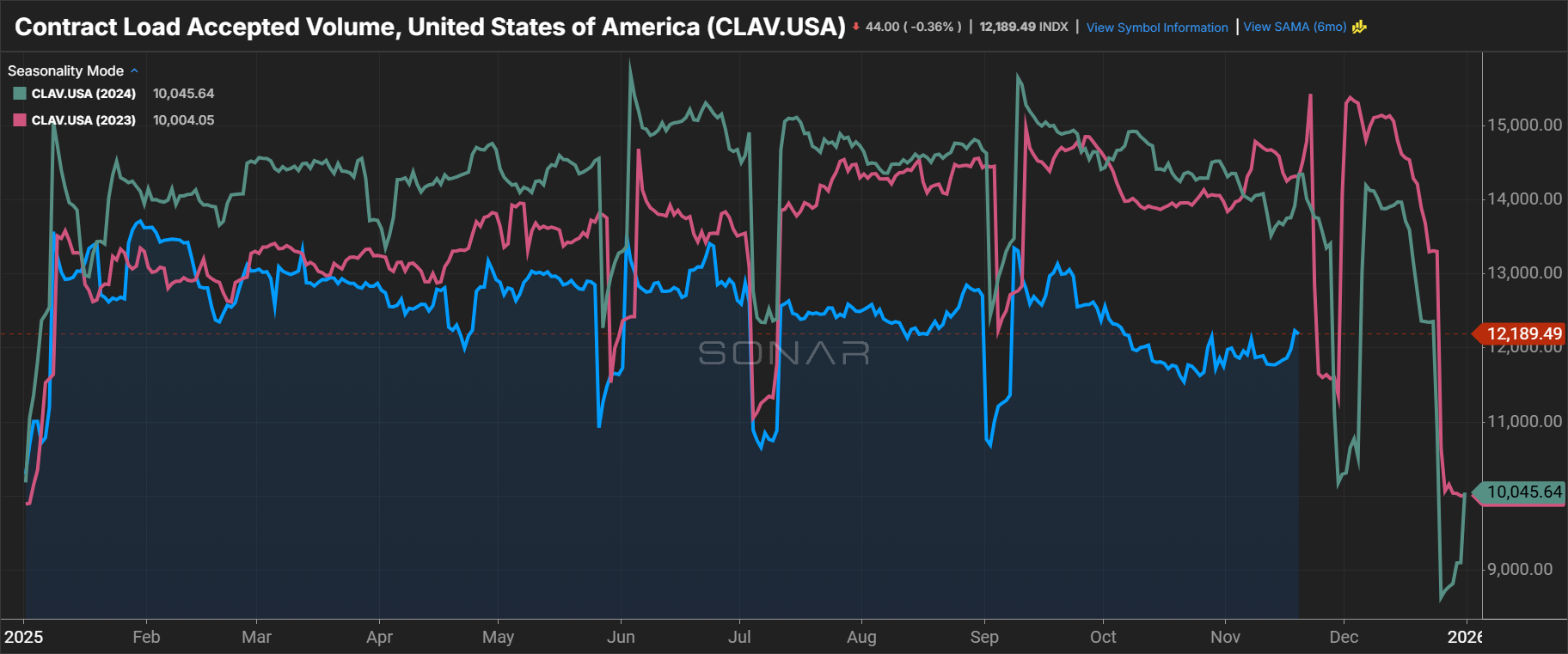

Volatility tied to Q3’s close and the late-September announcement of new non-domiciled CDL regulations has largely settled. Long-haul markets saw the greatest impact, though even that was muted.

With the U.S. Court of Appeals now pausing enforcement, near-term supply pressure should continue to ease. Combined with low demand and low rates, freight market conditions are unusually calm for this time of year.

