"*" indicates required fields

"*" indicates required fields

"*" indicates required fields

This document provides our outlook for national dry van and reefer truckload rates from January 2024 through December 2026. The Arrive Insights team developed this forecast using extensive historical research and predictive models built into ARRIVEnow™, our proprietary technology platform.

Successfully navigating freight market cycles begins with understanding the relationship between rates and the core drivers of truckload supply and demand. High or rising demand in a tight capacity environment puts upward pressure on rates, while weak or easing demand amid ample capacity pushes rates down.

By tracking directional trends in truckload demand (volumes) and available capacity (trucks), we can forecast rate trends with a high degree of accuracy and consistency. With that, we present our outlook for the year ahead.

David Spencer, VP of Market Intelligence, and Aaron Galer, SVP of Strategic Partners at Arrive Logistics, sat down with Ken Adamo, GM, Shipper and Chief of Analytics at DAT, to break down Arrive’s 2026 Truckload Freight Rates Forecast and the forces shaping the freight market, helping shippers and carriers understand the key risks and inflection points to watch and prepare for the year ahead.

The domestic truckload market has reached an inflection point and is entering a period of sustained spot and contract rate inflation. Winter storms acted as a catalyst, but several years of challenging trucking conditions have driven a mass exodus of capacity that has left the market far more vulnerable to disruption.

The summer peak shipping season between DOT Roadcheck Week in mid-May and the Fourth of July will be the next key period to watch, as tightening capacity amid elevated demand is expected to push spot rates to their highest levels in years. A weak but stable demand environment could limit how high rates move and how long disruption lasts, but if upside risks materialize, inflationary conditions could extend into 2027.

Equilibrium between truckload supply and demand has created an environment where disruptions now have an outsized impact on rate volatility compared to recent years.

Inflationary pressure could persist without a meaningful shift in demand, as the need for higher rates within carrier networks continues to disrupt routing guide compliance, drive spot demand and keep spot rates elevated.

Shippers have more tools and more information at their disposal than ever before. API pricing integrations can introduce competition where it did not exist in prior inflationary cycles and expand access to capacity, increasing carrier network flexibility and helping rates find a floor more quickly once disruptions fade.

Carriers will gain greater pricing control as spot rates remain elevated and operating costs continue to rise. A rate correction would bring needed relief to struggling carrier businesses, enabling overdue investment in equipment maintenance, driver wage increases and more.

Seasonal demand fluctuations will be the key driver of near-term spot rate volatility. With rates rising through what is typically a period of easing in the annual cycle, produce season and the summer peak will further test the upper limit for rates in the current environment.

As the market shifts and carriers gain greater optionality, prioritizing practices such as providing flexible shipping windows and adequate lead times, improving loading/unloading efficiency and expanding carrier networks will help shippers retain consistent access to capacity and limit exposure to higher rates.

Reefer conditions appear to be normalizing faster than dry van. Significant crop damage in regions like Florida from a rare cold snap could limit produce demand and the typical seasonal capacity crunch. While van and reefer markets usually move in tandem due to the interchangeability of freight, reefer carriers will also pursue van freight when the market is strong, leaving less capacity available to support reefer demand.

