"*" indicates required fields

"*" indicates required fields

"*" indicates required fields

This document contains our comprehensive outlook for national dry van and reefer truckload rates through December 2024. The Arrive Insights® team generated this forecast through a combination of extensive historical research and output from the predictive models built into ARRIVEnow, our proprietary technology platform.

Successfully navigating freight market ebbs and flows begins with a basic understanding of the relationship between rates and the unique components of truckload supply and demand. Simply put, high or increasing demand and tight capacity will cause upward rate pressure, whereas low or easing demand and ample available capacity will drive rates down.

By tracking directional trends for truckload demand (volume) and available capacity (trucks) in the market at any given time, we can predict rate trends with a high degree of accuracy and consistency.

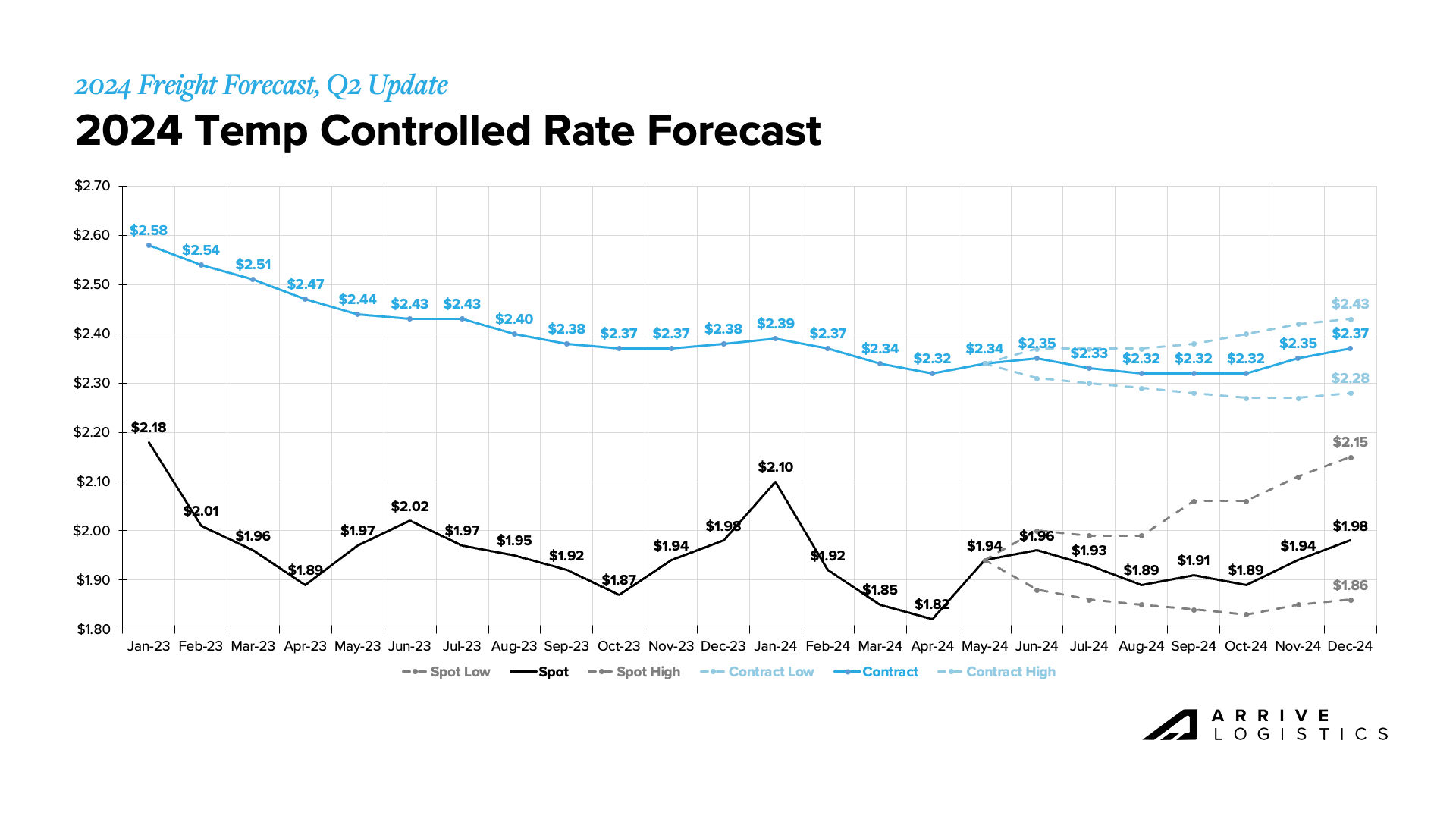

As 2024 progresses, we anticipate spot rates will remain relatively stable, with some volatility in line with typical seasonal patterns. Contract rates will continue to normalize but slower than in 2023, likely finding a floor in late Q3 or early Q4 2024. The contract-spot rate gap will decrease slightly over the year, marginally increasing the market’s vulnerability to significant disruption. However, given the current oversupply of capacity, any major disruption would likely require a black swan event or other catalyst, making it difficult to predict the exact timing of the next major cycle shift.

Forecast Indicates:

Freight tonnage is unlikely to significantly improve trucking conditions. However, a resilient economy and steady consumer demand amid ongoing inflation are keeping demand relatively stable. Downside risk remains as economic conditions show signs of a potential slowdown.

The market remains oversupplied and is thus unlikely to experience a significant enough correction to increase vulnerability to disruption in 2024.

This forecast outlines what we believe will be the most likely scenario based on the information available at the time of writing. The upside and downside risks presented could materialize due to unforeseen events, including but not limited to the following:

Ongoing wars in Europe and the Middle East, along with the threat of more attacks in the Red Sea, could continue to impact global trade. Similarly, tensions between China and Taiwan could affect Asia-U.S. relations and trade, particularly regarding Taiwan’s significant semiconductor production.

Although a recession seems unlikely in the short term, uncertainty remains. Effects from elevated inflation and interest rates are still emerging and could worsen conditions faster than expected, leading to declining trucking demand due to reduced consumer spending and manufacturing slowdowns.

Severe weather frequently disrupts the freight market. Winter storms early in Q1 had a notable impact, potentially indicating the market’s response to future weather-related disruptions. Additionally, forecasts for this year’s hurricane season show a high probability of numerous large storms, which have historically acted as inflationary catalysts.

Spot rates have remained below the operating cost per mile for public truckload carriers for most of the past year. When this happens, spot rates usually rebound or experience upward pressure because rates can only fall so far before carriers start losing money and exit the market. This scenario creates a rate floor, which is why our forecasted spot rates typically trend downward. As more capacity exits the market, spot rates will likely reset higher after each period of seasonal volatility.

Volatile fuel prices have impacted forecast trends, with rapid fuel surcharge changes complicating the measurement of forecast errors. These fluctuations can also alter shipper and carrier behavior. For instance, rapidly declining fuel costs create more favorable conditions for carriers and reduce pressure on shippers seeking cost reductions. Although fuel prices have been relatively stable recently, the past 2-3 years have redefined fuel price volatility.

The national average spot and contract rates per mile used in this report are sourced from DAT and undergo no additional processing by Arrive. However, DAT sometimes updates previously published rates, which can lead to variations between our report and materials created by DAT.

Based on the macroeconomic factors impacting supply and demand in the domestic truckload freight market, we aim to set reasonable expectations for directional movements of the national average spot and contract rates published by DAT.