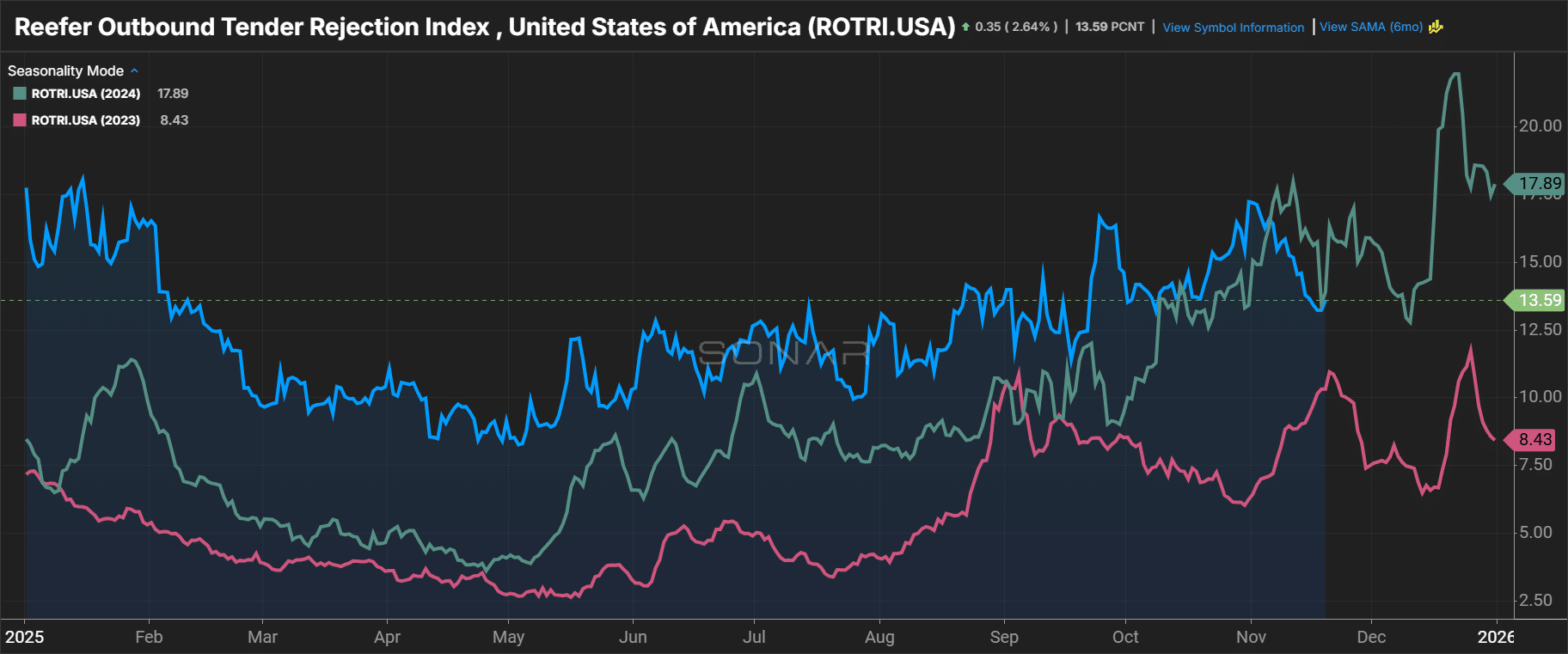

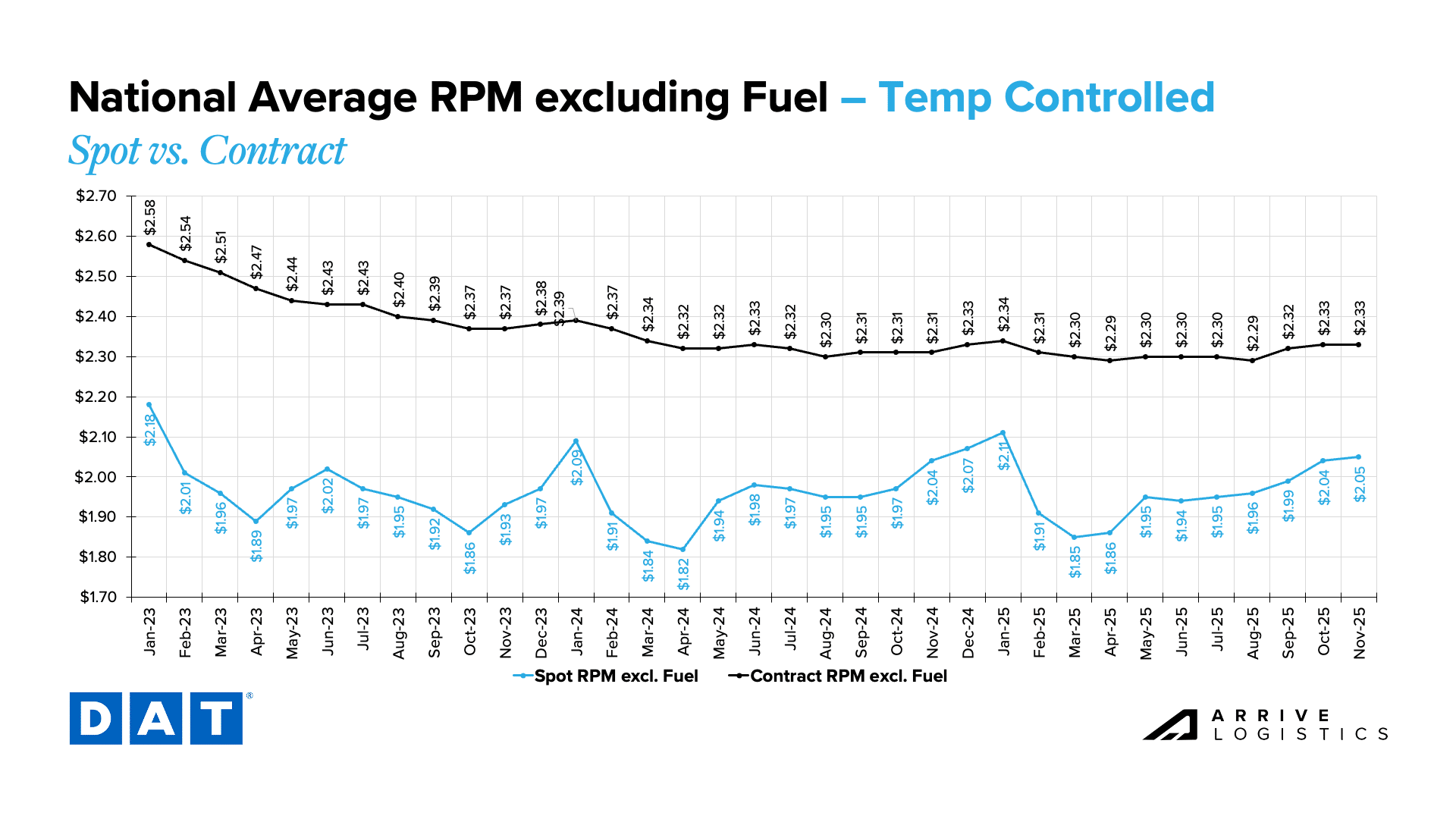

Reefer rejection rates followed normal seasonal patterns through October before falling in early November, with only pockets of tightness driven by seasonal food shipments and freeze-protect demand. With continued softness across other major modal markets, current capacity should easily cover short-term holiday or weather-related disruptions.

Longer-term conditions are less certain, as equipment orders remain below replacement levels and ongoing regulatory uncertainty could create downside risk.