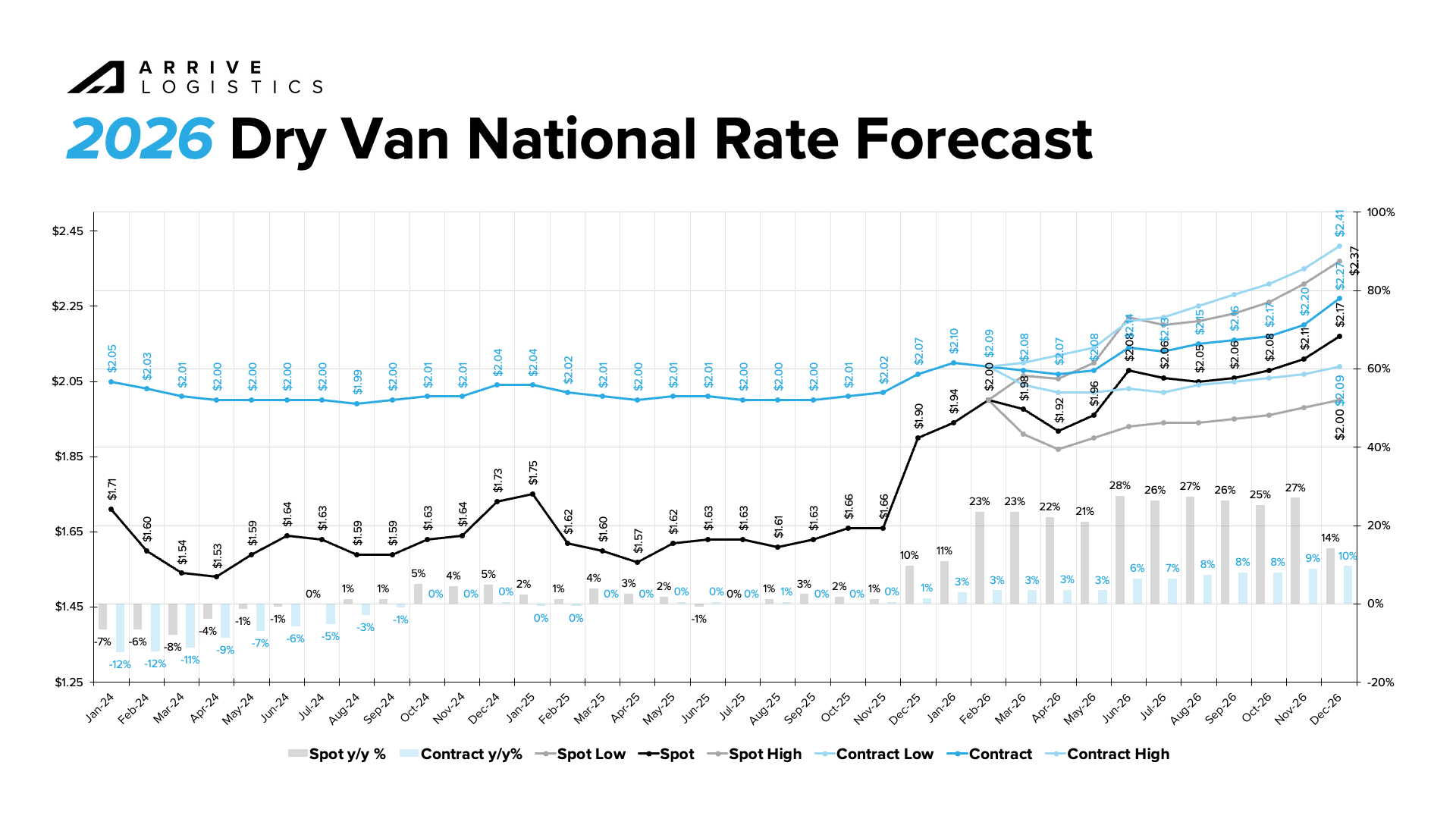

Van spot rates will reach a peak year-over-year growth rate of 28% in June 2026.

Van contract rates will reach a peak year-over-year growth rate of 10% by December 2026.

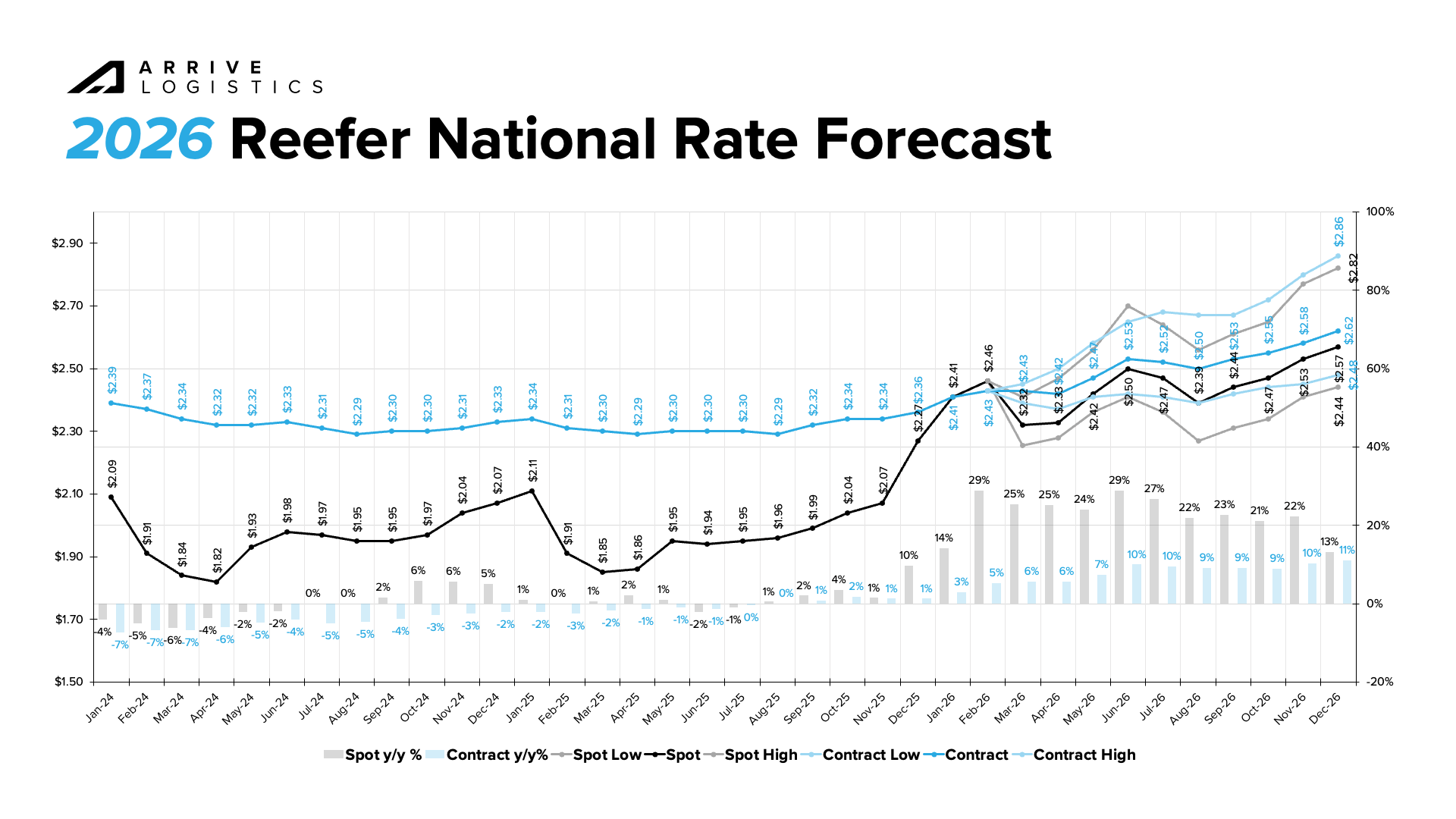

Reefer spot rates will reach a peak year-over-year growth rate of 29% in June 2026.

Reefer contract rates will reach a peak year-over-year growth rate of 11% by December 2026.

Overall demand remains weak, but increased spot market volumes are driving spot rate volatility. Green shoots in manufacturing and tariff restructuring point to potential growth in imports and manufacturing demand, while housing remains a key drag on the growth outlook.

On the consumer side, spending has held steady and the labor market is stable. As long as those trends continue, volumes should avoid further declines, though any growth could cause additional upward pressure on demand and rates.

Routing guide disruptions continue across all modes, driving increased spot market demand and keeping upward pressure on spot rates. In order for current rates to decline, contract compliance will need to fall from elevated levels to relieve spot market demand.