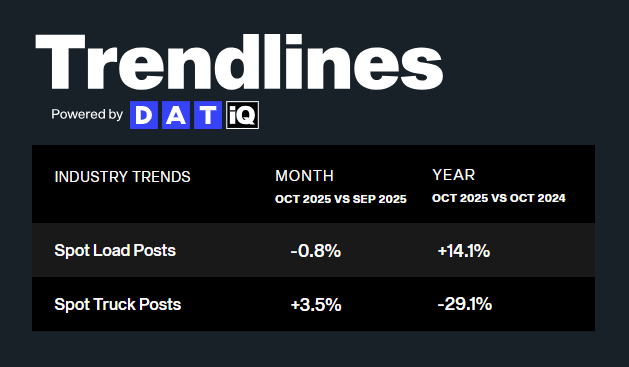

Import volumes remain soft due to the summer pull-forward surge that left shippers well-stocked long before typical peak season preparation began. With retail forecasts now pointing to declining volumes through year-end and manufacturing still contracting, meaningful near-term demand growth looks unlikely.

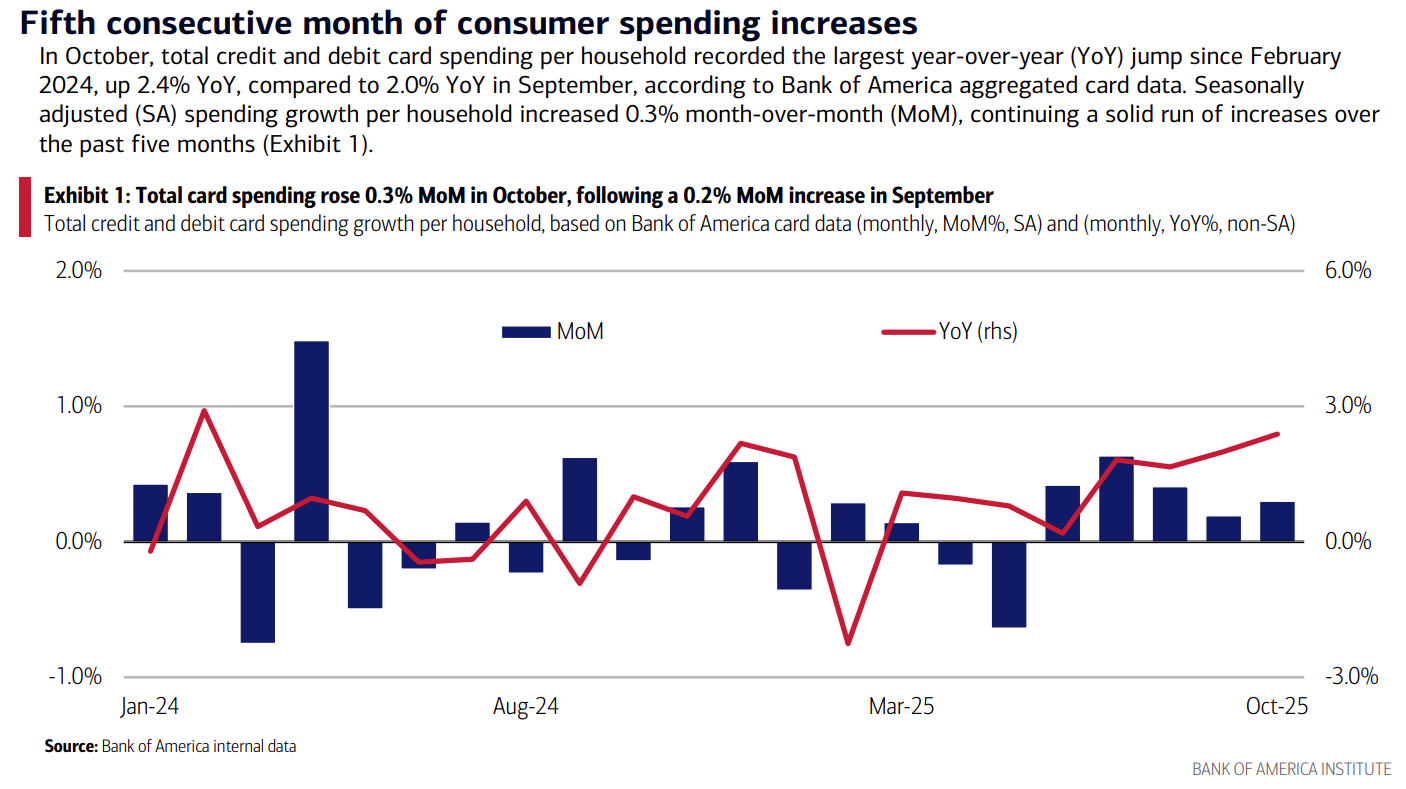

The government shutdown disrupted economic and labor market data availability this month, but Bank of America card data shows consumers are still spending despite inflation and interest rate uncertainty.