Domestic manufacturing returned to expansion for the first time in nearly a year as the share of the sector in contraction fell sharply from December. The improvement is notable given how broad the pullback was late last year, but a similar one-month expansion in 2025 was followed by renewed weakness, making it too early to determine whether this marks the start of a sustained recovery.

Import volumes still reached the fourth-strongest January level on record despite declining 6.8% year-over-year. This is encouraging for demand, especially if recent tariff policy shifts create coverage gaps that allow importers to make use of lower duty windows.

A cooling labor market could create some downside pressure. Conditions are stable for now, so consumer spending should remain at or near current levels unless conditions deteriorate.

The freight market is far more sensitive to disruption now that capacity sits in equilibrium with demand. This vulnerability became particularly apparent as tender rejection rates surged during Winter Storm Fern, and their continued elevation signals resistance against a return to 2025 conditions.

These trends suggest the market has reached a tipping point where the rate environment of the past few years no longer supports trucking businesses. Carrier operating costs continue to rise, from increasing insurance premiums and equipment expenses to wage growth and driver recruitment challenges. Emissions regulations taking effect in 2027 are also driving many carriers to pre-buy 2026 model-year equipment, adding further pressure to already tight budgets.

Simply put, it is not getting any cheaper or easier to run a truck in this new operating environment, so carriers will prioritize rates that support their businesses.

The truck driver role is facing heightened scrutiny. From English-language proficiency rules to audits on non-domiciled CDLs, adding and retaining drivers will remain difficult. This could increase the magnitude and duration of disruptions by limiting how quickly capacity can return when needed.

Year-over-year growth in tender rejections during seasonal and weather-driven disruptions points to mounting routing guide challenges and a more balanced supply environment. The failure of rates to normalize after recent events indicates that capacity is no longer sufficient to absorb disruptions as it was in recent years.

With the average age of equipment at or near record levels after a long stretch of weak equipment orders, the tractor population is shrinking at a time when fleets should be replacing equipment. This alone may not spark an inflationary rate cycle, but it will help sustain one.

This forecast reflects our base-case scenario based on the information available at the time of writing. Upside and downside risks could materialize due to unforeseen events, including the following:

Ongoing uncertainty around tariff policy has clouded the truckload demand outlook for 2026. Although the Supreme Court ruled against using the International Emergency Economic Powers Act (IEEPA) to impose tariffs on imported goods, the administration appears intent on pursuing other methods, beginning with broad Section 122 tariffs of 15% on all goods for 150 days following the ruling. Meaningful changes to the overall tariff environment could create both upside and downside risks to the forecast.

A recession appears unlikely in the near term, but uncertainty remains. The effects of elevated inflation and interest rates are still working through the economy and could worsen trucking conditions faster than expected, especially if consumer spending and manufacturing growth trends reverse.

Severe weather has proven highly disruptive to the freight market in recent months. With inflationary pressure already building, significant weather events could further tighten conditions and push rates higher than they would during deflationary periods.

Spot rates remained below operating costs per mile for nearly three years. Historically, spot rates can only fall so far before carriers begin exiting the market, creating upward pressure. Rates must remain elevated for a sustained period before carriers feel confident investing in growing or even maintaining fleet size. As a result, the length of the downturn could extend the time needed for conditions to normalize.

Fuel price and fuel surcharge volatility can complicate the measurement of forecast errors and influence shipper and carrier behavior. For example, rapidly declining fuel costs can ease conditions for carriers while reducing pressure on shippers seeking cost savings. Although fuel prices have been relatively stable recently, the past two to three years have redefined fuel price volatility.

The national average spot and contract rates per mile used in this report are sourced from DAT and receive no additional processing by Arrive. DAT may revise previously published rates, which can create variations between this report and DAT materials. Based on the macroeconomic factors shaping supply and demand in the domestic truckload freight market, our goal is to set reasonable expectations for the directional movement of the national average spot and contract rates published by DAT.

Get this free report delivered straight to your inbox every month.