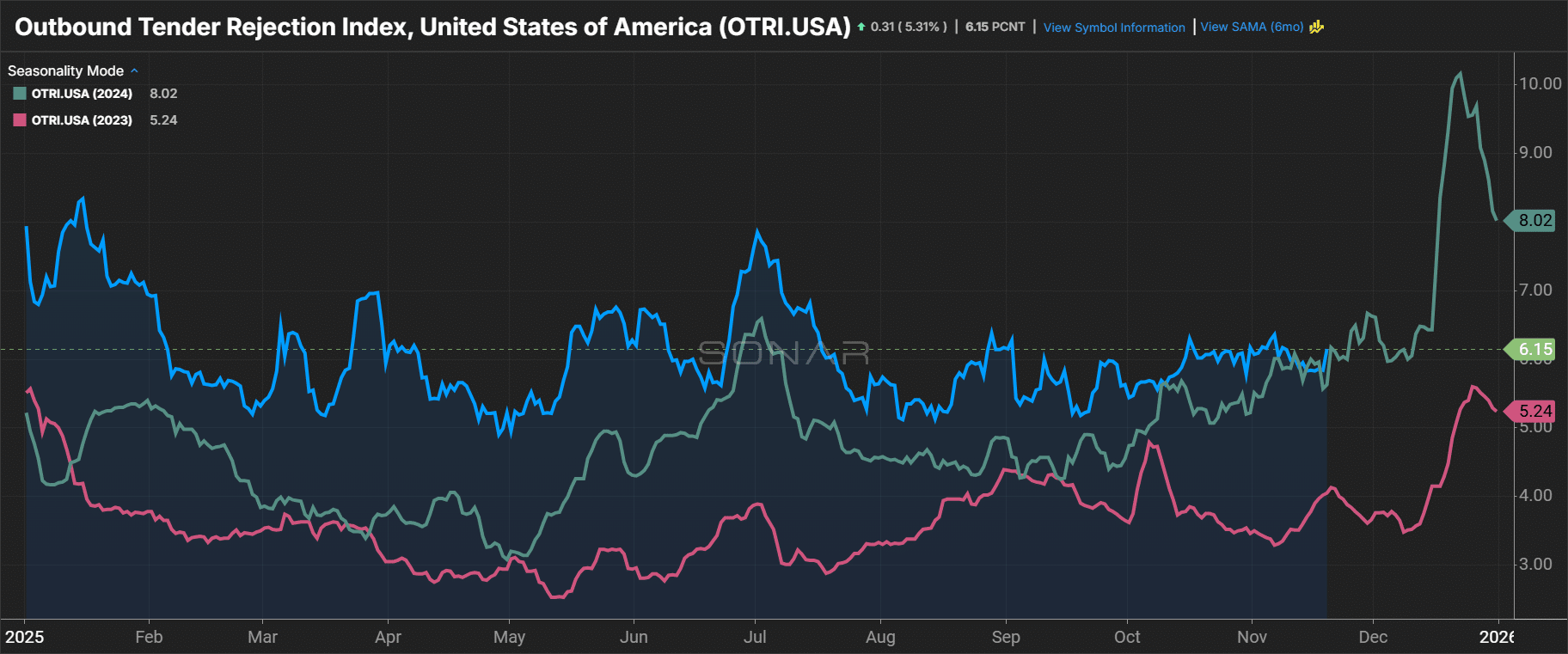

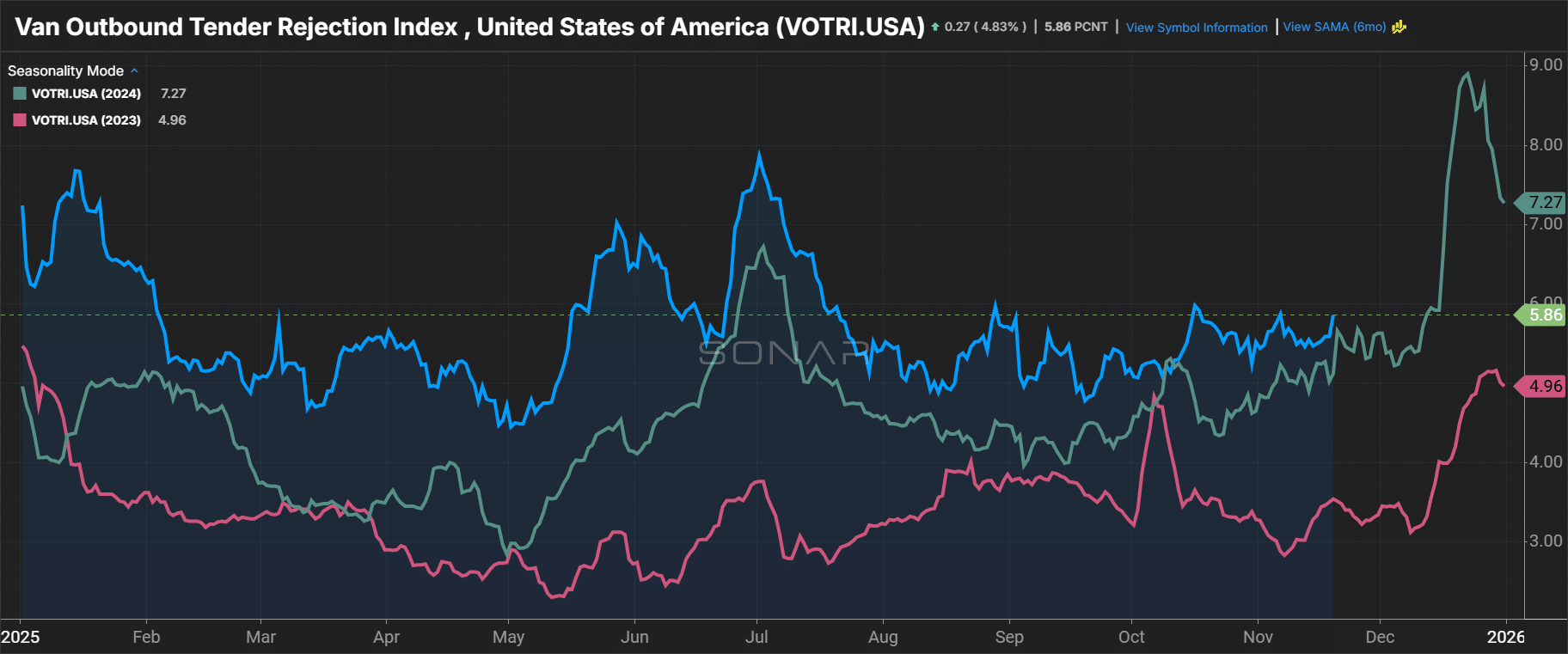

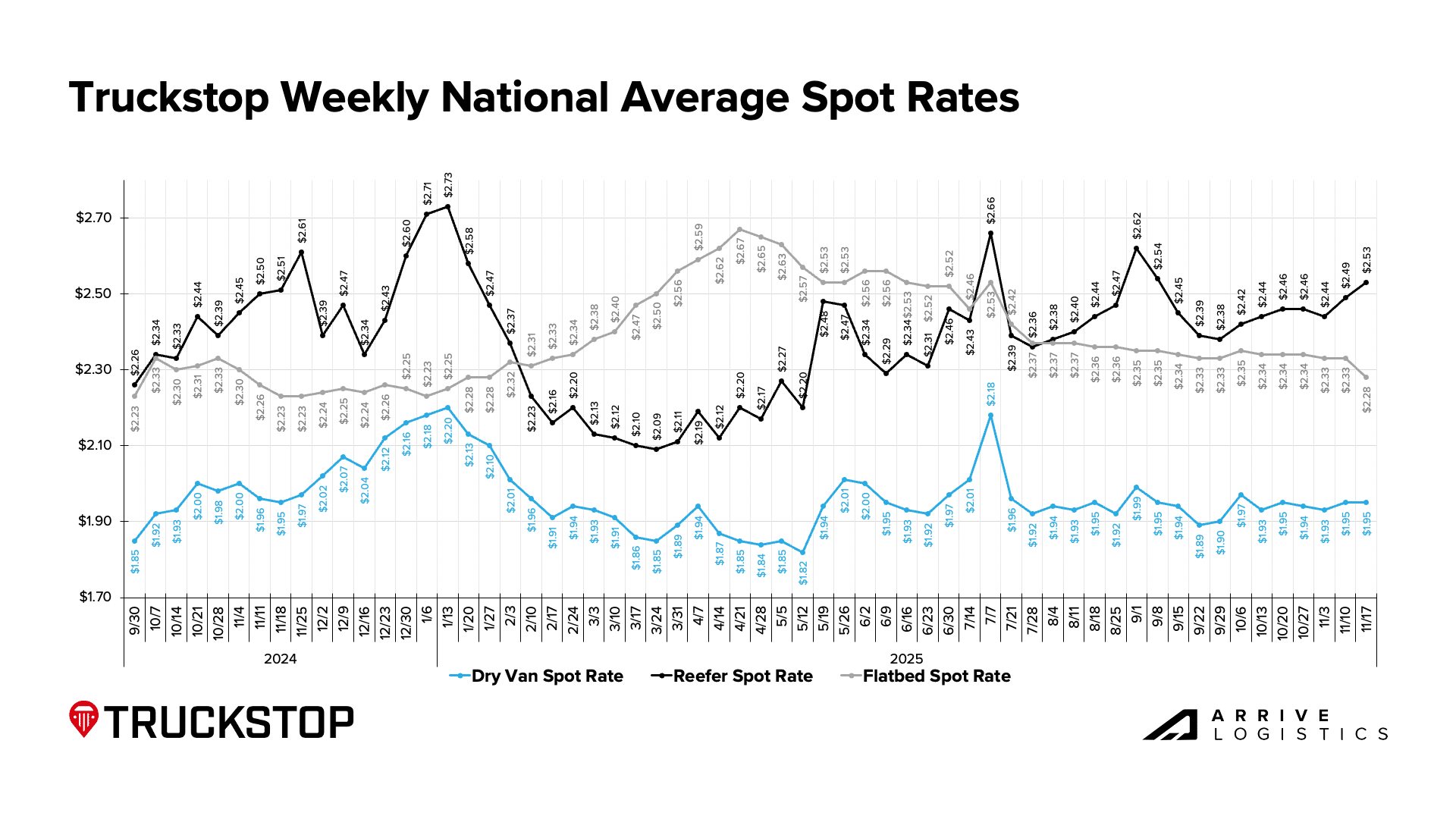

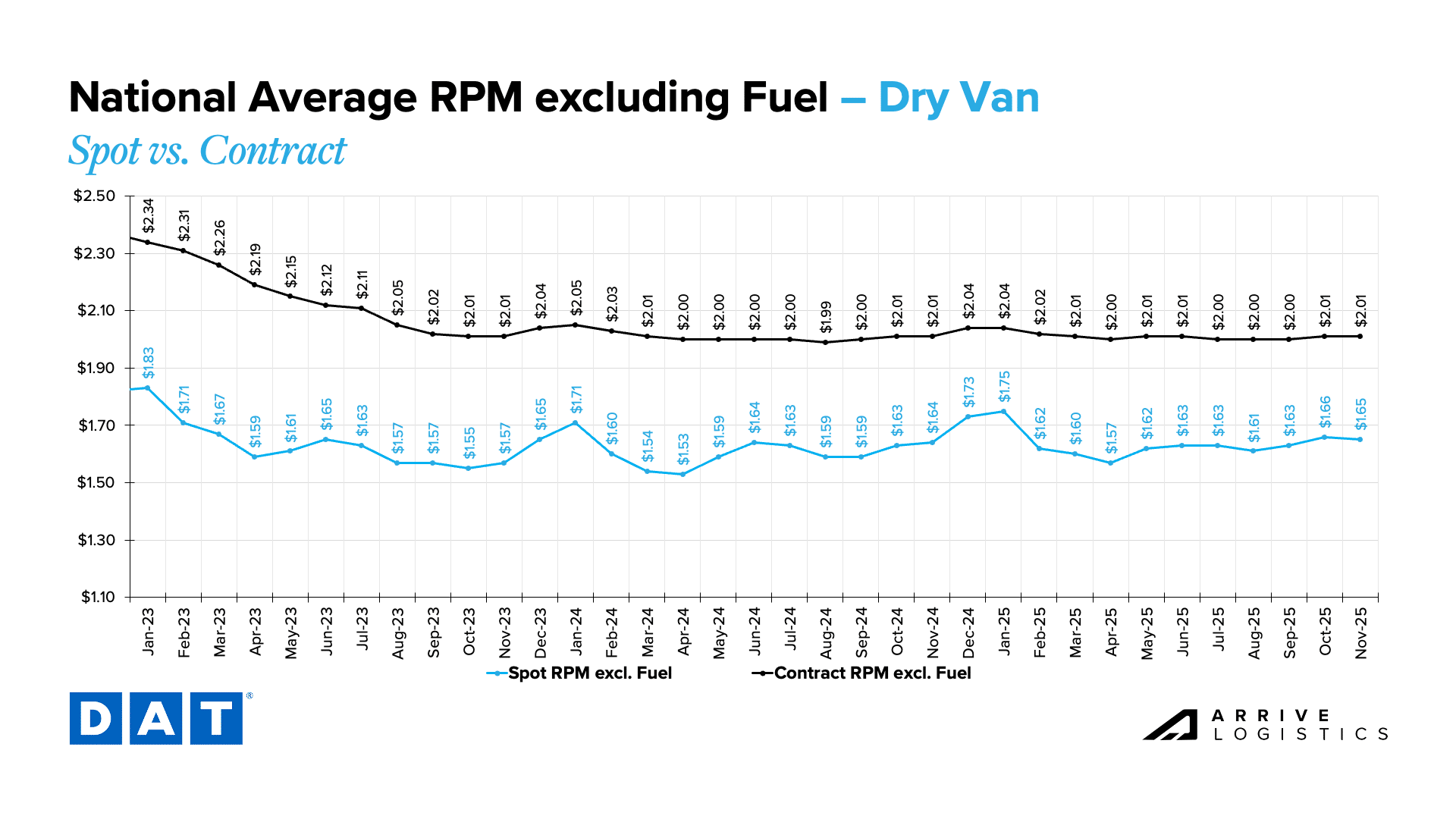

While indicators point to a muted peak season overall, some tightness and rate increases will still materialize. Reefer should see the most significant disruption as food shipments pick up through November and December, but dry van equipment remains susceptible to demand spikes and severe weather events, especially as drivers take time off for the holidays. Even so, strong supply levels should limit the duration of any disruptions.

Read on for a full breakdown of demand, supply, rates and economic conditions this month.